Precipitated Barium Sulphate-Will be Only producer of this chemical in once its operational by H1FY24

Creation of new market of Precipitated 𝐵𝑎𝑟𝑖𝑢𝑚 𝑆𝑢𝑙𝑝ℎ𝑎𝑡𝑒 in

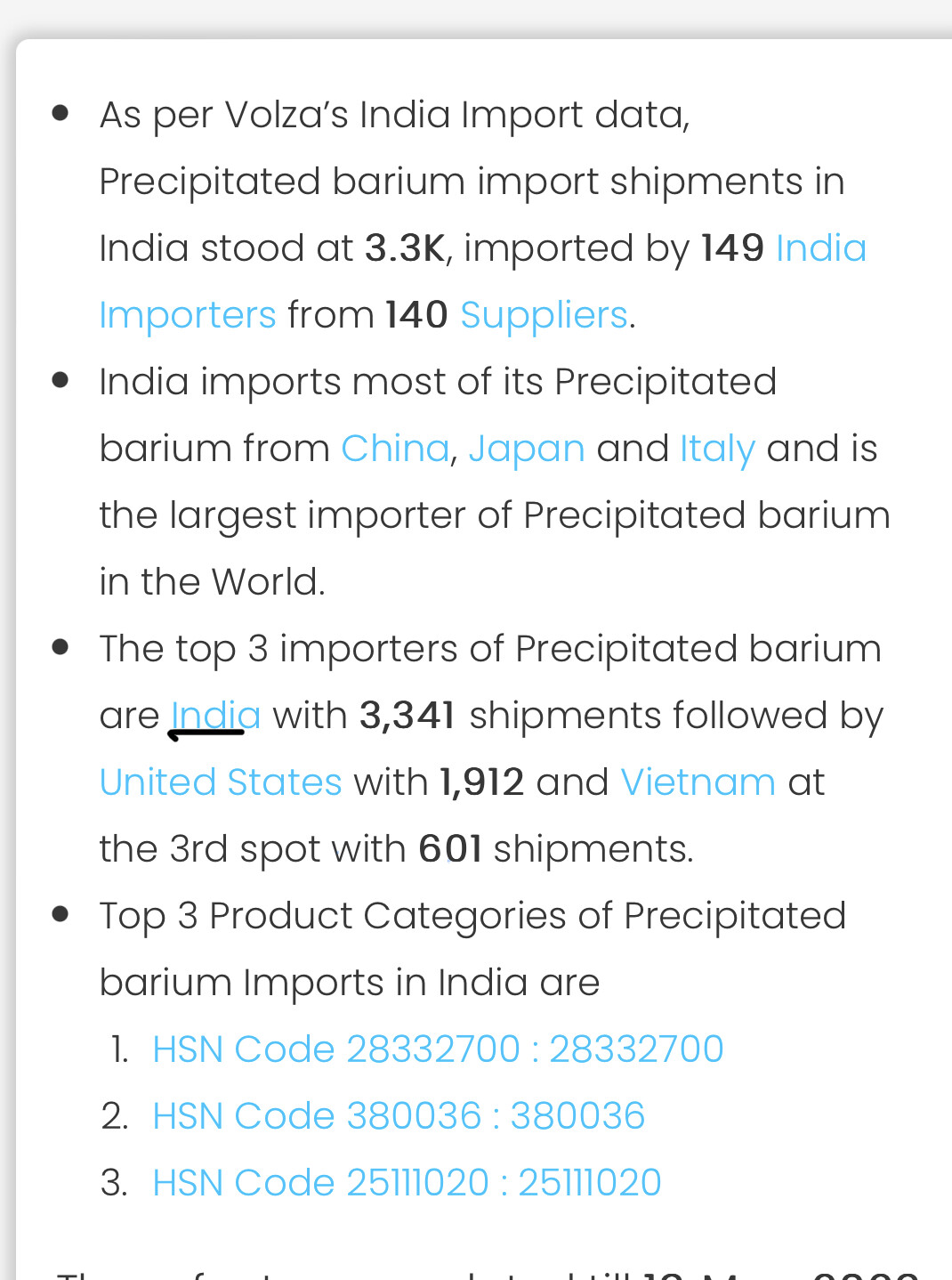

India Imports most of its Precipitated Barium Sulphate from China, Korea,Japan. Source (volza.com/p/precipitated… )

This is a Import Substitution + Export Opportunity for #VishnuChemicals

The demand is good across the globe,

Good runway ahead for them.

In the latest concall they spoke about how demand is not a problem for PBS. The challenge is them being able to get the requisite approvals from potential customers fast enough to be able to start selling as soon as Q1 FY24. From what I recall, it ois a 250-300cr sale per year opportunity from the present capex.

Vishnu Chemicals: Only producer of Barium Sulfate (Import substitute). Doubling topline by FY26.

Until 2019 we were only 2 prduct company. VAP gave higher growth and margins.

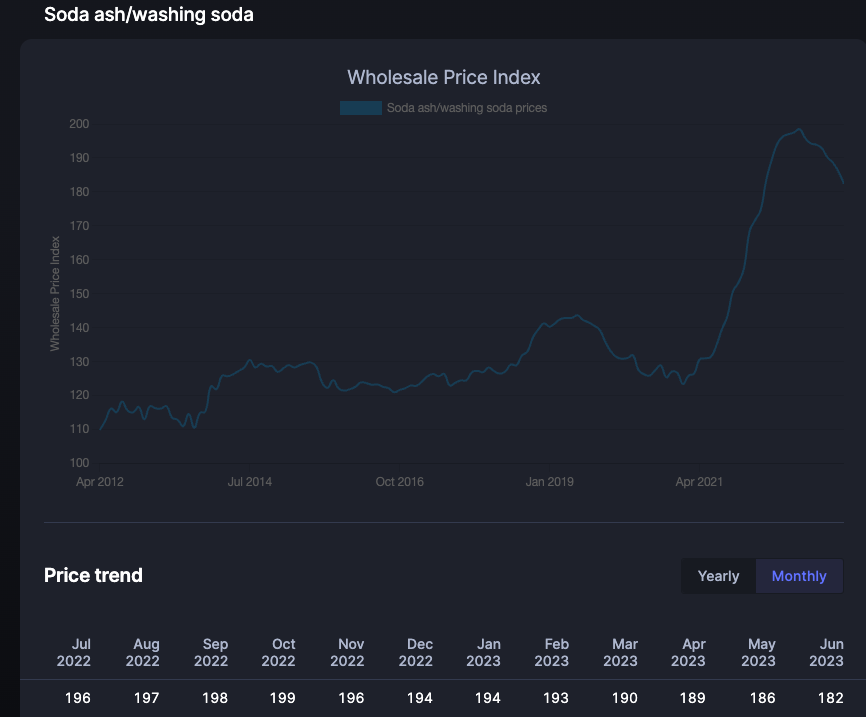

Soda ash consumption has come down significantly in total cost.

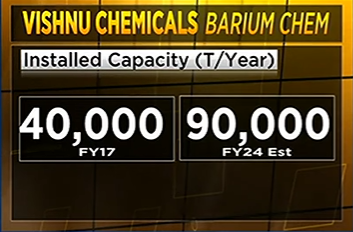

Started commercial production for Barium sulfate (doubled capacity) which goes into paints, batteries. Utilization would be 50% this year and FY25 70% and FY26 80-90%. Gross margins would be above 50%.

Chromium 10% volume growth. Barium growth will be much higher.

Looking to double the revenue by FY26.

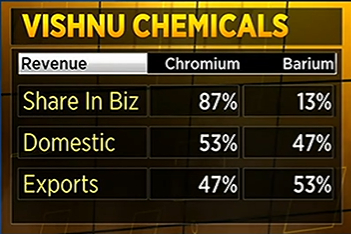

No other producer of Barium in India. It imports from Europe and China.

China is a net importer of Chromium. China is not a threat for Chromium business. There are few peers in Turkey.

Per management, China is a net importer of Chromium products. Their Chromium segment is also backward integrated. Soda ash prices have been falling, Tata Chemicals reduced prices a few times recently.

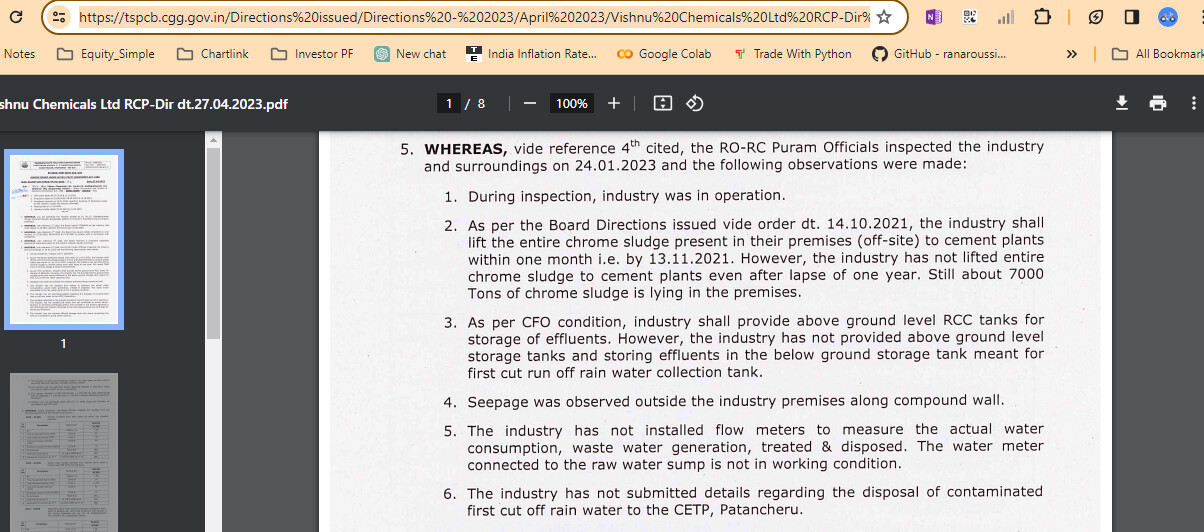

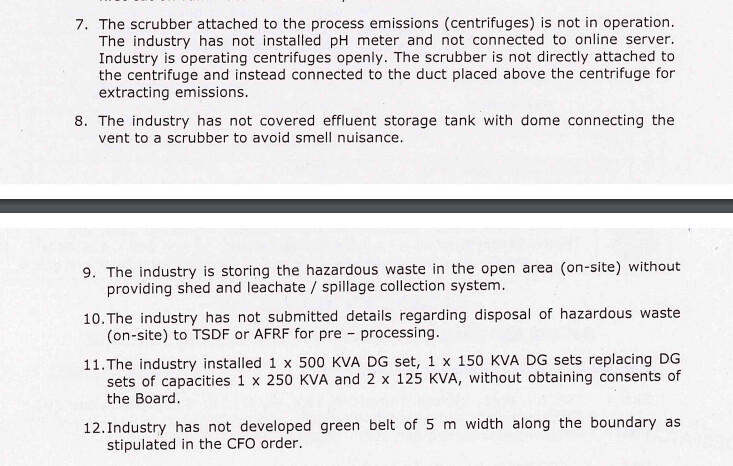

While i was reading about this company, some triggers that I noticed was a eye catching trigger for me to just be clear on the rosy picture portrayed on the other end.

Thank you for bringing to the notice. For me, compliance comes under governance ambit and it is important element especially for chemical industry. Violations here seems to be untenable.

Summary of the key points from the Q3 and nine-month FY24 Earnings Conference Call of Vishnu Chemicals Limited:

Financial Performance (Consolidated):

Total income for Q3 FY24 was 308 crores compared to 311 crores in Q2 FY24.

Consolidated EBITDA for Q3 FY24 was 45 crores compared to 49 crores in Q2 FY24.

Consolidated PAT for Q3 FY24 was 21 crores compared to 24 crores in Q2 FY24.

Financial Performance (Standalone):

Total income for Q3 FY24 was 258 crores compared to 269 crores in Q2 FY24.

Gross margins increased from 42.3% in Q2 FY24 to 43.1% in Q3 FY24.

Standalone EBITDA for Q3 FY24 was 32 crores compared to 40 crores in Q2 FY24.

Standalone PAT for Q3 FY24 was 22 crores compared to 24 crores in Q2 FY24.

Chromium Chemical Business:

Domestic market demonstrated robust demand, leading to a sales mix favoring domestic sales.

Focus on improving efficiencies resulted in a 10% reduction in average consumption of key raw materials compared to FY23.

Barium Chemical Business:

Capacity utilization in barium chemistry was similar to that in Q2 FY24.

Upgradation of equipment and infrastructure in the newly acquired baryte beneficiation plant was completed, with stabilization expected in February.

Strategic Initiatives:

Acquisition of a chrome ore beneficiation plant is progressing well, aiming to secure raw material supply chain.

Commissioned a new capacity for manufacturing precipitated barium sulphate, with good volumes sold during the quarter.

Outlook:

CAPEX for FY25 will prioritize vertical or backward integration and volume expansion.

Expecting improved performance in the quarters to follow, especially with the stabilization of new projects.

Gross Debt and Net Debt: As of December 31st, the gross debt on a consolidated level is around 320 crores, and the net debt is nearly 250 crores. The debt to equity ratio is 0.5x, expected to decrease to 0.45x by the end of the financial year.

Employee Cost: The 10% quarter-on-quarter jump in employee cost on a consolidated basis to 15 crores in Q3 is mainly due to the one-time impact of annual bonuses rolled out across the company during this period every year.

PBS Revenue Contribution: The revenue contribution from PBS (Precipitated Barium Sulfate) is currently less than 5% and is expected to increase from Q4 and into Q1FY25.

Capacity Utilization: Barium carbonate is operating at 75% capacity, and barium sulfate at 55-60%. The aim is to increase barium sulfate operating levels to over 80% and barium carbonate to over 90% during FY25.

Revenue Growth: The company expects Barium Chemicals capacity utilization to improve from Q4 onwards, aiming for 70% utilization level in the next financial year, which will increase profitability and revenue.

Future Expansion: The company is looking at adding chromium metal to its portfolio, with commercial launch expected by FY26. There are also plans to expand chrome oxide green production at the Vishakhapatnam plant.

Chrome Oxide Green: There are good enquiries for chrome oxide green, and the company is considering adding capacity at the Hyderabad facility to meet demand.

Chromium Segment Competition: The company has exhausted its full installed capacity in the chromium segment and is investing in both primary chemicals and derivatives in the next financial year to penetrate new markets.

Baryte Acquisition Benefits: The benefits of the baryte acquisition are expected to be seen in Q4, with current utilization levels at about 60%.

Revenue and Profitability Guidance: The company does not give revenue or profitability guidance for FY25 but aims to achieve an EBITDA margin of more than 16%.

Competitive Landscape: The company is facing some competition in the PBS segment from Chinese players but is positioning itself as a quality supplier with a price difference of 5-8%.

Very good summarization.

Please advise how much percentage of your portfolio invested in Vishnu and any plans of increasing stake considering it is consolidating for last few quarters.