Nabakalebar was in 2015 (I am from Puri). But I can’t understand the link between Nabakalebar and low ghee consumption.

Thanks Raj. Yes there is a connection. People do fasting in these days which lowers the ghee consumption by the households as such. But, again if I am not mistaken, the MD used to tell that the ghee consumption is more in temples and like. The durga ghee is a cow ghee which is generally used in temple rituals. If that is the case, then the scenario should be opposite. But, I am not sure on this.

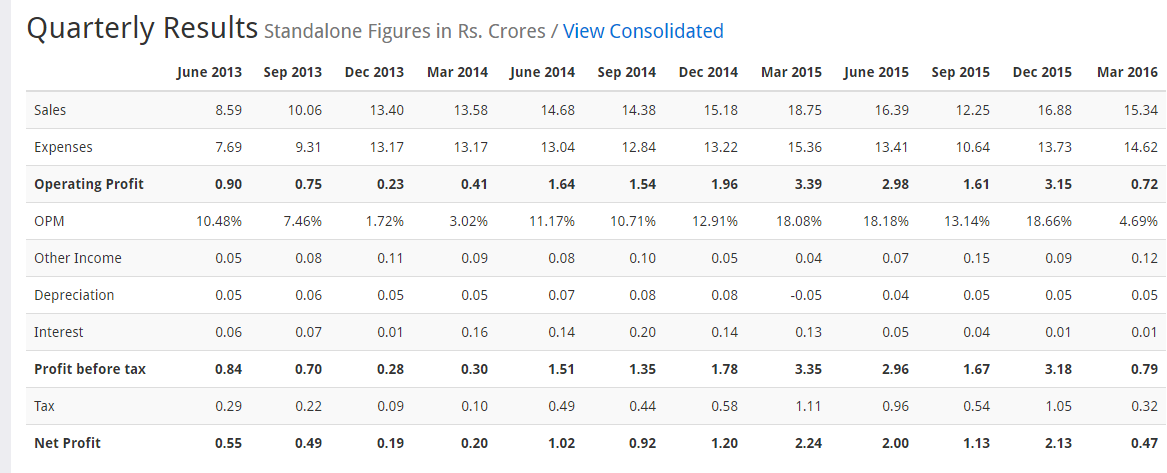

Even though we discount one month for Adhik Masa and the 7 days for Nabakalebara 2015 which according to wikipedia has started from 23 rd march; the growth is sales is almost flat. What about the other 10 months and 23 days - especially when a company has Durga Brand with it !!

Safe to avoid.

1 Like

Virat have two two brands Durga and kamdhenu ghee (cow ghee); refer .:: VCIL ::.

Also refer their 9 months(Apr15-Dec15) growth is reasonable; nos. from screener

Disclosure : Not invested

Thanks MHS. Ya I knew that they have two brands but forgot that Kamdhenu deals with the ghee needed in Pooja.

But, the performance is bad if we discount the impact of festivals also. These is a negative top line growth !!

The last Nabakalebara was in 1996, a good 19 years before. So, I doubt there is enough past data within org. to say that, this is a trend.

Plus, Karnataka foray was also there in the year. So overall, struggle for sales growth isn’t a great sign.

Disc: No holding.

3 Likes

The Sept Qtr. results have finally shown some traction atleast in terms of Sales. Perhaps companies like Virat Crane need to be given a slightly longer rope! It sure operates in an exciting space & could be a potential winner in the long run. I had lost patience & exited a few months ago as the numbers were not forth coming. Perhaps time to take a closer look again!

The Co. brings back fond memories of my visit there. It was a bit of an effort _ Mumbai-Hyderabad-Vijaywada & finally Guntur! The fact that I was accompanied by two of the smartest “Young Turks” in Ravi Teja Rebba & Abhishek Kulkarni, fellow valuepickrs, who had the courage of their convictions to give up regular jobs in the pursuit of their passion of being full time investors, made it a great learning experience n we had a lot of fun!!

8 Likes

Results of 4th quarter

Disclosure: invested

I had a question regarding Virat Crane which has been bothering me for a long time.

The reason people got interested in Virat Crane has been that its a dominant brand in Andhra and has done well in Orissa too. With plans to expand into new value added products and geographies, if it succeeds in other states too, then it would grow into a much larger company, thereby creating wealth for the investors.

I see a fundamental flaw here based on my experience with organisational growth projects. Though it makes perfect sense to get into other value added products to take benefit of strong brand name in its existing markets, I have serious reservations about the geographic expansion.

Their flagship product is ghee, which is undifferentiated, except for some quality differences which many others can guarantee. In the absence of a strong product, other aspects like promotional activities play an important role for creating the pull. I don’t think they have such deep pockets to go all out advertising. In Andhra, the brand got built over a long period and could have been due to the good will of the promoters also to some extent. The same doesn’t apply in other markets.

In such a scenario they will have to create retailer push for products, which means schemes and more sales force. Even if they grow their revenues, I doubt it will be a very profitable growth. Which further means limited promotional expenses compared to deeper pockets.

I therefore see a very very long gestation period before company can gain solid traction to be on a long phase of profitable growth resulting in “substantial” value creation.

Would be glad to hear what others think.

1 Like

I haven’t researched about this company nor aware of their recent developments. Yet,

- I am from Guntur, never heard about their products since childhood --> Poor branding or advertising.

- Generally we get ghee from wholesale market which is good and cost effective --> Like Metros, supermarket culture is not big in Guntur. People generally go to wholesale market where you can buy veggies and grocers at lower cost.

- Heritage foods is Andhra CM’s business .They are moving into value added products. Due you guys believe Heritage will allow Virat to outshine ? --> Competition

No investment in Heritage or Virat.

1 Like

There is no need for another trad on this but let me just say a few things:

- I like the management

- I like the products

- I like where they are located(Cattle rich and water abundant location)

- I like the fact that they are local and not omnipresent like the biggies

- How can you compare it with any other FMCG company, this is a commodity with a brand on it, its a service not a Value add

- They are ultra micro cap in nature

- There are strict Circuit filers on quarterly and yearly level, hence cant trade randomly.

- Can be a future take over candidate with geographies expand there, if not can grow organically in itself too

1 Like

Few Observations:

- Promoter holding high at ~73%

- RoCE of 25%, RoE of 18% (and that too depressed due to legacy issues in the balance sheet)

- Negligible debt

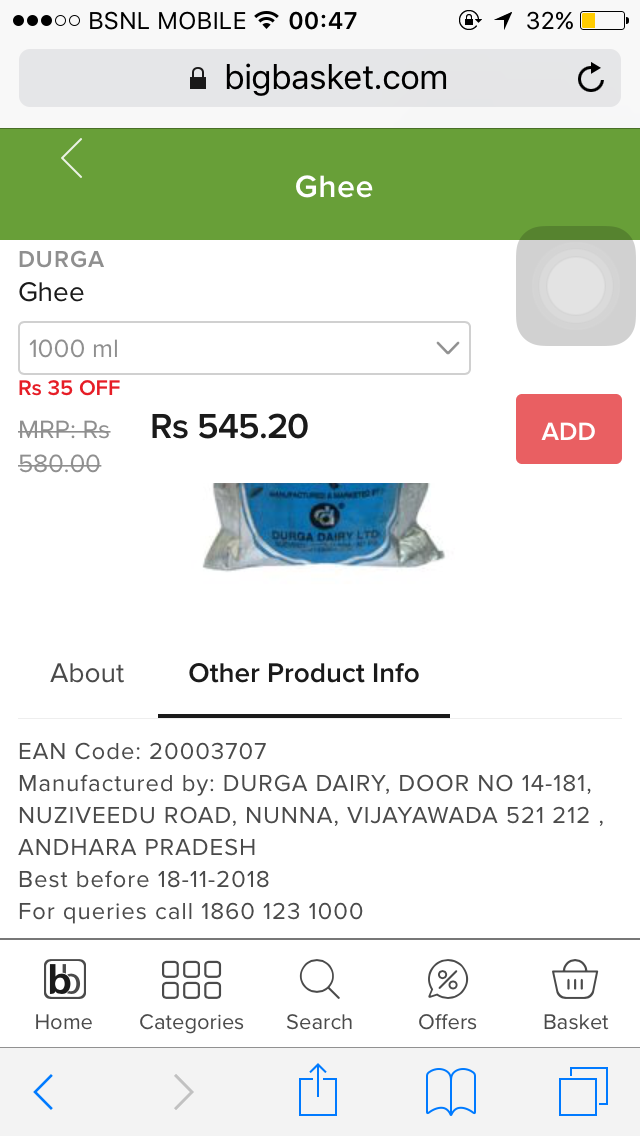

- Selling most expensive ghee in its geography(from bigbasket.com)

- Very comfortable cash conversion cycle of less than 10 days(from Ratestar.in)

- Launching new products

- Dividend paying with decent payout (although company is in investing mode)

- Latest balance sheet shows capital investment……may be to enhance capacity

- Rising raw material price (i.e. milk and its derivatives), proper succession planning and failure of new products might be risk here

1 Like

Is this the same company or different company.This snapshot taken from bigbasket Guntur Vijayawada region

1 Like

It’s the same company

1 Like

Hi, anyone has any updates on the company? Is the current price attractive to buy for long term … @chaitu

1 Like

@brijeshmahawar @suns @evicky @csteja @cathene @RajeevJ @zidane @richdreamz Are you still following the company?

https://beta.bseindia.com/corporates/ann.html?scrip=519457#

Q2 FY19 Results does seem ok, no growth seen QoQ. Without management / investor presentation its difficult to understand what is going on… Any insights appreciated…

QoQ Sales declined slightly, but net profit is flat. EPS is flat.

H12019 vs H12018, slight increase in Sales, good increase in net profit and EPS.

1 Like

Volumes have started increasing in this counter.I think value buying is happening in this stock.

1 Like

Loans to related parties is a big negative. These loans are interest free also.

1 Like

Any further updates on Virat?

1 Like