There are many forms of faking something Let me explain,

There could be some, who probably make duplicate copies of Durga packaging and sell god knows what in that package there by damaging the original brand. VICL can act against them as they have genuine case.

However another form is, seeing the success of Durga packaged ghee, there are competitors who have launched packaged ghee with similar sounding names. Like “Devi Durga” ghee here. The adv. features one of Odia film super hit heronie from past. https://www.youtube.com/watch?v=xpFdKs0ncdo

In such cases, it probably takes offer of higher incentive to channels to stock it. Which maybe relates to your second point about dealer network not stocking Durga ghee.

For customers, maybe the durga brand recall isn’t strong enough to postpone purchase or go looking for it to other stores when it’s not available in one store.

This form of competition is hard for Durga to do anything about except spending on A&P which we can expect to be matched by the competitor.

Overall, it’s probably a decent business not a superlative one

Yaar, why only compare PE’s between higher ranked players and expect/hope the smaller players to catch up. We need to put other things like comparative Returns on Equity, Asset Turnover, Working capital management, payout ratio in the perspective as well ?

Hey Raja, my assumption of PE re-rating is mainly because the financial metrics for Virat are second to none and are superlative (though on a small base, so it remains to be seen if this can be maintained). Also, I have reported issues with the story in my earlier posts in this thread.

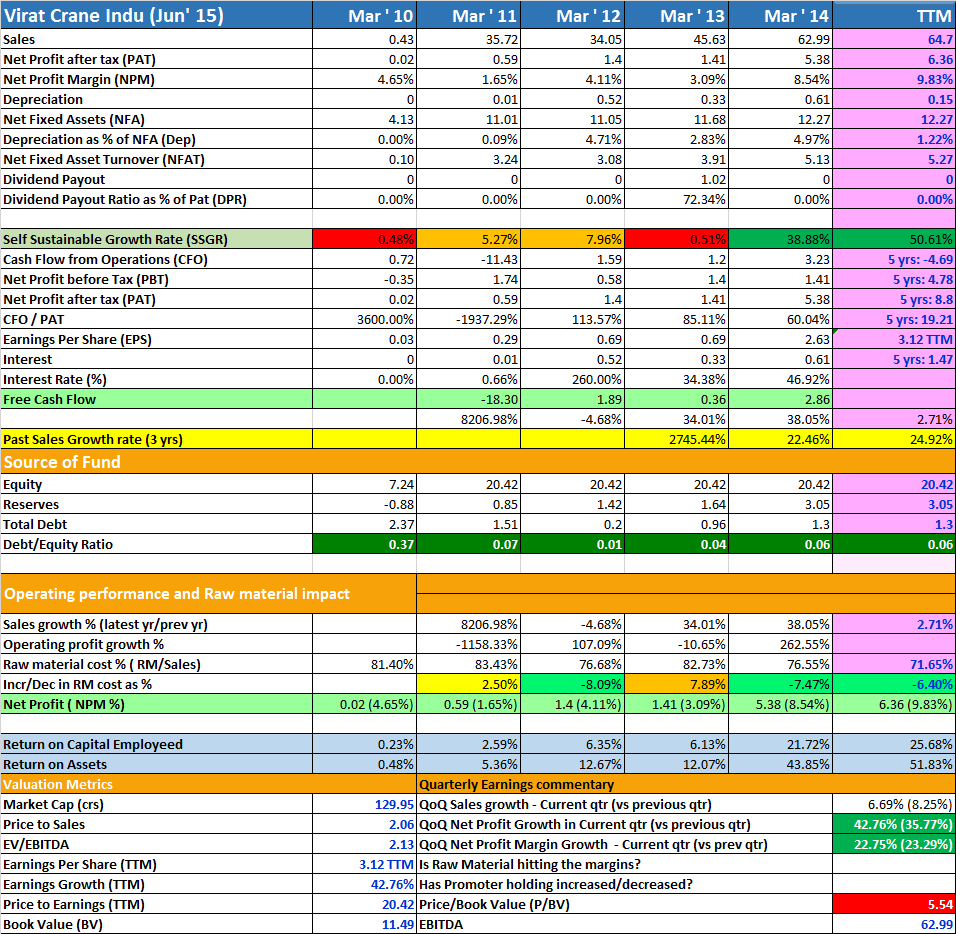

RoE and RoCE of 30% and 50% thereabouts for FY15. (there are intangible assets of 10 crore which you need to adjust while calculating equity as this came as good will from Durga Diary acquisition). That’s how I calculated.

Net Fixed Asset turn over of more than 25 (62.98 crore revenue/2 crore net fixed assets). Not capex intensive.

Dividend pay out of 40% in FY 15 and more than 50% for 2 years before that. The 50% dividend is on a much smaller base, so let’s not give that much importance to that.

Inventories as a %ge of revenues for FY15 is only 6.5%.

Negligible debt.

**

Disclaimer

My holding bias may be the reason behind my positive rant, so please do due diligence before any buy.

Anyway, I should stop here as too much positive bias may lead to members getting positively influenced whereas they should take decision starting from neutral view point and drill down based on facts.

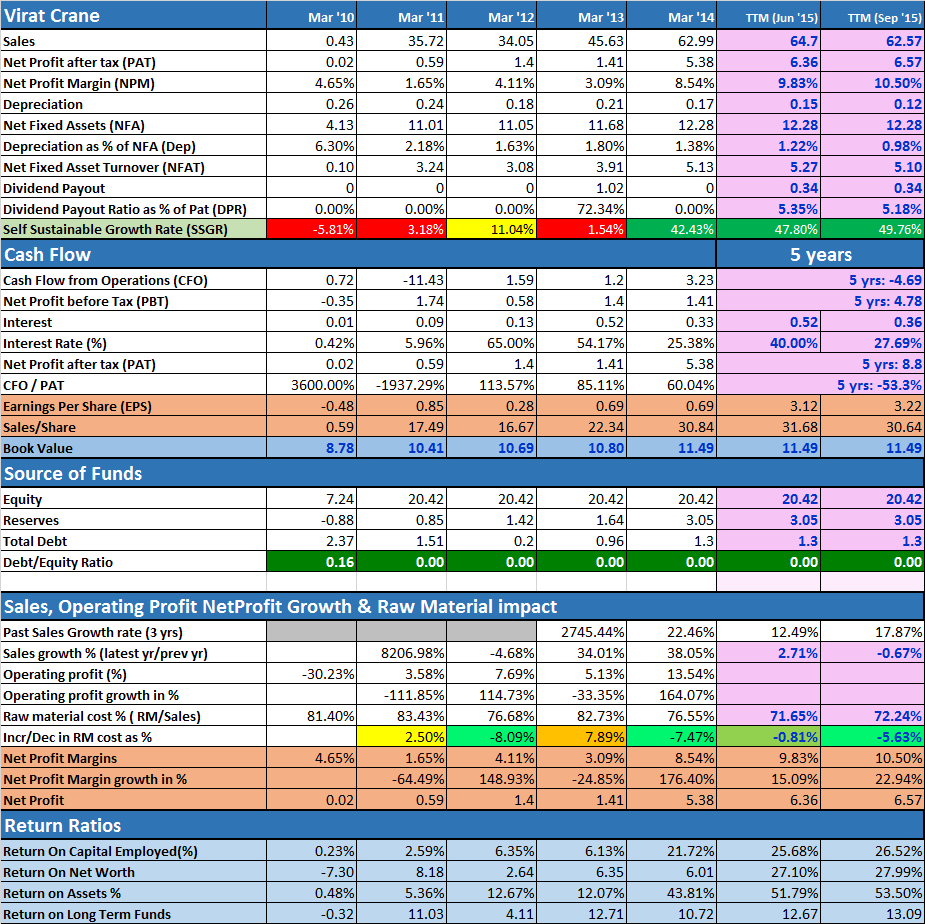

Virat Crane results were declared and they are a bit subdued on the revenue growth front. This could be due to lesser MRP per packet compared to last year. The reduction in milk prices could have been passed to the customer. This also means there could have been not much volume growth.

However, as expected the raw material costs have come down and though the revenue was lower by about 10% YoY the Net Profit grew by 22% YoY.

HALFYEARLY ANALYSIS:

For such a small company, the quarterly earning may not be a right approach as the growth would be lumpy.

If we look at Half Year metrics, the Revenue growth is flat (29 crore vs 28.6 crore) so indeed there is a bit of volume growth (7-10%?) and the net profit (EPS) growth is 61%.

Other expenses are a bit higher which I think could be due to expansion activities in Karnataka (?).

Balance sheet is strong though and finance costs have dropped by a lot when compared to the balance sheet size and the company is practically a zero debt company except for working capital requirements.

@richdreamz I think if company has reduced the MRP then things get shifted to Volume front. In last 2-3 years, sales increase was result of increase in milk prices that overshadowed the volume game.

If milk prices stabilise (that we’re noting in the current year) then its a reason to worry for company unless they grow through volumes. I just want to know what is our volume growth visibility.

@Apandey My assumption is that volume growth has come about as mentioned above if we see Half year comparison. Also, I read in blogs that some one off events in both AP/Orissa like back to back “adhika ashadam” has played a role in lower sales growth. I cannot corroborate but I buy the logic as I myself has experienced this lean marriage season during casual family talks.

Basically, this is an undiscovered story with no institutional interest. With name “Virat Crane” no one expects it to sell an FMCG product with an excellent brand name ‘Durga’ and sticky consumers towards this eatery. On top of this, improving financial metrics and possible sales growth (due to volume growth) due to new plant in Orissa and Karnataka foray. As this is a micro cap, quarterly growth would be lumpy and we need to give time for sales growth thesis to play out. Again, I hold the stock so take my opinions in this context.

Some updates straight from the horse’s mouth (Virat’s management) post Q2 results as updated by a friend who spoke with management:

The reason behind sales de-growth is due to 2 months inauspicious period between July mid to September mid which comes once in 12-19 years and with no festivals/marriages etc Ghee off take was low… So sales were lower by 30-35% in Q2. This is both in AP and Orissa which was a double whammy.

Pent up demand will be seen in Q3/Q4.

Orissa production plant is in progress to start production by Q1 2017. The land is already procured and there is little CAPEX needed. So the incremental RoCE will be very high.

Karnataka foray is on track through the already established Crane Betal network and the response is good.

Management has started concentrating on Durga brand to make it a well established regional player. All the efforts will pay huge pay offs if story goes as per thesis. It is already a premium player locally (Ghee sells at 20% premium to Amul/Heritage Ghee etc. with little or no discounts.

The return ratios are improving and are best in the diary sector.

In my opinion, due to better financial metrics and pristine balance sheet, sticky nature of the FMCG product, brand power, high dividend payment the company deserves better valuations.

Disclosure: I hold Virat as indicated earlier. The details are already available publicly in internet.

Ok, I have been going around retail stores (More, Vijetha) in Hyderabad to see the shelf space Durga ghee occupies and to get product feedback. Overall I have been getting unanimous replies from the store members that Durga is the choice if you want a ‘nice’ ghee.

Yesterday, I wanted to see if Durga has any shelf space and to enquire the feedback of the ghee in a posh area where typically the people are from middle class/upper middle class and are generally informed of the product choices they make.

I have been to ‘Hyper City’ mega mart located at Inorbit mall, Madhapur - the posh area this side of Hyderabad. I was pleased with what I saw.

Durga shares significant shelf space equal to Amul! (Second pic below, 3 rows each). As per store members both Amul and Durga sell but Amul might have a slight upper hand. Here too the lady said, but sir, if you want a nice ghee, go for Durga. I thanked and came.

Key conclusions are:

Management really are doing what they are upto as Durga started having better brand visibility when compared to couple of years back.

Having equal shelf space with Amul in a super competitive retail market is a feat. With time, this should contribute to revenue growth.

In the local area stores, there are imitation brands like ‘Nand Gokul’ (Nand Gokul copies Durga packaging as is except for hologram, Crane Group Logo) which shares shelf space with Durga BUT in the Hyper mart, there is no such competition from local imitators.

Ok, so brand visibility is improving, with time the sales growth and its associated disproportional bottomline growth (due to high RoCE, Low Capex) should pan out.

I hold Virat Crane and this is not a buy/sell suggestion. I’m just doing the ‘brand visibility’ scuttlebutt to confirm that product exists and sales do happen really as part of my conviction building process.

EDIT:

If you zoom the second picture, you will see the prices of Amul and Durga ghee. Amul sells at 385 INR per KG whereas Durga Ghee sells at 465 INR per kg which is 20% higher, which is huge premium. This ought to tell us something apart from high quality/aroma of Durga Ghee, what is that?

P.S: On a lighter note, I took my family saying its a surprise outing and they don’t know the main reason is my scuttlebutt thing, thankfully, my wife does not read the forum yet

Appreciate that you liked the ground research, I have observed further points but refrained from posting as I’m not sure how forum members will take my frequent postings on this company as there is thin line between genuine and passionate research and misunderstanding my intent as I hold the stock and is a small cap.

Anyway here you go,

If you closely observe the second pic last but one row and extreme right, you will find packs with 2 different colours, 1 in light blue and another in darker shade (which is the colour of all other packs). The light blue ones are old stock from July 2015 while the darker ones are from October 2015 stock - I have checked. To keep away the competition copy cats which came up with the lighter blue shade packaging, Virat Crane has come up with better packaging and labelling - my guess here.

The point I’m driving here is a) management is forth coming and proactive in generating sales. b) Product sales are moving and very less/no 3 months old stock in retail stores.

Not sure if this is covered already, but there is no or less %ge discounts given on Durga Ghee while adjacent other Ghee companies offers freebies, more discounts but Durga ghee sells.

I’m assuming this aggressiveness is a recent phenomenon which will bear fruits in future in terms of sales growth.

New website of Virat Crane (Durga Ghee) - though not perfect, nice attempt, positive moves:

Absolutely nothing wrong with frequent postings…the research u r doing is great and other investors would be highly grateful for posting your views on the same…

even i got a very positive feedback about Durga ghee from some businessman who stays in Andhra…he was positive not only on the brand but also about the management … he told the promoters are good and doing good business…

Good discussion , this looks to be good story so far. but in their cash flow statement, Cash from operations is quite low when compared to their profit. What could be the reason, don’t see any major spike in their debtors as well. Am I missing something here ?

A big fake ghee syndicate has been arrested last week in Vijayawada, Andhra. The below video explains this, however the video is in Telugu. However, through visuals, one can understand that they sell predominantly Durga ghee to the regions in Vizag, Orissa etc.

The video indicates that genuine brand owners heave a sigh of relief with this large scale fake mafia has been found and stopped.

As I understand,the product is such that it should not be very difficult for competitors to replicate the quality.Therefore their success hinges upon effective marketing and distribution.Based on their annual report,the company is heavily focussing on branding.In Andhra,Telangana and Orissa the brand has good traction because of many years of branding.In my opinion it would not be easy to enter new markets and become and instant success (because of little difference when compared to products of competitors who are established local players). @richdreamz I was inspired by your field work and thought I would also check it out for myself.I went to a Reliance Fresh store and found that Durga ghee is placed at the eye-height of the customer while other brands are placed lower down.Durga ghee seems to get better visibility.

To an extent yes there may not be too much in terms of product differentiation but Durga ghee is liked by families for its aroma and quality. I did not dig too deep into what exactly is the difference in terms of product, am sure each company will have its own ‘formula’, though essentially the end product is ghee.

Now coming to brand differentiation, the below 2 factors may be their USP (regionally, at least)-

Better visibility in retail stores - Tick. As per your and my observations. Discussed in some of above posts as well.

They came out with 2 really good regional TV ads, one is already shared in one of the above posts which is for Durga ghee itself and the other belongs to Crane Betel nut, which is one of their group companies.

Crane betel nut ad

(The advertisement is very catchy for telugu people with its tune and universal applicability and has “who is who” of TV industry and elders from Telugu film industry). Each and every artiste appearing in the ad is a well known name in their respective industries - almost.

Now, a thought occurred to me, in this ad, just replace the “Crane Betel Nut” with “Durga Ghee” and the advertisement will be equally applicable!!!

Durga Ghee advertisement

I did not see the ads recently though on TV, however, Crane Betel Nut has been sponsoring some programs in telugu TV channel ETV, they got a 10 pm slot I believe.

In marriage and festival seasons there is huge demand and sales for Durga Ghee. Its a monopoly brand in most of the places in Andhra ( I’m from A.P.) There is no competitor for durga. But some people prefer VIJAYA brand also which is to be bought from VIJAYA diaries only. I personally inquired some sellers about the sales and got positive feedback. The present quarter has some auspicious Hindu festivals as well as marriages till December. So definitely there will be some growth in top line.

And according BSE capping circular what is the minimum and maximum price it can move in Nov, Dec. (I am a SIPper. Will accumulate more)

Thank you.

This is my first write up. Welcome positive criticism.

Disc: Invested at 58/-

thanks Ravi for the update…how is the brand visibility & demand of other brand of the company “Kamdhenu ghee” …which i think is cow milk ghee… & Durga Ghee is for buffalo milk ghee…

Hi Abhishek, I see Kamadhenu ghee also besides Durga but the shelf space is limited and also the packaging is not as attractive as Durga ghee.

The packaging is white in color

Cow ghee is used for pujas at home, temples etc. so I believe it’s not as much consumer product as Durga is

I do not know what %ge of sales are split between Durga and Kamadhenu but I surmise lion’s share is taken by Durga ghee itself.

Since this is for pujas, not sure how brand conscious would people be, they would most likely buy ‘any’ cow ghee except for may be someone who wants a particular brand.

Since Durga ghee is made to use sweets, mix with baby food, people want best ghee (for kids), tasty ghee etc.

These are just observational thoughts on cow ghee and not much research/enquiry has been done.