Yes Saurabh, please elaborate, I am heavily invested in VEL. Not able to fully understand your message.

He means pay close attention to cash flows. P&l can be easily manipulated and does not narrate the actual position of the company. Look at balance sheet and cash flows and working capital efficiency.

1 Like

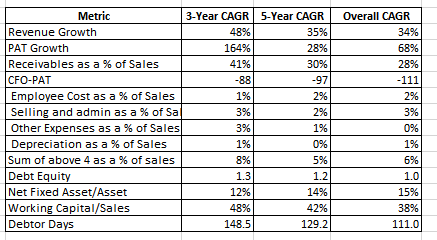

P&L statement at the end is an accounting treatment So, it MAY or MAY NOT be real cash profit. So, it is important that PAT is real cash profit and to what extent it is real cash profit is reflected in Cash flow Statement. The other part is how is this accounting profit (PAT) or cash profit is being generated. This is generated using items in Balance Sheet.So, we need to see how balance sheet is getting strengthened or worsened. Now I will just give some ball park numbers to chew:

I am highlighting few questions below now. It is not a verdict but highlights the risks one carries and must deep dive in annual reports for further clarity:

-

The revenue growth and profit growth (as per P&L) looks stupendous but so is receivables which raises the question “are these real revenue or mere accounting treatment”?

-

If revenue and profits are real why there is so much mismatch between profit and cashflow from operations

-

Neither receivables have improved nor working capital intensity. So, mere revenue growth and PAT growth is useless. It will continue to be accounting profit company but not cash profit

-

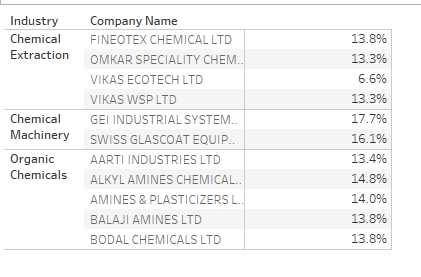

Now comes the best part. sum of employee expense plus selling and advertizing expense plus other expense plus depreciation is 7 %. I am providing below respective numbers of other companies in this industry as same metric(i think employee cost was highlighted above in thread but when i tried to look, the issue was spread across multiple expense items)

Do not numbers for Vikas ecotech look totally out of order. What kind of assets have 1% of depreciation, I mean this is height. So, this is such an so called ASSET LIGHT MODEL which does not have much assets which does not have key expenses anywhere comparable to peers. looks like they are either in trading business or mere penting up numbers because asset light businesses do not throw such balance sheet and cash flow numbers.

5. Look at net fixed asset to total asset ratio, the long term range is 12-15%. So, when no hard assets are being created, where the huge leverage is going off (look at debt to equity ratio). What kind of business model is this?

- After all this, even if one assumes, business is genuine , so the latest valuation is out of latest PAT margin which is around 6%+. This has come totally from gross margin improvement. Now, with all expense item being uniquely low among industry, I do not see how employee cost + selling and ad cost + other cost + depreciation can go down further. This means the day raw material commodity cycle changes, PAT margins will go for toss because I dont see why they will have a bargaining power. So, while one is paying a price for this company, in valuation what kind of PAT margins one is taking.

Historically, if one analyzes companies where people have lost bulk of their money (educomp, treehouse, core project, tanla etc etc etc the list is so long as Kedia jee says 80% of market is bhangaar cap), Many of these characteristics depicted above have been common characteristics of the list mentioned and hence think these points are enough for me not to spend further time on this. This is worth a good academic study on where not to invest. Will cover this in some detailed blog soon once go through AR as a part of academic study.

Note : Views above are personal opinion based on macro level analysis and I may be wrong in my analysis in case the business is trying to something uniquely different which cant be captured in above metrics. But we live on probability ![]()

14 Likes

suru27 http://forum.valuepickr.com/u/suru27I appreciate your detailed

financial analysis. You are taking of past ,which, of course, is very

important. Let us look at the future - Vikas makes a chemical which will

replace the lead based chemical used in manufacture of water pipes. Govt of

India is expected to pass a law which will ban use of unhealthy lead based

chemicals in PVC water pipes used in buildings. As soon as the law is

passed the demand for the their product is likely to shoot up. Pl check the

concall notes which I had attached earlier.

This is the real expected game for Vicas Eco tech - if it worked out it

could be a multibagger - else a bhangaar stock.

One of his major clients, using his chemical for manufacturing PVC water

pipes, had invested about 7 Cr, about 1-2 years back to get equity

holding in this company, If it was a genuine deal then it indicates huge

trust in the company.

Next 2-3 quarters will reveal all - either way. I have no great regard for

the management - which is still to prove itself. We need to keep a very

close watch.

1 Like

A kutchhi businessman can rarely be wrong !

1 Like

Also Mr. Anil D Gala promoter of Navneet Education, having close family connection to Prince Plastic Group holds 49 lakh shares of this company.

Respect your thoughts. Personally ,if I can’t trust the past,I can’t trust the future .

Went through annual report from 2010 to 2016. In 2016 , the company mentions R&D focus at least 30 times with whole strategy around R&D. What are the R&D expenses in last 5 year : 9.5 Lakh on an annual revenue base of 200 cr  . Flashy annual reports, when specialty chemical sector picked up , use specialty chemical on front page, change name of company to latest buzz words.all typical signs. I ve not yet gotten into where money is going and how many subsidiaries companies are getting formed but will soon post views on that too. Just condolidatoon the info .

. Flashy annual reports, when specialty chemical sector picked up , use specialty chemical on front page, change name of company to latest buzz words.all typical signs. I ve not yet gotten into where money is going and how many subsidiaries companies are getting formed but will soon post views on that too. Just condolidatoon the info .

By the way about the customer buying shares in company, read a book called financial shenigenains on such way of juggalary too.moreover, one should buy based on own research not because of someone else. For example, a Goldman Sachs has also been part of dubious entries,so, these r nothing

4 Likes

Please note the above company is a different entity

2 Likes

I think market is looking at the time line given by NGT for banning of Lead stablizers, which was earlier announced in May-17 and 6 month grace period has been given to Govt. to implement the ban. I think there may be some news regarding it. Vikas ecotech management has told that it will be a gradual shift but i think organized will do there bit in advance. I think what we anticipate the market of Organotin stablizer is only a tip of the iceberg in long term because many other products like drainage piping, water tank and other PVC product use to make food containers.

Discl: Invested from lower level.

Higher receivables and lower expenses could be due to the trading business that it has. The de-merger of trading business (expected to complete soon) could provide better clarity in next few months.

1 Like

Company recently (on 8th January 2018) announced introduction of new range of eco-friendly Calcium-Zinc heat stabilizers for flexible PVC applications such as cables, soft hoses, toys, healthcare products, etc.

Trial run of this product began in December 2017 and commercial production to begin in February 2017.

Further company today announced Intimation of Analyst/Institutional Investor Meeting with Axis Bank Mutual Fund, Mirae AMC and SBI Mutual fund over next two days.

Expecting some buying to come in this counter soon and expecting price up move.

Expecting better results from the company in the coming few quarters.

Disc : Invested at 35 and added some quality recently at 45. My views may be biased, but i am expecting this one to be a multibagger in 1 year’s time.

1 Like

When is the Demerge of Vikas Ecotech business divisions will happen. Is record date announced? Thanks

Rudra Shares has initiated coverage on Vikas Ecotech on 12 January 2018 for long term with a view for 3 years.

Read the entire Report @ https://www.rudrashares.com/Downloader/DarkHorse/VIKAS%20ECOTECH%20LTD.pdf

Disc : Invested since last few months. Plan to add more on declines.

Hi i m new to forum.And i am following Vikas ecotech since around a year.I would like to get the research report on my mail id.The one you shared with the Chinese guy.

Summary

1 Like

Dear Abhishek,

FYI

-Had gone through Vikas ecotech founders and management.The core founder of Vikas leasing is and in not wrong father of Mr Vikas Garg is polically connnected and 4 times MLA from one of the consituency in Delhi and he related to current ruling government in centre since long.The family also runs one prominent academic institution.One famous publication house is also being run by the family/promoter group.

Further one of the independent director of the company Jagdish Capoor is ex Deputy governor of RBI and ex chariman of top private bank.The founding company Vikas leasing was in NBFC sector and lease and finance business in around 1980’s which shows the strong connections of the group.

-Recently Prakash industries came into news for SEBI banning the company from trading due to stock manipulations from bourses.Now at one point of time of Vikas leasing limited co used to deal in Prakash industries as one of the client and also if am not wrong the founder of Vikas group is one of the main guys and director in Prakash industries.Ace investor Rakesh Jhunjhunwala is also a investor in Prakash industries.

-Currently evoting pertaining to shareholder resolution is going on in Vikas ecotech.The resolution is pertaining demerger of ‘Recycled compound and trading division’ into Vikas multicrop limited.Would like to know whether the same is beneficial for overall growth of the company?p.Attached below is link of board presentation on Demerger scheme

Below link pasted pertaining to credit rating by CRISIL date 7-Dec 17.The rating also takes into consideration its demerger of trading division into Vikas Multicrop limited.

CRISIL rating.

AS114.pdf (339.6 KB)

Hi,

I have been following vikas ecotech from Level of Rs 19 and invested from 19 levels and still holding.

On 09.02.2018 , In Lok Sabha in question round, the top of Lead ban on PVC is taken up and please find the answers given by MOEF.

Soon the ban is going to come and expecting tigger for the stock and more media coverage.

3 Likes

Q3 results on 14 February. That can also be a good trigger for the stock.

MOEF decision is still pending. Let’s hope for the best.

Trigger is one thing…it presents an opportunity. After that it is up to the company and the management how they want to capitalize on this. That will decide the way the stock moves in the next 3-5 years.

Discl: Invested

Hi Darkwanderer79, did you read my attachment AS114