Hrishikesh Kale,

It could be a Debt capacity + Cash bargain stock (applying the concept studied under Sanjay Bakshi). They can borrow at 12% ( Crisil AA- rated!), if I assume they can take a maximum debt which will yield an interest coverage of 3 (margin of Safety), they can borrow a debt upto 97 Cr. (EBIT/(Int.Coverage * interest rate). This when added with the current cash + investments could put the company at a potential of 297 Cr which is 5% higher than current market cap. (But this is too small a difference)

The company is available at a bargain price. If I take the FCF of the past 5 years, and assume no growth in the FCF for the prolonged period, discount it at 15%, I would get a value which is 380 cr which is 33% higher. Else, if I discount it at 20% I would get around 278 Cr, which is similar to the current range.

Catch here is the assumption of no growth. Will the firm be able to grow FCF at higher pace than 0% in the future? We need to be certain of that. This is one crucial question to ask, because, the companyas current valuation is dependent on discounted cash flow of future valuations!

http://www.textileworld.com/Articles/2004/September/Fiber_World/pictures/p71_Copy.jpg

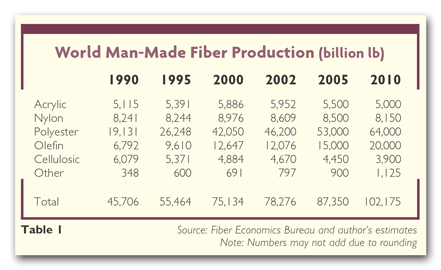

Based on the above table, I see the acrylic fibre is not such an attractive option for growth in the past 20 years. The consumption and production hasnat grown over the past twenty years. The trend and the climatic condition could only result in the fibre consumption and production to increase. Also, China is planning huge investments in the space, which could result in supply overpowering the demand, by which the prices would be subdued. But I believe the companyas major source of income comes within India. Indiaas market is slightly deviating with respect to the global markets, but when there is an over abundant supply, there is a great chance the products from external markets coming into our country. In such a case, the competitiveness within the industry would increase, which too is not attractive.

Some other questions too I have considered exploring while looking at the companyas numbers, they are,

1)** What expense contributes the most for determining their margins? The Operating margins, seems wavy**

Margin reduction can be two folded, the price reduction or cost increase ( or both). Prices within Indian Acrylic fibre didnat decrease because this industry is growing at a higher pace than international peers, and there is a demand for the fibres, which results even in imports. Prices needs to be competitive, as low priced imports comes into the Indian markets. The cost increase might not be due the plant operations, as they might be operating at higher capacity utilization. Some external factors which determine the costs are,

Raw material a Acrylonitrile prices are directly proportional to Crude oil prices

Devaluation of rupee& reliance on external sources for procurement of raw materials

In the current context of falling crude oil prices and depreciating rupee, the companyas position is, I believe, wouldnat be much positively benefited this year. Anyhow, with the current industry structure, it is anyways better.

2) How are they generating more revenues, if their net block seems reducing every year? Are they due for an investment cycle?

They are not investing in expanding the capacities at all. The reason is unclear. In edelweiss report, it was mentioned that 20000 MT is the capacity of the plant. In the latest annual report they have mentioned their production during the current year is 20478 MT. It could mean they are operating in the shifts, as they have made no investments in capex. It could also mean that their plants and equipments would depreciate faster than they can anticipate. With such a condition the company would have to invest in the maintenance CapEx continuously, so that they can continue to operate at the same way. I sense a maintenance CapEx spends such as, replacing machines/equipments etc., would increase in the upcoming years, reducing FCF. A capacity expansion in this industry which is degrowing or growing slowly would only be detrimental. That would explain the following,

aAll management does is to be fairly interested in buying and selling of mutual fund/bond based investment vehicles.a

Summary:

Share valuation wise attractive. The opportunity for growth in earnings and Cash flows? Yes. But I am not sure on the sustainability of it. Hence, If I am investing, I would probably invest for the bargain it offers and expect to get something like 15-30% increase in valuation. Nothing more, nothing less. J

{kind=link}