VARDHAMAN TEXTILES

DATE – 02 FEB 2018

Industry :

Over the last decade, the global textile and apparel trade has been growing at a CAGR (compound annual growth rate) of 5.6 %. In 2014, it stood at US$ 820 billion. Apparel categories had a larger share of 56% while textiles had the remaining share of 44% in the overall trade. The global textile and apparel trade is expected to reach US$ 1,600 billion by 2025. It is projected to grow at a CAGR of 6.3% over the next decade. The Indian textiles industry, currently estimated at around US$ 120 billion, is expected to reach US$ 230 billion by 2020

Textile plays a major role in the Indian economy. It contributes 14% to industrial production and 4% to GDP. With over 45 million people involved, it is one of the largest source of employment generation in the country. The textile industry accounts for nearly 15% of India’s total exports.

Company :

Products – Fibre, Yarn, Sewing threads, fabric, garments.

They have presence in markets like the European Economic Community, Canada, China, Japan, South Korea, Mexico, Brazil, Mauritius and the Middle East. Also emerged as a preferred supplier to global garment makers like Tommy Hilfiger, Esprit, Gap (including brands such as Old Navy), Zara, H&M, Mango, Benetton and Arrow, among others.

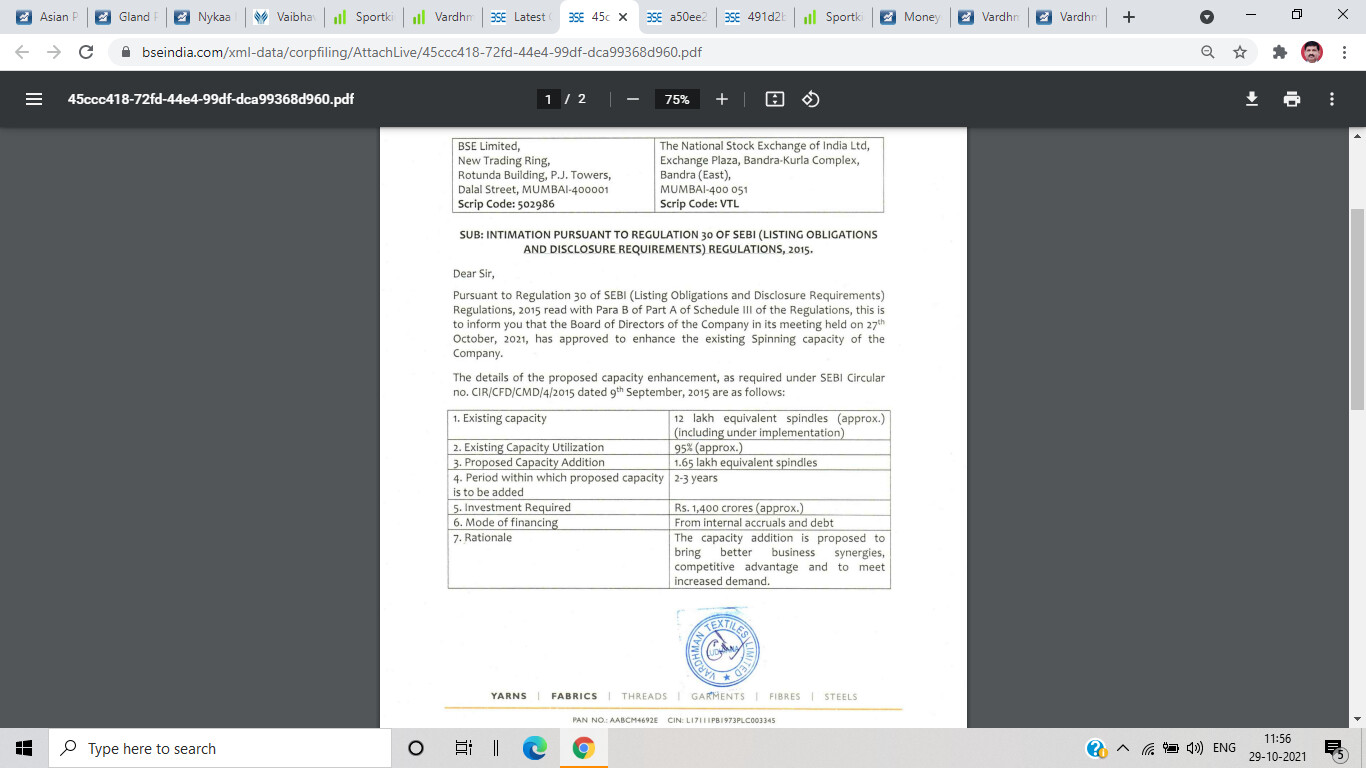

Future - Currently, they operate at near 100% utilisation levels in the yarn business, catering to diverse customer requirements. They are also consolidating the fabric business and are focusing on expanding capacity in this space. Going forward, they have a planned capital expenditure of ` 2,500 crore over three-four years towards the ongoing schemes at Baddi, Himachal Pradesh, as well as proposed expansion in Satlapur and Budhni in Madhya Pradesh and modernisation in other units.

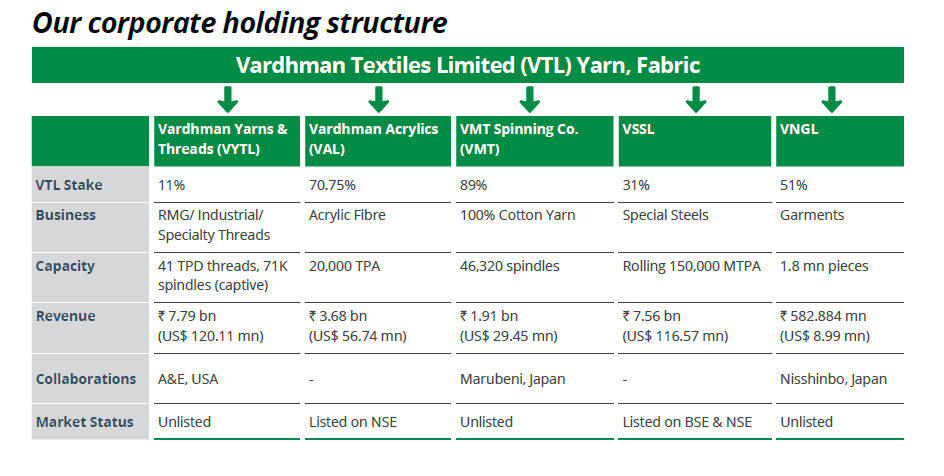

Subsidiaries, Joint Ventures and Associate Companies:

-

VMT Spinning Company Limited (VMT): This subsidiary of the Company is a Joint Venture with Marubeni Corporation and Marubeni Hong Kong and South China Limited of Japan. The Revenue from operations of the company has increased to

19,112.99 lakhs from15,663.72 lakhs in the last year. The Net Profit of the Company after comprehensive income worked out to826.11 lakhs as against738.97 lakhs in the previous year registering an increase of 11.79% -

VTL Investments Limited (VTL): This 100% subsidiary of your Company is engaged in the business of investment. The earnings of the company mainly comes from dividend/interest earned on its investments and profits made on sale of investments. During the year, the Company has earned a net profit of

975.12 lakhs as compared to357.01 lakhs in the previous year. -

Vardhman Acrylics Limited (VAL): This subsidiary of the Company is engaged in the business of manufacturing of Acrylic Fibre. Presently, the Company holds 70.74% shares in this subsidiary. During the Financial Year 2016-17, VAL recorded Revenue from operations of

36,842.96 lakhs against44,759.18 lakhs in the previous year. The net profit of the company after comprehensive income worked out to4,099.14 lakhs as compared to4,080.18 lakhs in the previous year -

Vardhman Nisshinbo Garments Company Limited (VNGL): This subsidiary of the Company is a Joint Venture partnership of 51:49 with Nisshinbo Textiles Inc., Japan for manufacturing men’s shirts. During the year, the Revenue from Operations of the company was

5,828.84 lakhs as compared to5,799.22 lakhs in the previous year. The company incurred a Net Loss of53.88 lakhs as against a net profit of153.36 lakhs in the previous year. -

Vardhman Yarns and Threads Limited (VYTL): Vardhman Yarns and Threads Limited, Joint Venture with American & Efird Global, LLC (A&E), is an Associate Company of the Company. It is engaged in the business of Threads Manufacturing and Distribution. During the year, the Company has sold its 40% stake in VYTL to A&E and is now holding 11% stake in VYTL. A&E is the second largest player in Threads Manufacturing and Distribution across the world. During the year under review, the Revenue from Operations were

77,857.87 lakhs as against72,863.26 lakhs in the previous year registering an increase of 6.85%. The Net Profit for the year after comprehensive income worked out to9,909.48 lakhs as compared to8,991.66 lakhs during last year registering an increase of 10.21%. -

Vardhman Special Steels Limited: Vardhman Special Steels Limited (VSSL) is an Associate Company of the Company. The Company holds 31.39% shares of VSSL. During the year, the Revenue from Operations of the Company was

75,312.90 lakhs as compared to72,551.41 lakhs in the previous year. The Net Profit for the year after comprehensive income worked out to1,891.01 lakhs as compared to405.12 lakhs in the previous year. 43 DIRECTORS’ REPORT ANNUAL REPORT 2016-17 -

Vardhman Spinning & General Mills Limited: Vardhman Spinning & General Mills Limited (VSGM) is an Associate Company of the Company. The Company holds 50% shares of VSGM. It is a trading Company dealing in the business of Cotton and Fibre. During the year, the Company has not traded any goods. So, the Revenue from Operations is Nil for the Financial Year 2016-17. The Company incurred a Net Loss of

6,851 as against a net loss of27, 292 in the previous Year.

Valuations :

CMP = 1300

M.Cap = 7480 Cr

Enterprise Value = 9610 Cr

Debt to Equity ratio = 0.52

PEG Ratio = 0.29

PB x PE = 19.15

CROIC = 20 %

RoE = 18%

EPS growth last 5 yrs at CAGR of 24%

Sales growth last 5 yrs at CAGR of 4%

I have used Ben Graham’s formula to arrive at the intrinsic value.

The original formula from Security Analysis is :

V = EPS x (8.5 + 2g)

where V is the intrinsic value, EPS is the trailing 12 month EPS, 8.5 is the PE ratio of a stock with 0% growth and g being the growth rate for the next 7-10 years.

V = 109.1 x (8.5 + 2x5)

V = 2018

Management Quality :

Mr. S.P Oswal is the MD. I have googled with the names of Directors and company for any frauds or SEBI notices. No such cases are reflected.

Risk Analysis :

- 35% of the total sales of the company is exports. Hence company is exposed to currency risks.

- Raw material cost is about 50% of the sales. Hence any increase in cotton prices will put pressure on the margins. This margin risk is also evident from that last 4 quater results which show OPM reduced to 12% in Sep 2017 from 21 % in Dec 2016.

The cotton prices are said to go up in this year.

Cotton prices seen holding firm in 2018 on slow arrivals - The Hindu BusinessLine

https://www.icac.org/Press-Release/2018-(1)/PR-1-2018-Global-Consumption-Increasing - Textile industries are capital intensive by nature and hence bottomline may squeezed due to fixed capital costs and rising cotton prices.

Disclosure : Not Invested. Tracking. Intend to invest soon.