the company has not declared results for June quarter. I emailed them a couple of times, but got no reply. What could be the reason I wonder?

SME stocks declare only half yearly results. Its an Arti group co the leaders in chemical sector.Have patience & invested in it.

2 Likes

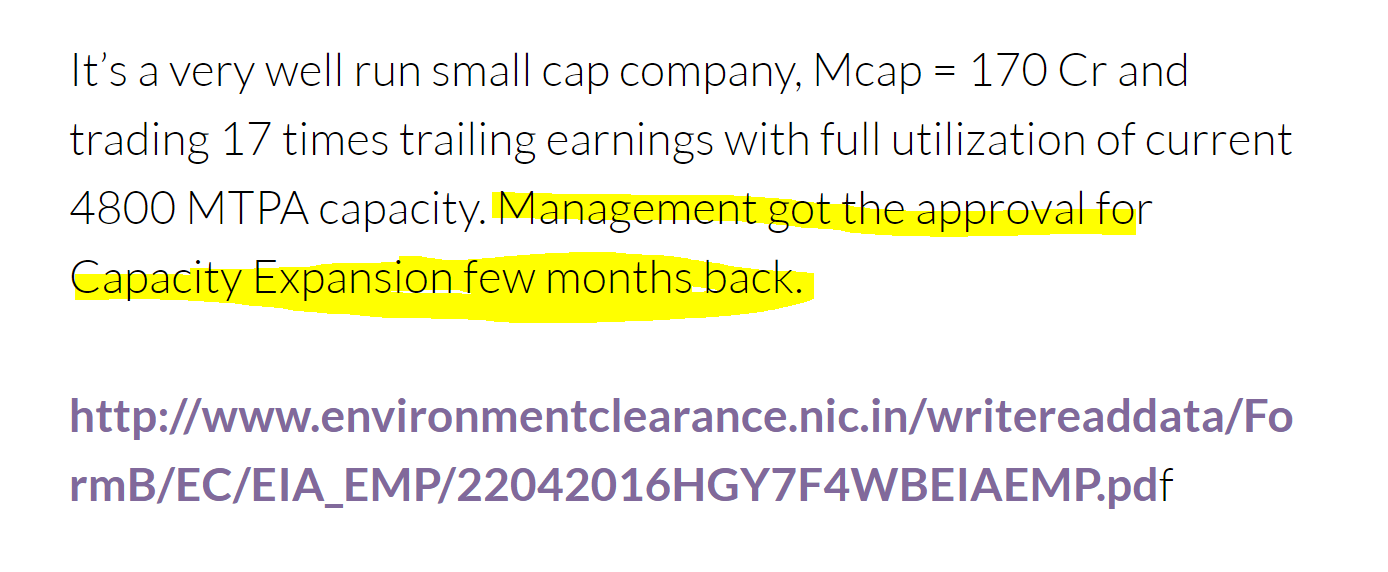

Any idea on how much was the capacity expansion done this year and if govt approval for same is received ?

If i remember correctly plan was to expand 5 fold in various products (correct me if i am wrong) . Lets see in this half yearly numbers how much is done. I hope management share the details too.

they were planning to increase capacity from 400 MT to 1800 MT (4.5x) in 3 years. I know that they have increased capacity and were waiting for govt approval. But I am not sure by how much was the capacity increased and if they are yet to receive the govt approval.

Any thought about how the merger with Abhilasha Tex Chem playing out ?

In annual report they mentioned nothing about it and their website also doesn’t show Abhilasha products in the catalog.

I guess it already happened but numbers are not reflecting that, Do you expect its numbers to show up in recent results.

Taken out the link … as personal links not allowed.

4 Likes

Hi Dhruva,

Nice write up.

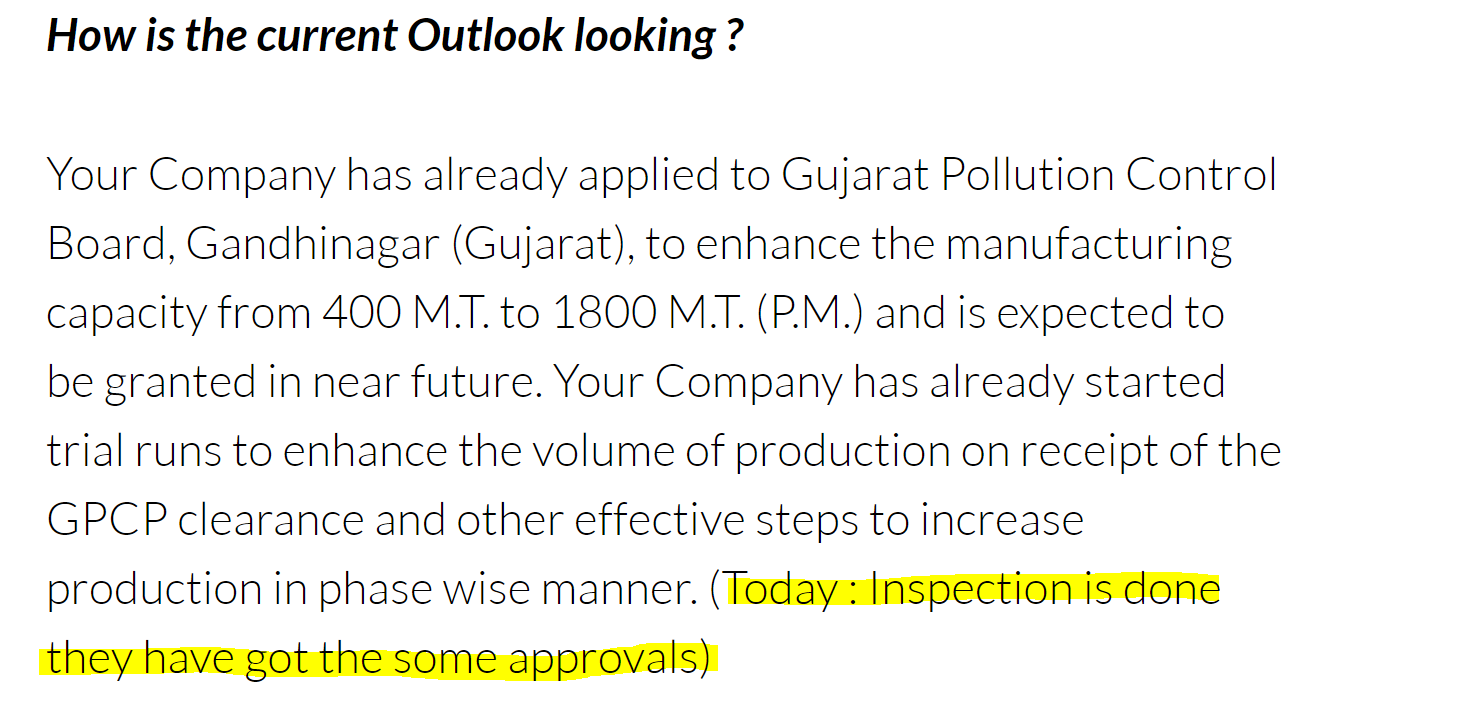

How to understand these two different statement.

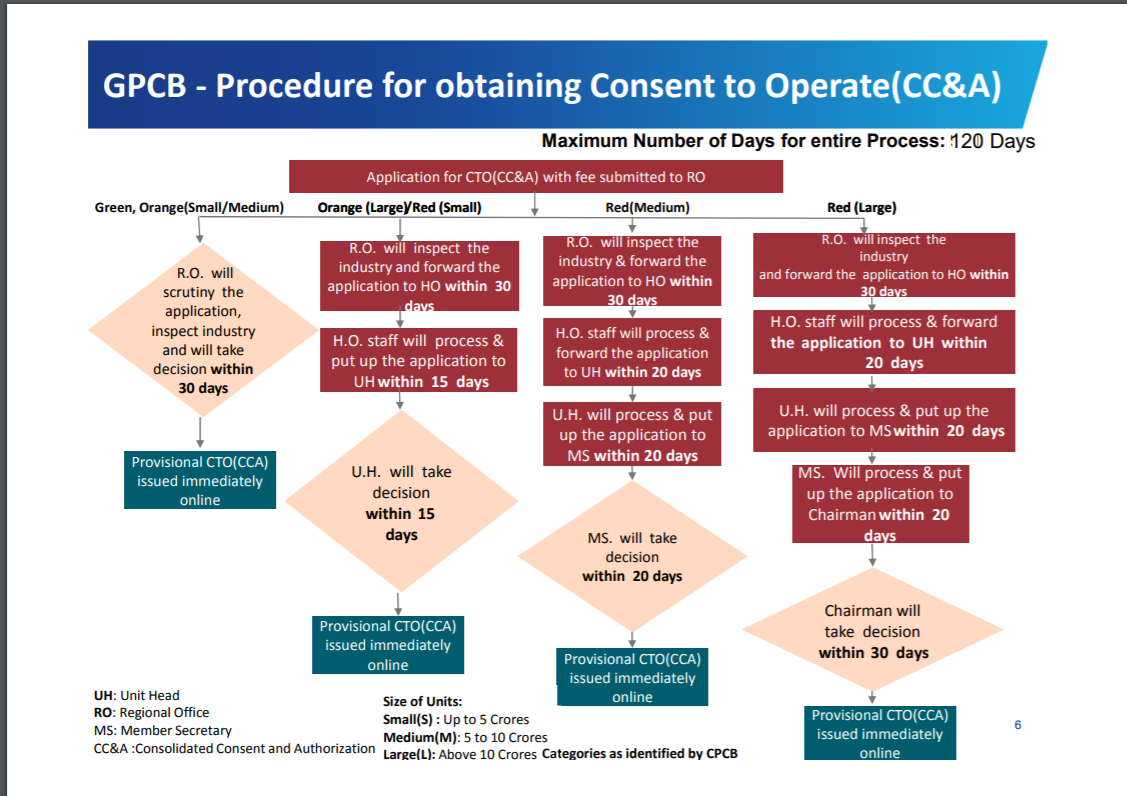

My understanding after talking to the management is that they have some permission with respect to installation of P& M and to carry out trial production only. Actual production can commence on getting GPCB permission which is pending. Increase in turnover expected due to sale of trial run production material.

Thanks

Disc: Invested

3 Likes

Ohh alright ! thanks for the information.

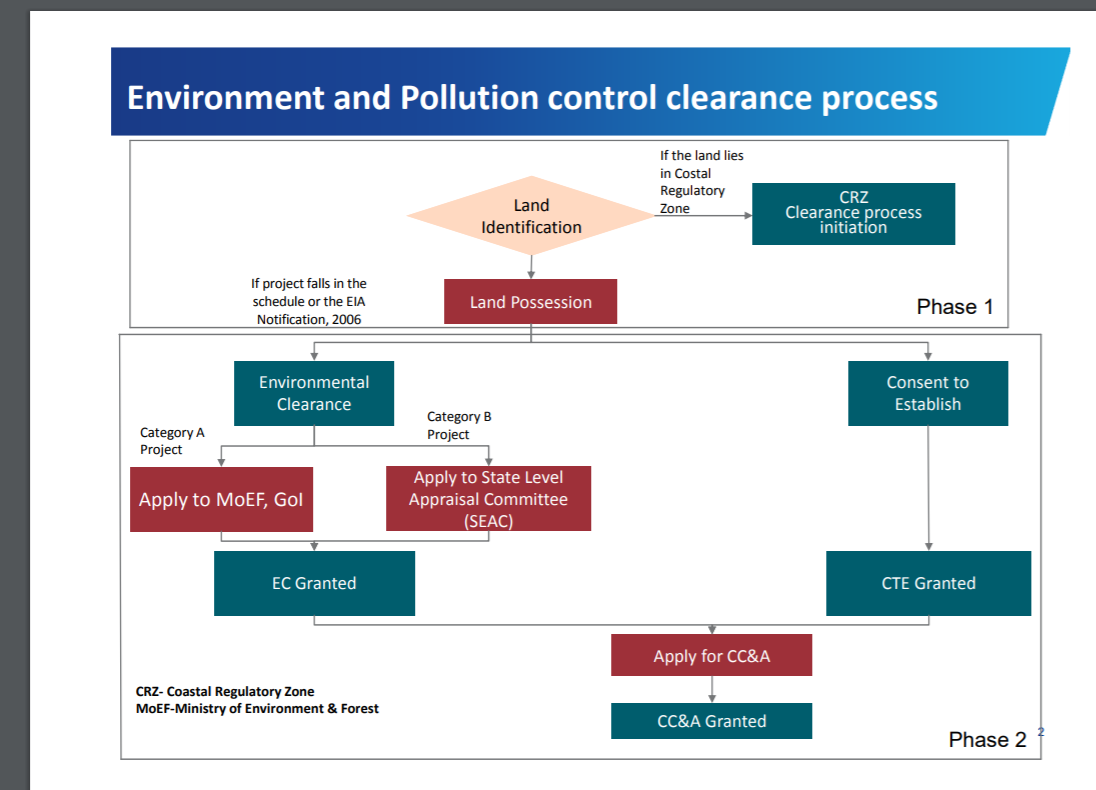

I always have headache understanding these documents (the link in above pic), I was confused between inspection is done or approval is also there.

My interpretation seems completly wrong, I’ll correct it.

Nice write up Dhruva. I liked your analysis elsewhere in this forum too.

While everything looks good, why do you think Mr.Market has not been kind to this stock since some time in Jul? Why has it fallen off from 600+ to around 500 now? Anything Market knows that we dont know?

2 Likes

Price action in short term can only be judged by flow … If you look at todays volume out of 0.36 Cr some two people decided to exchange 600 /- shares at -4% that doesn’t really mean anything to me.

Thats the only problem with stock market if all HDFC bank shareholders decide to hold (makes sense to hold that kind of stock) but one idiot decides to sell just one share at -20% the whole market cap of HDFC bank will collapse to -20% for that moment.

So, If you see the decline has happened at very thin volume, I don’t think if somebody knows something will have this much patience to sell drop by drop everyday so that no one notice.

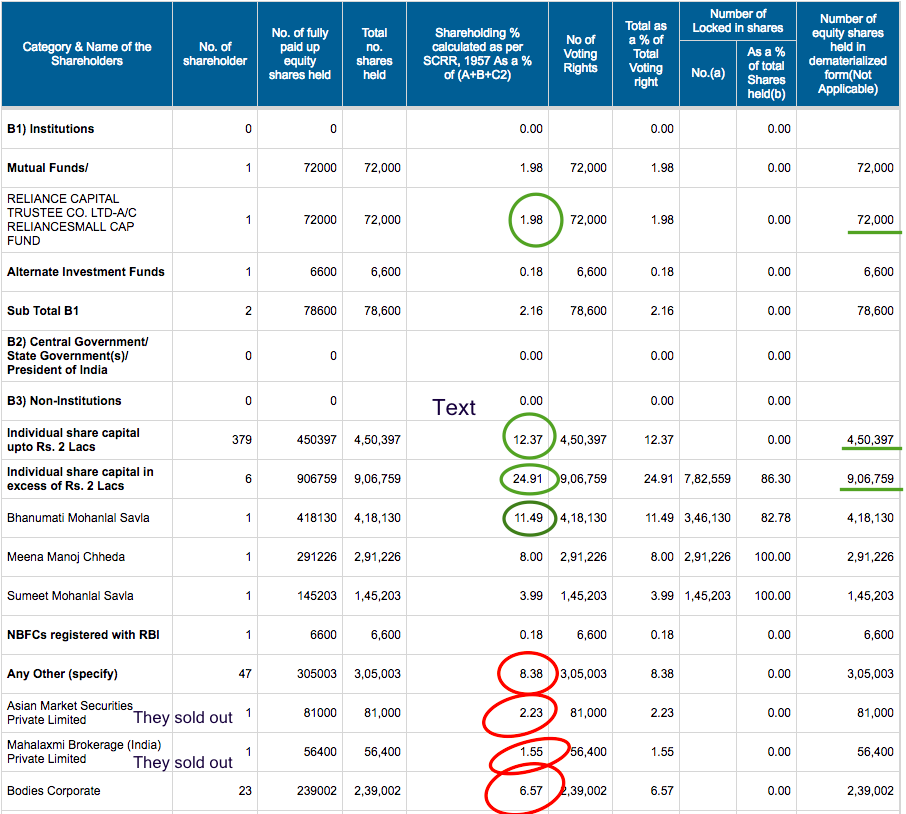

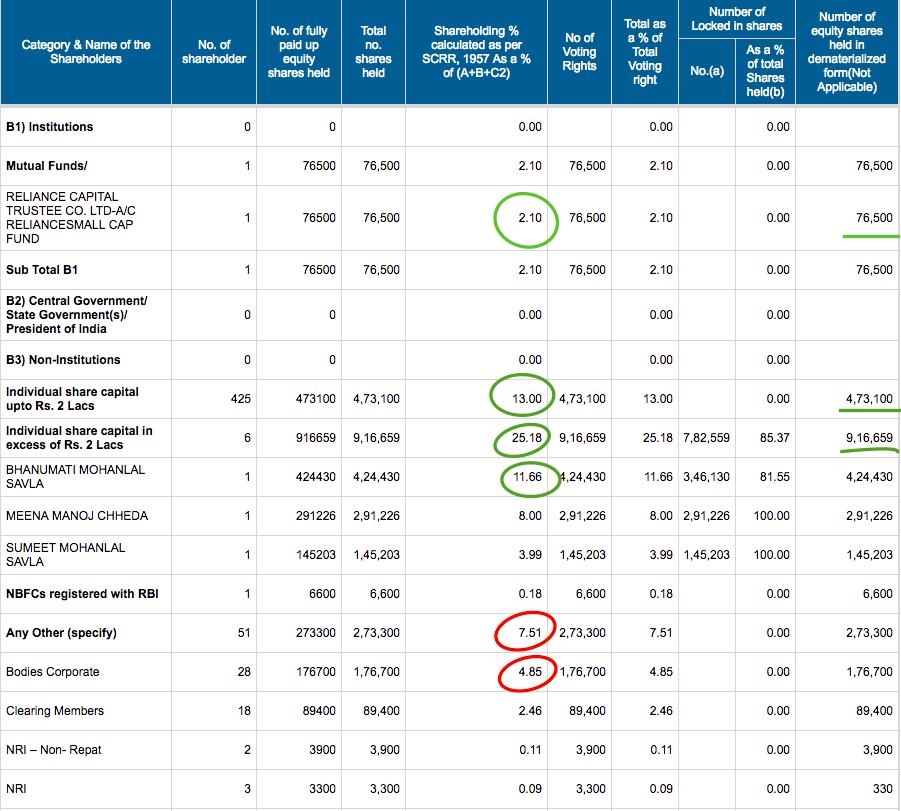

Anyways since you asked it that way i looked at the shareholding pattern -

It seems since March 2017 to Sep 2017

Reliance has increased its holding from 1.9 to 2.10 % They bought net net 4.5K shares.

Individuals up to 2lacs have increased their shareholding they bought net net 23K shares.

Individual holding more than 2 lacs have bought net net 16 K shares.

On the other hand below two sold out …

Mahalaxmi Brokerage Ltd

Asian Market Securities Ltd

and many other trimmed …

If these guys know something that others who bought don’t know then please TAG SEBI here .

March 2017

Sept 2017

1 Like

Some additional points:

-

Gujarat authorities gave clearance in early 2017. Refer http://seiaa.gujarat.gov.in/5%2013012017.pdf and http://seiaa.gujarat.gov.in/Minutes_104th_SEIAA_Meeting.pdf

-

Valiant is actually listed as a promoter entity in Aarti Industries.

3 Likes

And what is that? All this is publicly available info if you look hard enough.

4 Likes

So from the below flow chart its now clear that consent to establish( EC) was obtained in January 2017 and now the consent to operate( CC&A) is awaited:

Its a matter of time now for commercial production to start

7 Likes

somebody ask me these questions, I would love to know your thoughts on it.

- Source of funds for CAPEX – to understand the future of Balance Sheet

- Who will be the customer of this new 5x capacity? What is the Total Addressable Market?

- Why is the competitive intensity less in chlorophenols? Why is their process not easily replicable?

Those who are in touch with management, Please get their answers too.

1 Like

Once all clearances are obtained from GPCB,Valiant is going to add capacity at the rate of 2400 tonnes per year. So the expansion is going to be staggered. This is being done so that the market can take the extra production as the market for it expands and newer markets are developed.

For every 2400 tonnes of capacity expansion the capex envisaged is in the range of Rs.2.5-3 crores only and will be funded by internal accruals as per the management. Land they already hold so no capex would be required for land. Time required for addition of 2400 tonnes is approx 7 to 8 months.

4 Likes

Yes Dhruva. I had similar questions in my mind.

- What is the entry barrier for any other to enter and start making the same stuff and sell them?

- Who are their current competitors? What is this company’s MOAT which enables them to beat others?

- How does the order book look like? While utilization has indeed been maxed out, do they have customers lined up to buy the extra stuff they plan to produce?

Could not find answers to these in their AR.

I also I came across an interesting article about Amalgamation of Abhilasha Tex-Chem with Valiant.

There are a ton of useful info about this marriage here.

Yes … Swap ratio seems to be fair.

If you see FY17 profits can be assumed for ATCL around 5 Cr (I guess this could be bit on the higher side considering past growth) , then EPS comes around 82.

VOL EPS = 27.

So, Each ATCL shareholder should get 82/27 amount of VOL shares which comes around 3.

they kept the swap ratio of 3.65

//

365 Equity Shares of VOL of Rs10 each will be issued for every 100 Equity Shares of ATCL having Face value of Rs100 each.

Not that bad i have seen worse

https://dhruvapandey.wordpress.com/2017/02/15/arfin-india-how-to-cheat-minority-shareholders/

I exited on this crap and since then stock has doubled.

Hi,

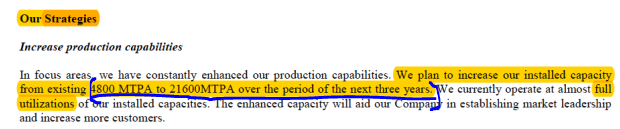

In one communication, mgmt communicated for 5x increase in capacity in 3 years

In other communication - capacity in next 2 years is only increasing by 2x (so 2019-20 capacity increase should be 11600 tonnes)

Also @manojag mentions capacity to be increased in buckets of 2400 tonnes per year. At this rate company would 7 years (not 3 years) to increase the capacity at 21600 tonnes

Can somebody clarify on this.

1 Like