Each of the 50 stores of V2 retail is doing 12 crores in annual sales, and being valued at 30 crore per store. Given most of these stores are in small towns, I find these numbers too large to make sense!

1 Like

I’m a long-term investor in V2 Retail. On a work visit to Delhi about 10 days back, I dropped into their store near the international airport. Was very impressed by the overall look of the shop and their systems. Piped music playing Hindi hits, with intermittent announcements about their ongoing promotions. Bought a T-shirt and did a few enquiries from the counter clerk. He told me they are currently doing sales worth 4 to 5 lacs every day. On the weekend the sales climb up to 6 to 7 lacs a day. The number goes up by at least 50% during the festival months. Considering this was one of their larger outlets, I can imagine 12 crores per annum per store could be the right figure or pretty close to accurate.

7 Likes

V2 Retails opens 2 more stores in Jharkhand and Odisha.

http://equitybulls.com/admin/news2006/news_det.asp?id=228011

V2 Retail Ltd opens Retail Store at Hyderabad, Telangana

http://equitybulls.com/admin/news2006/news_det.asp?id=230853

60th store opened today.So, another 40 stores remaining as per management target for this year

1 Like

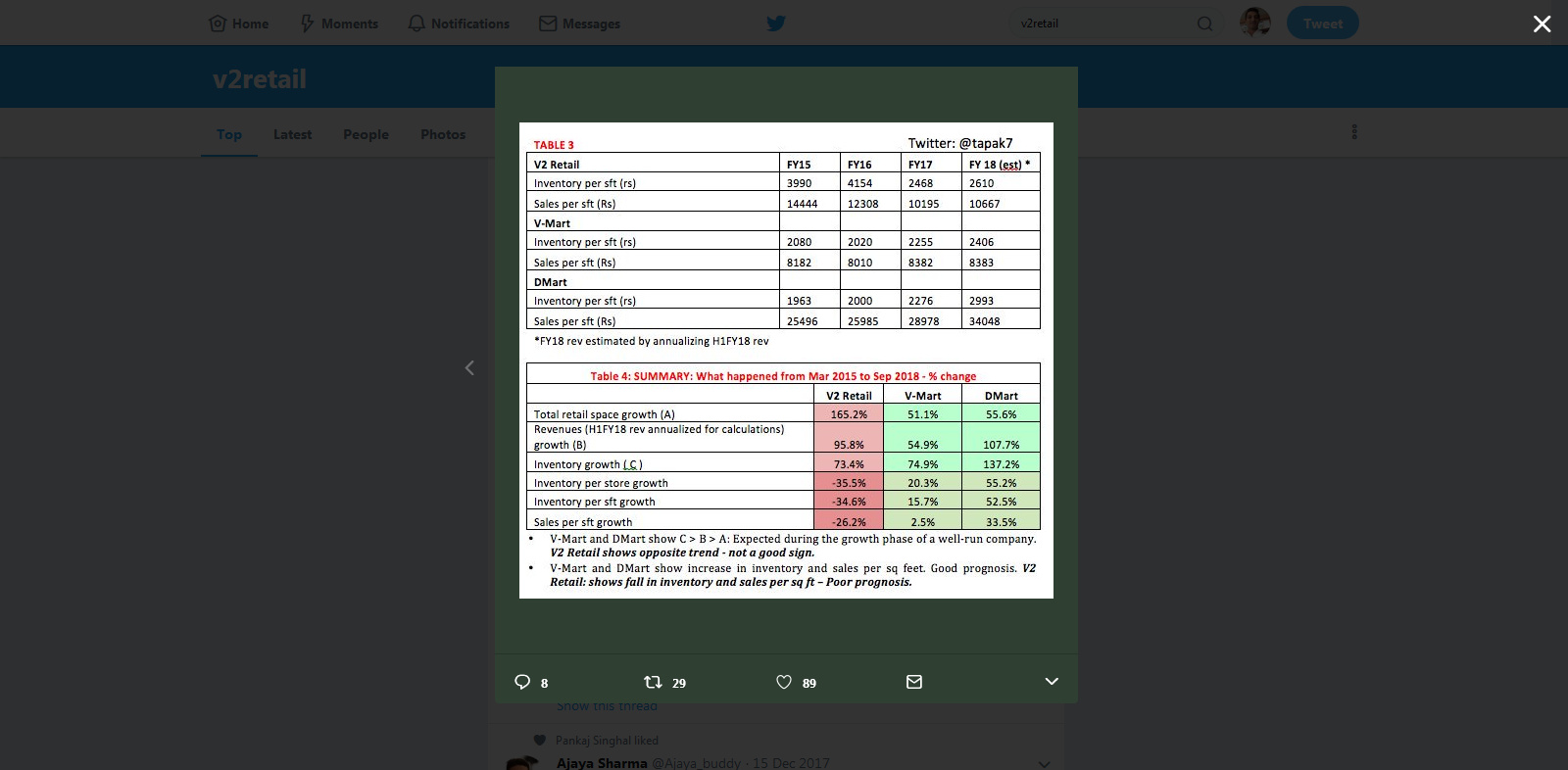

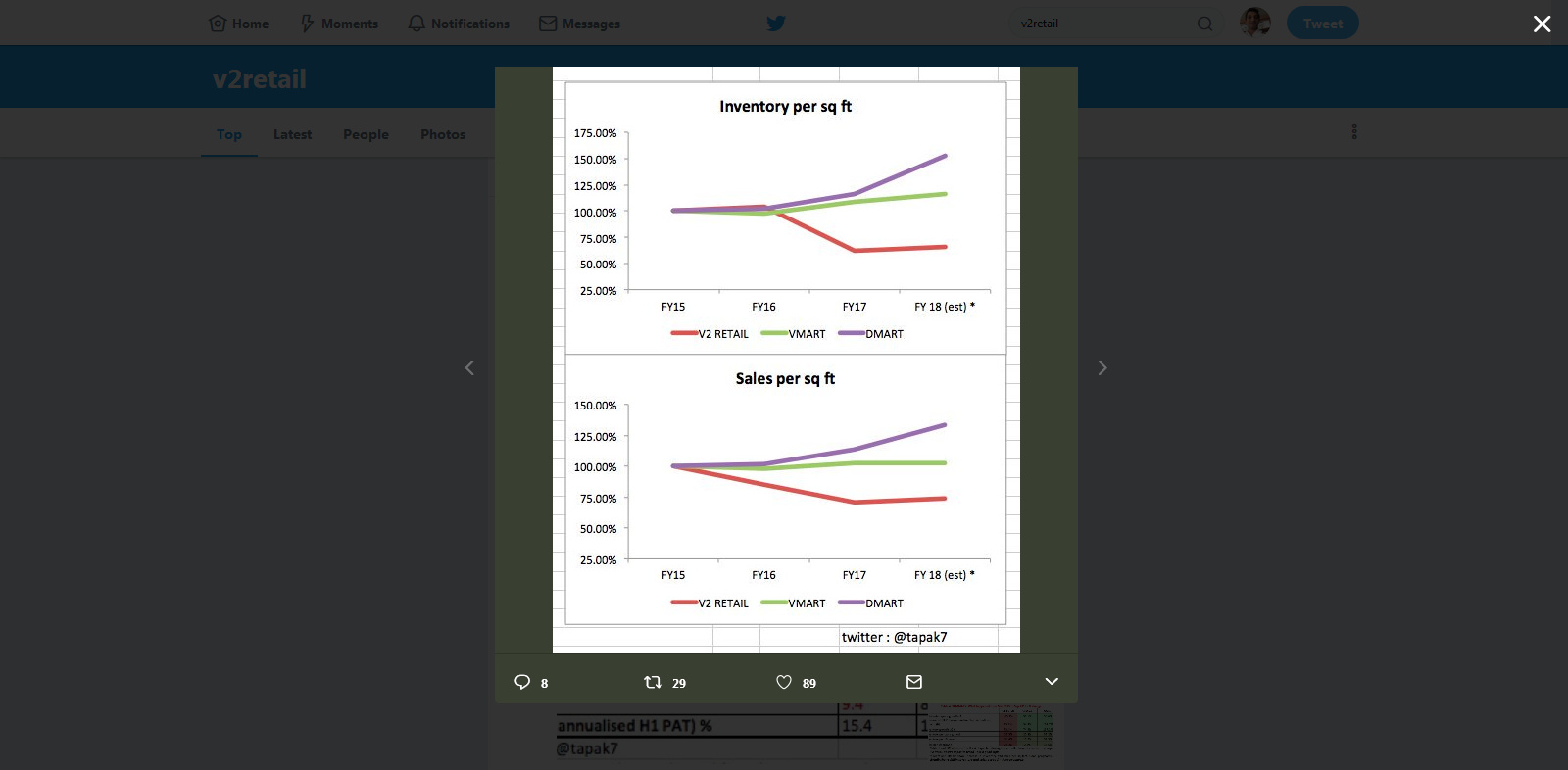

Found these slides by a well followed person on twitter. Personally i agree with the analysis given how Q3 and Q4 results have panned out. Would want to know other people’s opinion about the same. Not that things cant get better from here as it happens with many small cap companies. ( dis: Buying price is 35 but presently selling out slowly )

2 Likes

I am failing to understand why there is so much demand of vmart whereas v2 retail is hovering on same price for last 6 months. Both have same customer targets. More or less their ebitda margins are same. Anyone can shade lights on the differences between them?

1 Like

1 Like

V2 Retail posted good results in Q1, but even then the stock is in correction mode.

http://equitybulls.com/admin/news2006/news_det.asp?id=233507

Can anybody throw some light into this price behaviour of V2 Retail?

maybe growth is 29% and PE is 40

but that is also a guess

I have invested large chunk of my portfolio in v2 retail thinking it is a small cap and in consumption space. But since January nothing is happening in stock price. Results are good so I am not thinking to move money from v2 to somewhere else.

Is there any issue which we might not be knowing.

hold on as results are good, so eventually it will pick-up

Disc: Planning to invest

the reason in my opinion is return on capital and return of equity which r much superior for vmart. But these cud also b coz v2 is in aggressive expansion mode so the ratios will remain low till d new assets start contributing to the top and bottom line

Promoter to Promoter transfer

Akash Agarwal gifts all his 7.3% s=stake to his father Ram Chandra Agarwal.

Why - is there anything negative (like son moving out etc) that has triggered this transfer …anyone any ideas

V2 retail from Jan2018 gave around -41% return. I was unable to understand this much of a fall. They seem to have reasonable growth and margins. I met an advisory company a few weeks back, they told me v2 retail same store sales growth is negative which is key metrics in evaluation and other thing is they are in the UP-Bihar region where purchasing power is very less.

I was obviously worried with its stock performance so attended its recent Q2FY2019 conference call and found couple of noticeable points.

- Same Store Sales growth is going to be negative or at most 0%. Whole growth will come from new stores addition.

- Competition has increased. Earlier there were only 2 such stores in the city but now 4-5 stores have opened and this is resulting in no or negative growth in SSG.

- They are spending lot of money in building company for long run and beat the competition by installing SAP Hena system to predict demand, inventory mgmt; own private label designs, increased Head office team. All of these changes will play in FY2020.

I am not sure that these changes can beat the competition. Competition will stay and drive the profitability down. I have also seen VMART mgmt showing increased sign of competition.

Right now there is serious loss but not able to make mind to exit from the counter. Let me know What is your opinion on this stock.

3 Likes

I had a large position in V2. Have exited.

Here are my reasons,

-

Increasing competitive intensity. A number of players seem to have entered this segment. V2 continue to hold the view that mobile/online retail has not been affected by them, but it is hard to think it will not affect them over the next couple of years.

-

No clear plan from the management to address competitive pressures. Last quarterly call they talked about B2B offerings, inhouse brands and process improvements. This quarter’s call was about automation, process improvements and a passing reference to online portal. It seems they are still trying to find their way through the competitive landscape and tweaking their business model.

-

Poor execution (reduced the guidance of opening 100 stores to 90 by EoY 2019). SSG has been negative or zero and the guidance is that SSG will be around these levels going forward. Their expansion is South India is taking much longer to materialize. Store closures seem to be happening too. They have yet to explore Tier-4 towns while their competitors seem to be already doing that. This will hamper their capability to deliver the stated 40% Y-o-Y growth, assuming they do it just by opening stores and don’t take on debt.

-

Increasing cost pressures. In the call you attended they also talked about refurbishing their portal and getting their omnichannel strategy going. I see this as a significant pressure on costs as they will have to spend large amounts on online marketing to get any traction from their portal. Online retail is a tempting but very different business and one must tread very carefully. Additionally, they then start competing with the bigger guns in the online retail space.

-

The management seems to be cagey and coy about explaining things and shifts statements without explanations. The way the exceptional item relating to settlements came out of nowhere this quarter could have been better managed. I went to their annual meeting, which was poorly managed (well, more stage managed than managed).

-

The SAP Hana rollouts and the automation of 40+ processes etc. is a complex exercise which will not bear results immediately, if at all it does. They haven’t articulated how they see this rollout affecting them, except improving “efficiencies” etc.

-

Their sales are going to be flat-ish this quarter, which is supposed to be the strongest for retail, fourth quarter is usually not a great quarter either, so for the next 6 months there is unlikely to be any major improvements in top or bottomline, except from the store count additions.

-

End of cycle risks. As US markets correct, international volatility persists on trade negotiations and domestic volatility amps up due to elections, further corrections are like from its current high PE>30.

I believe they haven’t hit a growth bump but a management capability bump, which will take a while for them to sort out as they seek better talent to join them and sort out they processes and structures and business model. They have made some moves in that direction with their product design teams, process automation etc. but more needs to be done.

These are my reasons. I would appreciate feedback on this (supporting or challenging this line of thinking). Also, these are are just opinions.

5 Likes