Bad results again by UPL. Missed the estimates by a huge shot. Debt’s interest cost is very high tbh

2 Likes

What is the risk of default for UPL? With such high debt , I am currently comfortable to buy it at book value only.

Not invested: keeping a watch.

I think we can wait. As per management presentation expecting recovery from Q2FY25

1 Like

improvement in the chemical cycle and interest rates cut globally may lead to some positive results

The decline in revenue was majorly attributed to Destocking and lower demand in the European Union and the margins have been impacted due to high-cost inventory liquidation and higher rebates to support channel partners. The company mentioned that the business will be back to normal only after Q2FY25.

We have been witnessing a bearish price trend for the company and the same is expected to continue for the time being.

The company has, at last, realized that its main priority is to reduce debt and it will raise rights issue of up to $500 Mn to repay debt and explore other opportunities to repay debt.

4 Likes

This is what I am fearing for. Market wil beat such high debt ridden stock. Will only accumulate near book value. I rest my case here.Open for discussion.

3 Likes

Noob question: With the recent rating downgrade will the interest cost rise for existing debt as well? Or will the higher interest cost (based on ratings) be applicable for fresh loans?

3 Likes

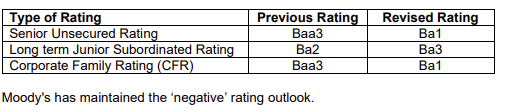

Fitch Downgrades UPL Corp to ‘BB+’; Outlook Negative

UPL’s weak performance mainly reflects sustained pressure from overcapacity in China.

UPL expects channel destocking, which has affected demand, to subside by 1HFY25. However, the outlook for capacity in China is more uncertain. We assume UPL’s product prices and margins to rise meaningfully from 4QFY24 on supply rationalisation in China in response to weak profitability. However, there is risk that the glut will persist for several years and constrain UPL’s EBITDA margin improvement.

1 Like

UPL out of the NIFTY50.

2 Likes

p/bv is al time low & EV/EBIDTA-11 Low to peers. Capex , share holding only 16% retail holding; OPM should mean to reversion. Inventory normalized, Q4 should be better. Margin of safety looks good. Price retest trendline july 2013 to mar 2024 on monthly line chart.

Is it a value stock or a value trap though?

The main problem that has emerged recently is their high debt levels (incl. high working capital reqs.) which are significantly worsened in a soft worldwide agrochems market.

China is a big landmine, with excess capacity at home, they are dumping.

Demand may revive, but what about china?

Exclusion from index is also a bad thing.

Overall, it does not look like a good thing to buy or hold right now. The long term growth will also be slower this decade compared to last (perhaps high single digit). There is no visibility on when rate cuts will begin worldwide also.

IMHO this is not yet peak pessimism and more pain can be expected.

DISCLOSURE - just a lay person, i am also known to be an idiot, so …

6 Likes

UPL plans to launch an IPO for its seeds business named Advanta Enterprises in early FY25 as per CNBC TV18 report.

2 Likes