Hi,

I have made some refinements and updates to the below note. Please use this link to refer to the updated version of this note: Yellowstone Equity | Best Ideas Basket | Multibaggers

Thank you,

Ankit

Note on Uniply Industries

Disclaimer: This note is just for discussion purposes and has no other intention.

1) Suspicious and High Quantum of Related Party Transactions:

There are more questions than answers regarding the related party transactions at Uniply Industries.

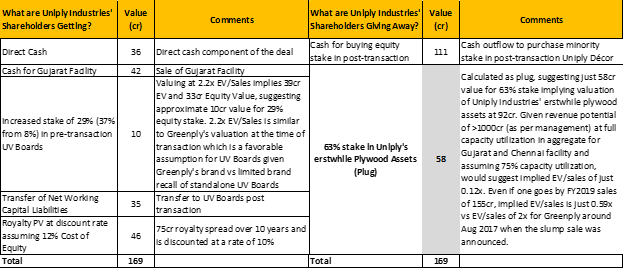

Slump Sale of Plywood Business at a Discounted Valuation to Related Party: If one looks at the economic value of this transaction (not the camouflaged 300cr economic value quoted by the management), one notices that Uniply Industries’ shareholders went from owning 100% of Plywood business to ~37%, while receiving marginal net economic value, suggesting that the sale happened at a significant discounted valuation to the detriment of the minority shareholders. Below table shows the economic value obtained for the effective 63% stake sale in the plywood business. As per below, the transaction happened at EV/Sales of just 0.12x, if one takes the full revenue potential of the Plywood business (>1000cr revenue potential, as per management, implying 750cr revenue assuming 75% capacity utilization) and at just 0.59x per FY19 sales. This compares to 2x EV/FY19 Sales valuation for Greenply and CenturyPly around Aug 2017 when this slump sale transaction was announced. Looked another way, why is the 37% stake in the post-transaction UV Board business valued at 111cr vs 63% of Uniply Industries’ erstwhile plywood business valued at just 58cr, when the post-transaction UV Board business (i.e. Uniply Décor) is going to comprise primarily of Uniply Industries’ erstwhile plywood business?

Management claims that they would be able to get rid of debt completely post this transaction. However, as the above suggests, net present value of economic value from this transaction would be just 58cr. This when looked from a cash flow perspective, i.e. adjusted for royalty payments (present value of 46cr) that are staggered over 10 years, non-cash nature of increased stake in pre-transaction UV Boards (10cr) and including the 3.75cr royalty payment made for 2H FY18, current cash flow from the transaction would be just marginally positive (58 – 46 – 10 + 3.75 = 5.75cr) at 5.75cr. This is surprising as the management claims that after this transaction, Uniply Industries will become completely debt-free. Only debt reduction with this transaction was through reduction in net working capital liabilities. Rest of the debt remains intact as indicated by end of FY18 balance sheet borrowings of >300cr. Furthermore, why is there such a high inter-corporate loan of 97cr from Uniply Decor (previously UV Boards) to Uniply Industries? This is close to 100% of revenues for Uniply Décor at the time.

20cr related party transaction to S. Viswanathan Printers & Publications Private Limited during FY 2017 (classified as related party w.e.f. Mar 20, 2017): One of the directors on S. Viswanathan Printers’ board is Nivedita Lakshmi Ratan (probably wife or daughter of Uniply Industries’ director Lakshmi Ratan). Why would Uniply Industries, a plywood company, do such a high value transaction with a book printing agency? Printing and Stationery expenses as per FY2017 annual report were just 37 lakhs. Even if this was a legit and reasonable related party transaction, why has there been no disclosure around the nature of this transaction as shown in the below excerpt from the FY17 annual report?

Except for this line item, all other related party transaction line items have some description for the nature of the transaction. This is not the only case where related party transaction has been conducted with relatives of directors. In FY 2016, Keshav’s wife’s entity, RMKV Fabrics, has had related party transaction with Uniply Industries in the form of inter-corporate loan deposits of about 4cr. There is also a small related party transaction with CFO’s wife in the form of legal fees.

2) Suspicious Cash Flow Trail at Uniply Industries

A closer look at the cash flow movements of Uniply Industries reveal that, since the new management took over1, only a part of the investor capital raised has gone into real assets. Rest of it has been diverted to either promoter’s other business entities, suggesting potential conflicts of interest, or have been consumed for deteriorating working capital requirements, suggesting weak quality of sales.

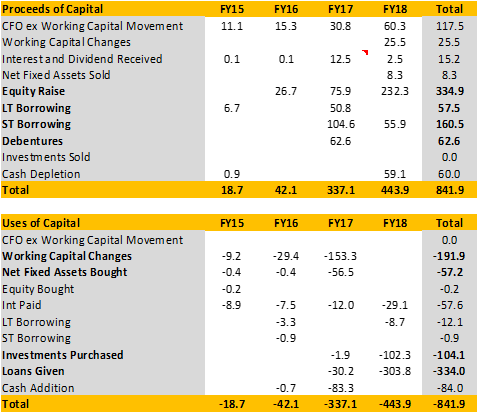

Over the past four years through FY18, management has raised 615cr, 335cr from issuance of equity/warrants and the rest 280cr (split as 57.5cr: long-term + 160.5cr: short-term + 62.6cr: debentures) from debt. This contrasts with management’s tall claims and promises of rationalization of balance sheet and reduction in debt.

Below is a summary of Uniply Industries’ proceeds and use of capital over the past four years.

As the Uses of Capital table above reveals, the two big-ticket items where the capital has been used are “Loans Given” and “Working Capital”. Let us take a closer look at each of them.

a) Loans Given: Bulk of the 334cr loans given have been funneled to other promoter entities like Foundation Outsourcing India Pvt Ltd “FOIPL” (name changed to KKN Holdings – holding company for Keshav’s investments) and Foundation Outsourcing Pvt Ltd (seems to be an offshore entity as no MCA records available for it) in the name of capital advances. Going by Foundation Outsourcing company’s website, it is an investment holding company with ownership in Uniply Industries (and subsidiaries like Vector, Uniply Blaze), ArtMatrix Malaysia, ETA Techno Park SEZ and Forge Point. It appears that the capital advances made to FOIPL have gone into acquisition of 40% stake in Art Matrix, other investments like ETA Techno Park SEZ, etc. with the promoter entities gaining beneficial ownership in these companies at the expense of Uniply Industries’ shareholders.

ArtMatrix Malaysia Investment: As per FOIPL’s website, FOIPL owns 40% in ArtMatrix Malaysia. While the transaction date for this is not known, Uniply Industries came out with a public announcement in Jan 2018 revealing intention to buy 100% stake in ArtMatrix Malaysia and a related proposal to raise ~200cr via equity capital. Later in Feb 2018, when the actual capital raising proposal was announced by Uniply Industries, it was not just the ~200cr capital stated above but also included plans for raising additional capital of ~400cr, so all in the plan was for raising ~600cr of capital suggesting an equity dilution of ~60%, assuming all warrants are exercised within their stipulated tenure of 18 months. There was no specific mention of what this 400cr capital was going to be used for. While Uniply Industries went ahead and executed its capital raising of 600cr by Apr 2018, since then it has gone completely silent on its plans to acquire Art Matrix. It has been over one year now and there has been no communication on how the raised capital is being used. On the other hand, promoter entity FOIPL’s 40% stake in Art Matrix Malaysia raises suspicion around management’s intention, potential conflicts of interest and potential funding of the stake via the capital raised from Uniply Industries’ shareholders.

b) High Incremental Working Capital: Other big chunk of cash outflow for Uniply Industries has been the incremental working capital. Since end of FY14 to end of FY18, Uniply Industries have clocked incremental sales of 275cr (incremental revenue each year during FY15-18 relative to 160cr in FY14) requiring incremental working capital of 165cr, which implies 60% of sales i.e. approx. 215 days. This contrasts strongly with management’s claims of strong improvement in operational performance and working capital metrics since the new management took over the company. Given Vector serves marquee B2B clients who can be assumed to be paying well in time and deploys fast-paced technology-driven execution, one wonders why is the working capital requirement for Vector Projects so high? Is there any issue with the quality of sales?

All in all, of the 615cr capital raised, legit real investments have been only 270cr split as:

• Net investments of 49cr in fixed assets: Purchase of 57cr of fixed assets, offset partially by sale of 8cr of fixed assets

• 84cr investments (net of goodwill): 104cr cash outflow (refer to the “Uses of Cash” table) towards investments purchased. Of these investments, about 111cr represents 37% stake in Uniply Decor. Uniply Décor has goodwill of 81cr, which adjusted for 37% stake is 30cr. Deducting this 30cr from 104cr, gives us 84cr.

• Expected incremental working capital of 138cr: Incremental sales of 275cr would need working capital to the tune of 40% of sales (conservative assumption)

Were it not for the loans given and weak working capital management, these 270cr investments could have easily been funded by internal accruals of >100cr as indicated by cashflow from operations ex working capital (CFO ex WC) over FY15-18 (adjusted for other miscellaneous cash outflows) and some additional funding (<200cr) via debt/equity vs current capital raise of 615cr. Why did the company raise so much capital despite the management’s claim in its FY18 Annual report that “The Company does not expect to make any significant capex across the foreseeable future”? The 615cr capital raise through FY18 does not even include the pending 300cr of capital expected to flow from convertible warrants during FY19-20. Note about 200cr of warrants were already exercised in Oct 2018, so only 100cr worth of warrants now remain unexercised. Despite all this capital raise and a significant chunk of business coming from asset light construction business as we stand today, Vector’s revenues declining in FY19 (which means freeing up of some working capital), why does the company continue to carry >300cr debt as of end of FY19?

3) Tall Claims vs Actual Execution

De-growth in Plywood’s B2C Business: Uniply’s B2C business seems to have de-grown significantly from the time it was acquired. At the time of acquisition in 2015, Uniply TTM sales were about 170cr. As of end of FY19, excluding sales to Vector which is a B2B business, plywood business’ B2C revenues were <100cr, significantly lower than that in 2015. This is in line with my channel checks regarding Uniply’s on-ground presence. To get a sense of the distribution network of Uniply, I called >25 dealers across Chennai, Chandigarh and Ahmedabad. <10% of these dealers carried Uniply brand and some of them did not even recognize the brand. Of the few dealers that carried Uniply, they also carried other renowned brands such as Greenply, Centuryply, etc. Further conversations with these dealers revealed that Uniply has no particular competitive advantage over other brands. Many other branded plywood companies are also offering termite-proof, water-resistant properties along with 20+ year guarantees.

De-growth in Vector’s Business: Going by FY19 results, Vector’s interiors business revenues declined to <270cr in FY19 vs about 320cr in FY18. Were the FY18 sales skewed by a one-off contract from the Karnataka government? The deteriorating working capital as of FY18 highlighted earlier, possibly were already hinting the weak quality of sales of this business.

Weak Brand Advertisement: Actual advertisement expenditure has been nominal relative to the 4-5% of sales guidance provided by Keshav back in 2015. Advertisement expenses were <17 lakhs in FY18 (<0.2% of plywood sales), despite a staggeringly high royalty fee of 7.5cr charged to Uniply Décor (3.75cr of which was paid for 2HFY18). In FY17, advertisement expenses were as low as <4 lakhs.

Keshav’s Claims Full Utilization of Chennai Facility: In a May 13, 2016 Interview to ET Now, Keshav claimed they are running at full capacity in their Chennai facility. This contradicts Keshav’s claims at the inception where capacity for Chennai facility was quoted to be 425cr (170cr revenues were already being clocked before Keshav’s acquisition and Keshav quoted capacity utilization to be 40% then) vs FY16 revenues of 145cr.

Share Pledging: Despite Keshav’s claims of completely doing away with share pledging, share pledging activity has continued unabated with pledged shares at times as high as >50% of the total promoter holding. Furthermore, some of the entities to whom shares were pledged like Kolkata-based L.K. Securities are not as well known and raise suspicion around the legitimacy and intention of such transactions.

Delayed Amalgamation of Vector: Why has the amalgamation of Vector Projects India with Uniply Industries delayed? Even if delayed, why not have the same auditor for both Uniply Industries and Vector Projects, given Vector Projects contribute a large part of revenue and assets at the consolidated level?