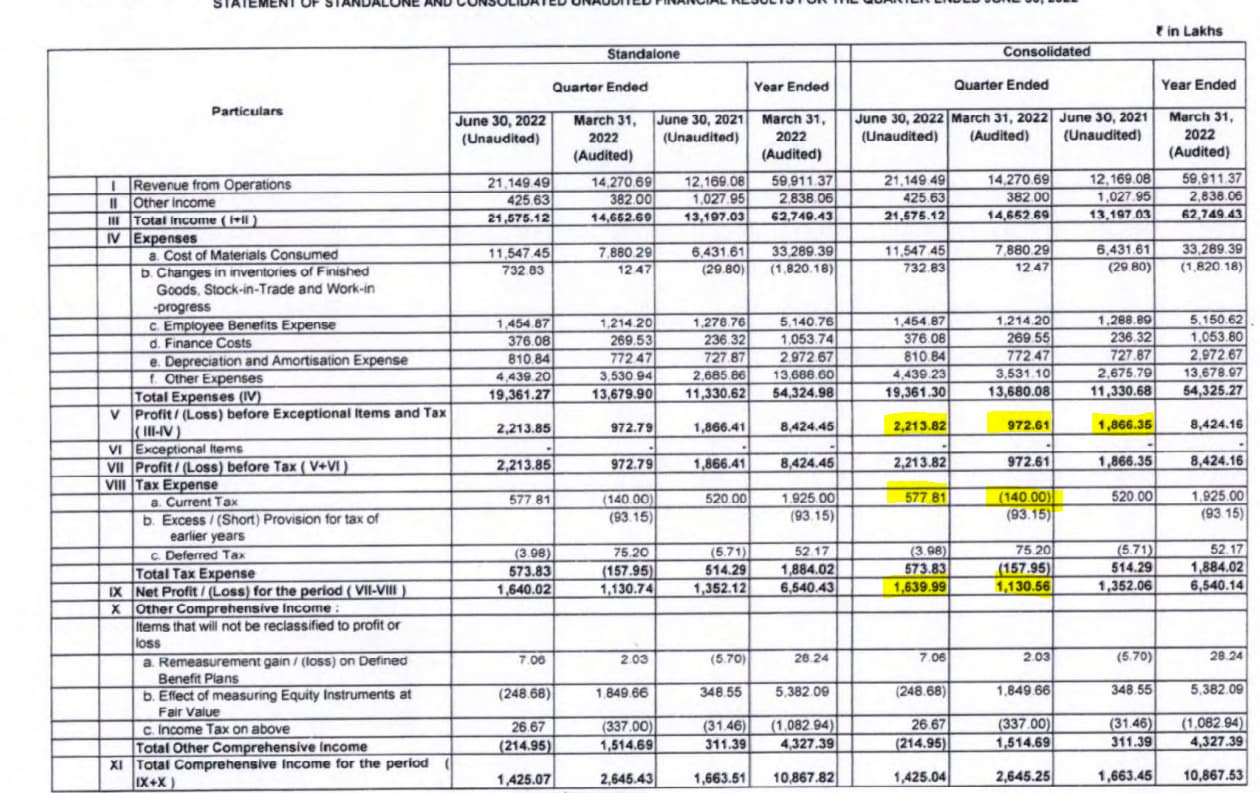

Quarterly results

Sales almost back to pre-pandemic levels while margin contraction happened . Let see if the margin comes back.

1 Like

Looks like a decent number from Transpeak. There is a sharp jump in revenue by 50% QOQ, but profitability has improved by approx 50% QOQ, suggesting that they have managed to pass on RM increases to end clients.

4 Likes

Transpek Industry Q3FY23 earnings call highlights.

-

We are a six decade old company and manufacture wide range of Acid and Alkyl chlorides. Globally we are well known, renowned for our proficiencies in sulphur and chlorine chemistry.

-

Current facility that we have, we have a manufacturing facility at Ekalbara, which is near Vadodara in Gujarat. The entire production capacity, which includes captive consumption of some products is estimated to be 66,000 metric tons. Just to clarify, merchant sales capacity is nearly 30,000 metric tons, out of which 15,600 is done at Ekalbara location and balance 14,400 metric ton per annum is through job work sites.

-

Growth has been primarily driven by international market as compared to the domestic business. Some of the issues such as supply side disruptions, raw material availability and price and higher freight cost have weighed on chemical industry as we all know. It has continued to hold back in general the growth momentum and we expect this to continue in the near term for chemical industry. Although freight charges and RM prices have eased out in the global market and that has helped further reduce the cost pressure in recent times, lot of uncertainty still prevail due to the current global situation.

-

Coming to new product and product developments, we are working on a couple of areas to diversify our clients, end user market and products. In nine months of financial year 2023, we have introduced five new products and anticipate adding a couple of more products that are in various phases of development. Once launched and once we reach a critical mass, these products will contribute meaningful business as well as reduce our reliance on one or two products on a significant basis. Together these 7 products have 150 cr sale potential. So some of the products we will be able to scale to the full extent, but some of the products that we have, or we are introducing or we have introduced also has much larger market. So right now of course we are working with one or two customers with whom we initiated this product but some of these products have larger markets and to capture that larger market, we will have to work on a combination of looking at our job work partners and see whether they can produce some of these products or these volumes.

-

We are having about 20 products at this point in time, about 14 products are regular products, 6 products are kind of semi-regular products where we produce based on the overall demand and of course we can do many other acid chlorides as per the demand of customers, acid and alkyl chloride, because we have already developed those products.

-

We are already working on building our business in geographies like South America, Eurasia and Japan and we have some positive indications from these regions.

-

we have been given permission but I also explained earlier that while 450 metric tons permission has been given, we can utilize about 200 to 250 metric ton per month, because otherwise we may exceed the effluent limit depending on the product.

-

We are indeed looking at other strategic initiatives to capture further growth including brownfield expansion and/or greenfield expansion. We are already on drawing board and discussing various options, possibilities and eventually, once we have a clear understanding of the way ahead, we will seek our Board’s approval and once Board approves, we will definitely and surely inform you at the appropriate moment on the initiatives that we plan to take.

-

We have highlighted that we are already replacing one old plant with a new plant with about 70% higher capacity and that would help in capturing higher demand for that product and this is also being designed in a manner which is going to be a multi-product plant. We have flexibility based on the demand scenario so far as this plant is concerned, we can produce different, different products. This will operationalize around anywhere between August to October of this year, this calendar year.

-

we can grow in acid chloride only up to 250 metric ton per month maximum. And this other Friedel-Crafts product, we can do more like, it is not very high, it is about 1,200 metric ton per annum, so 100 metric ton per month. So that’s where our permissions end so far as current situation is concerned at the Ekalbara site.

-

So we are right now seeing that our demand is expected to be steady and of course with introduction of new products that we are looking at, we can reach that kind of number between INR 900 crores to INR 1,000 crores next year. But more importantly, also we have to look at permissions, permissions that are available and permissions that we have right now got in terms of little bit expansion. And of course, we may have some possibility of doing some additional quantities at our job work sites that we utilize. So overall yes, it can be reached if everything goes well and we are able to get permissions in right time, within the normal time, because sometimes it can come in 3-4 months. Of course, not at Ekalbara site anymore because Ekalbara site, we have already reached the peak in terms of permission. But at job work sites, it may come. But sometimes it may take even 6-8, 9 months, months, depending on what is the record with the regulatory authorities.

-

We are not constrained by capacity. We have been constrained by permissions, but within permissions, we also, whatever capacity we have, we are trying to utilize to the maximum and also, as I mentioned, we have got little more ability or rather permission to increase our volumes.

-

FY23 we are looking at about INR 50 crores- 55 crores capex. When I say capital expenditure, it also includes the replacement of capital equipment. So out of about INR 55 crores, INR 20 crores will be for infrastructure, EHS activity, R&D activity, energy conservation activity and various other things. About INR 21 crores would be replacement of the existing facility and existing plants. And INR 16 crores is going to be for the new plant. Of course, the total budget for the new plant is about INR 36 crores, but in this particular financial year, we would be incurring about INR 16 crores.

-

There are three major elements that we need to consider when you are talking about Transpek. And of course, why customers have certain liking or interest for Transpek?

-

One is the very-very longterm relationship. For example, there are customers with whom we have been doing business since 90s. And they have full trust in us. So even if there are situations where the cost is a problem or a price is a problem or things like that, they always sit with us on a table and we sort out all the issues.

-

Secondly, our ability to provide the same product on a very consistent basis, batch-to-batch, lot-to-lot, and very-very high quality product, very pure product. And the service, the service quality that we have, in fact, all our customers say that when it comes to Transpek, we don’t have to worry about service.

-

From a technical standpoint, our ability to handle these various hazardous chemicals like sulphur dioxide, thionyl chloride, chlorine, and hydrochloric acid all these are very hazardous products and we handle thousands of tons annually so that is another ability that sets us apart. And most important thing in today’s time is the ESG, or environment, sustainability, and governance practices.

-

24 Likes

If anyone is attending AGM tomorrow at Vadodara kindly share notes here. Thanks

3 Likes

Transpek AGM 22 August 2023 at Vadodara

Chairman Speech:

Segment wise demand: Pharma and Agrochemical were subdued but polymer was better. Innovation in Polymer endues also contributed to growth

Company is among the largest player in Acid Chloride globally. Now also intend forward integrate and develop Non-Acid Chloride products which used acid chloride products as raw material. Also looking at developing products which address high growth market such as electronic chemicals.

Despite challenging environment, Transpek achieved highest annual sales volume and profit. However, Q1FY24 results were adversely affected by destocking in chemical chain. The management expect further 3-6 months slow down in the market and then recovery post December 2023.

Long term outlook for the company is positive but short term may be challenging. High energy price in Europe affected the end-use demand. Further, normalcy in logistic issue faced in past, resulted in stable supply and hence destocking of inventory whole chemical chain to normal level, which is working against volume growth. Further, competition in Acid chloride market has also increased with new players attempting to gain market share at cost of profitability.

In order to address this issue, the company is attempting to increase cost competitiveness in existing products, develop newer products/application/ geography. Recently company added new customers from Brazil/Japan/Korea which were not conventional export market for the company. It has also increase focus on sustainable manufacturing which increasing recycling of affluents.

The capacity growth for the company continues to be adversely affected to policy indecision about Ekalbara site. While pursing with regulatory authority for approval of new capacity, the company is simultaneously exploring alternative location for new greenfield expansion for future growth. During FY24, it intends to spent Rs 25-30 Cr on maintenance capex.

On sustainability The Company has continued membership with EcoVadis, and achieved Silver rating in EcoVadis audit. The Company is a member of the Indian Chemical Council and has taken many steps to implement ‘Responsible Care’, a globally recognized Chemical Industry initiative. Such relationships assist company in speeding approval of audit by large MNCs clients which are looking at use company’s product.

Question and Answers:

New Products: The company is pioneer in Chlorination technology. Thionyl chloride is base product which is used for Acid Chloride. The company has developed 3-4 new products which use Thionyl Chloride but are non-acid chloride products. New products current production volume is small but few of products have potential to reach Rs 100 Cr annual peak turnover in long term, while most other products are likely to reach annual peak turnover of around 30 Cr per annum. Peak turnover has assumption of price and full utilization of capacity of the company for the company being manufactured. This assumption may undergo change, so figure shall be considered more as indicative of market size and then actual sales.

Based on market enquiries and customer interaction, the company aspire to grow at 50-70% in next 3-4 years. Electronic chemical which are light in weight are increasingly going to get more usage in Electric vehicle (EV) replacing metal. Complex Polymers have higher strength and lower weight as compared to metal which place them at competitive advantage vis metal in EV. The company anticipate increased polymer use would also result in higher demand for its products which may work as raw material for polymers and hence optimistic about the prospect.

In current long-term contract, which is used in polymer, price is cost+margin basis. Company expects it EBITDA margin to remain in range of 16-20% of sales.

Previously company was selling Thionyl chloride in domestic and export market. However, 2018 onward, Thionyl chloride is captively used to manufacture value added products and exported. As a result, share of domestic market in total sales declined in past few years. The company is putting efforts to increase domestic market volume in medium term.

Approach to identity new product development: The company at times get enquiries from MNCs/existing clients which are looking at new product launches. Further, it also observes import export data in Indian market to explore potential target market segment new products. It also evaluates sustainability of products and its operational efficiency (which results cost competitiveness) for while exploring new products.

Transpek may also explore acquisition of certain capacities in case manufacturing base appropriate to company strategy is available at reasonable value. Hence, would continue to keep liquid investment on book for medium term.

Disclosure: Transpek is among top 12 holding in my equity portfolio. My view may be biased due to my investments. I am not SEBI registered advisor. I am not recommending any investment action. I may buy/sell above mentioned stocks without informing forum. Investor shall do their own due diligence before making any investment decision.

25 Likes

I heard there is a shift from chlorinated to fluorinated polymers because of environmental issues related to chlorination. this could be the reason for this company to available at cheaper valuations. if anyone is aware of it please share tia

2 Likes

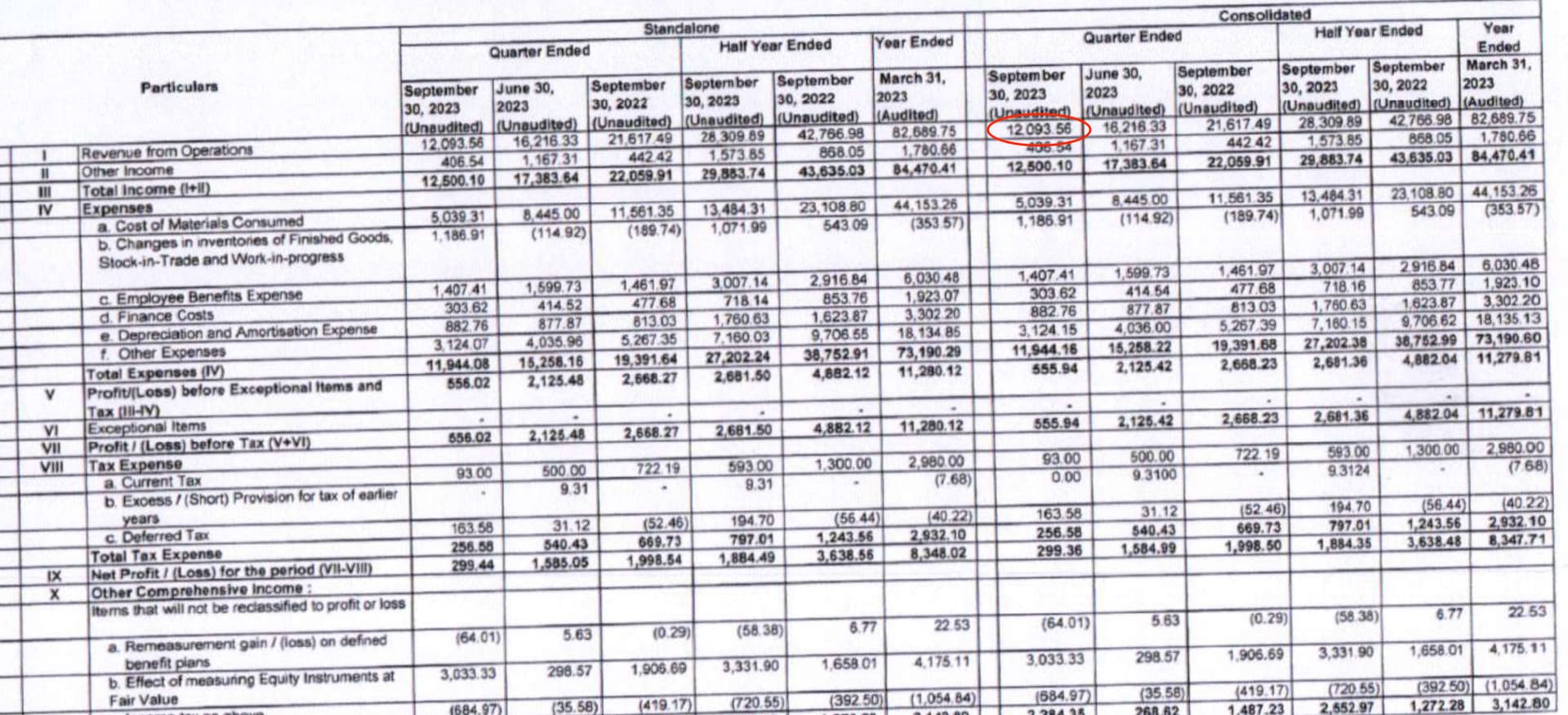

What could cause sharp downtun in Q2 revenue.… from 216 cr to 120 cr YOY…They did not gave any warning as such.

Management AGM did sound conservative. However, was not expecting such results. Having said that, broadly, decline in exports sales (my assumption) due to demand slow down in US may have adversely impacted sales during quarter. I hope same get recover quickly. My expectation would be moderate improvement in Q3 and Q4 and then normalise business in FY25. Let us wait for Con call to get more details and understadning of business.

Disclosure: My view may be biased as I it among my core investment holding. I am not suggesting any investment action. I am not SEBI registered advisor. I may increase/decrease/exit from my investment without informing forum. No trade in last 3 months.

5 Likes

Management had mentioned major destocking happening in Q1FY24 and this might be the spill over into Q2FY24. Need to wait for management commentary on this.

2 Likes

The investor presentation does nention destocking as one of the major reasons

Hello investors, what’s the best way to access the list of Transpek’s clients in North America? Since that’s where the bulk of the revenue comes from, before investing I’d like to check the number of clients and ensure: A) there is no consolidation due to large clients, and B) what other potential competitors these NA clients might work with.

I can share my findings with everyone here. Thanks!

1 Like

Hi,

Dupont is largest client for transpek.