Nuvama_on_Transformers_&Rectifiers_India–_Visit_Note_Engines_of.pdf|attachment (1.9 MB)

NUVAMA VISIT NOTE

2 Likes

Please pardon my writing skills, tried to summarize Nuvama notes below.

MD highlights favorable prospects amid a macro capex revival in power T&D, railways, renewables, etc.

Strong outlook,better positioning and lower competition (Chinese players exited the market)

Participating in INR37bn tenders with a 20-22% success rate, an INR21.5bn order book (1.6x FY23 sales),

Targeting 20-25% exports mix by FY26E/27E, and planned capex for solar and green hydrogen transformers.

Sees potential growth in sectors like railways, data centers, renewables, and green hydrogen, constituting new growth areas.

Outlook emphasizes capacity expansion and a focus on exports.

Any details available related to their renwable, greenhydrogen projects ?

2 Likes

Management is expecting improvement in working capital cycle and operating margin

6 Likes

Tried to understand based on a ready report.

V

Transformers and Rectifiers (India) (NSEI_TRIL) - Simply Wall St.pdf (2.2 MB)

After going through above report , What catches the eye is:

1.PE~100.

2.Fair value >800%

I tend to presume the above report might be based on insufficient data.

However screener presents more or less same PE

V

Although the stock price swings are extreme but it is continously moving in to just one direction.

The query - What is driving the price ? , is TRIL in froth zone ?

D-Invested.

First-generation company started by Mr. Jitendra Mamtora, a bachelor’s in electrical engineering, running successfully for over 4 decades under the leadership of Mr. Jitendra Mamtora, Chairman and Mr. Satyen Mamtora, Managing Director of TRIL

❑ Most preferred Indian Brand, known for manufacturing High Voltage Transformers viz. 220 kV 400 kV, 765 kV, 1200 kV indigenously

❑ Manufactures entire range of transformers viz. Power, Distribution, Furnace, Rectifier Transformers & Shunt Reactors, creating a unique positioning for itself in the transformer industry

❑ Supported by backward integrated manufacturing facilities housed in Gujarat

❑ International presence in 25+ countries

❑ An only Indian company who has the capability to manufacture **Green Energy Transformers. **

Major Highlights of Q2 FY24:

- Raised ₹ 120 crore by way of preferential issue on private placement basis in October 2023. 07742f7f-3d8f-4fcb-b626-8f38ffc41c1c.pdf (bseindia.com)

- Unexecuted order book Rs 2145 Cr: Break up as under

Central and State Utilities: 45%

Industrial Consumer: 40%

Renewal Segments: 9%

Export: 6% - Capex Plan for FY 25: 50-60 Cr for Industrial and Green Transformers side.

For future check: At the start of the year, they given guidance of Revenue of Rs 1400 Cr and double-digit EBITDA margin while till H1 FY24 Revenue was reported Rs 408 Cr and margin 6.52%

4 Likes

Stock EPS is shrinking and that’s what is concerning me at this point, given stock is at ATH. Looking to average up around 180, 200

Although EPS is shrinking, and next Q results may not be as blockbuster as the recent stock movement - this is a slightly longer play. Expect next FY to be great and the following even better, perhaps.

Recent guidance is for 3000cr revenues in 2 years.

2 Likes

Very good insights apart from the concall also:

2 Likes

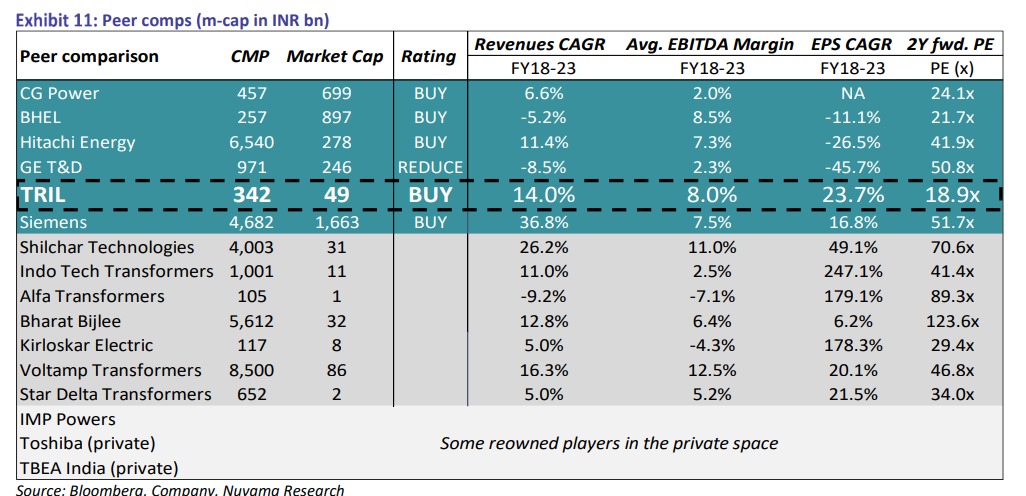

Page 5 is quiet funny,especially where Nuvama has given projections for the names out of their coverage. According to the analyst: Shilchar’s earnings are going to halve or fall even more,BBL’s earnings are going to fall by 75%,Star delta’s earnings are going to fall by 50-60% over the next 2 years and so on! All this while TRIL is going to have breakneck growth mostly due to low base of FY24(owing to various company specific issues)

Analyst seems to have extrapolated the revenue CAGR of Fy18-23 for all these names and extrapolated the exact margins. Thus,11% in Shilchar’s case,2.5% in Indo tech’s case,5% for Star,etc. seem to have been extrapolated. I doubt anyone would be so ill-informed to think that only one company(TRIL) with no particular niche is going to make 14-15% EBITDA while the rest are not going to have any margin expansion. The current numbers are already way better than extrapolated in the report. Other than Shilchar that derives major revenues from exports & thus makes margins head & shoulders above the rest,the sector is mostly homogenous & it’s not possible that only one company is going to benefit from power demand in the country & globally. Moreover,the pref & 500 cr QIP will lead to further dilution in TRIL’s case.In the meantime,no other transformer company has come to the markets to raise money.Even the ailing Alfa that turned around only this year has not raised money…so far atleast.

But other than somehow proving that TRIL is the cheapest name in the sector,the report was good.

Disc.: Not invested in TRIL…views maybe biased.

11 Likes

Fantastic news posted by TRIL today

3 Likes

Q4Fy24 Concall Highlights:

-

Achievements: Successfully tested the most stringent Dynamic Short Circuit test on multiple transformers of various voltage ratings. With this, it has crossed a commendable milestone of successful Dynamic short circuit testing on a record 150-plus transformers in the last two decades.

-

The technology for the 765 kV class shunt reactors has been fully absorbed during the year.

-

OrderBook: The Company received the highest-ever order inflow during the year of 2,050 cr. incl. the export orders of 11% with unexecuted orders of 2,582 crores.

-

Focus Areas: capacity expansion, being more export-focused, becoming fully backward integrated, exploring avenues for inorganic growth, and achieving operational excellence.

-

Operational Performance: During FY24, the revenue from operations was at 1273 cr., a 7% decline from 1375 cr. in FY23. For FY24, export revenue was at 139 cr., a 117% increase from 64 cr. in FY23. Export contribution as a % of revenue was 11%.

-

Orders in the pipeline: 17K crores of orders are in the pipeline, then anywhere between Rs.1,500 crores to Rs.2,000 crores should not be far-fetched.

-

QIP raised - 500 cr for capacity expansion and backward integration and inorganic growth opportunities.

-

Most of orders are on transmission side with power transformers of 220 kV up to 765 kV.

-

More focussed on orders of EPC contractors over state utilities due to better cashflows.

-

Current capacity: Its current capacity is 36,000 to 37,000 MVA capacity with 60-65% utilisation.

-

Capacity expansion of 12000MVA in Q3Fy25:

-

Revenue guidance FY25: Current orders of 2600 would be executed over 15 months with EBIDTA margins of 12.5-13%.

-

Challenging to increase the capacity and its focusing to reducing the working cycle:

-

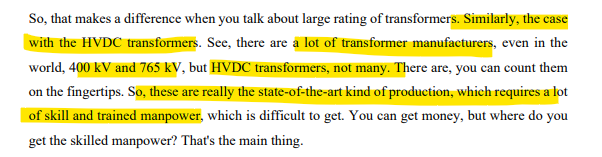

Not much capacity for 400 kV and 765 kV transformers and very few players have capability to manufacture those:

- Less capacity in HVDC transformers as it needs skilled manpower:

- Huge demand for scott-connected and V-connected transformers from Indian railways and Its RDSO approved as well.

- Company is having working capital cycle of 120 days & working on reducing this.

10 Likes

Anyone knows competitors of TRIL and what unique advantages TRIL has got over them? On Screener and Trendlyne I did not find their competitors in small cap space or in exact business line.

Should listen to Q4 FY24 Concall:

1 Like