Thanks @rajpanda - much awaited good news. Limited competition as of this date. Hope this late entrant can cover decent ground.

1 Like

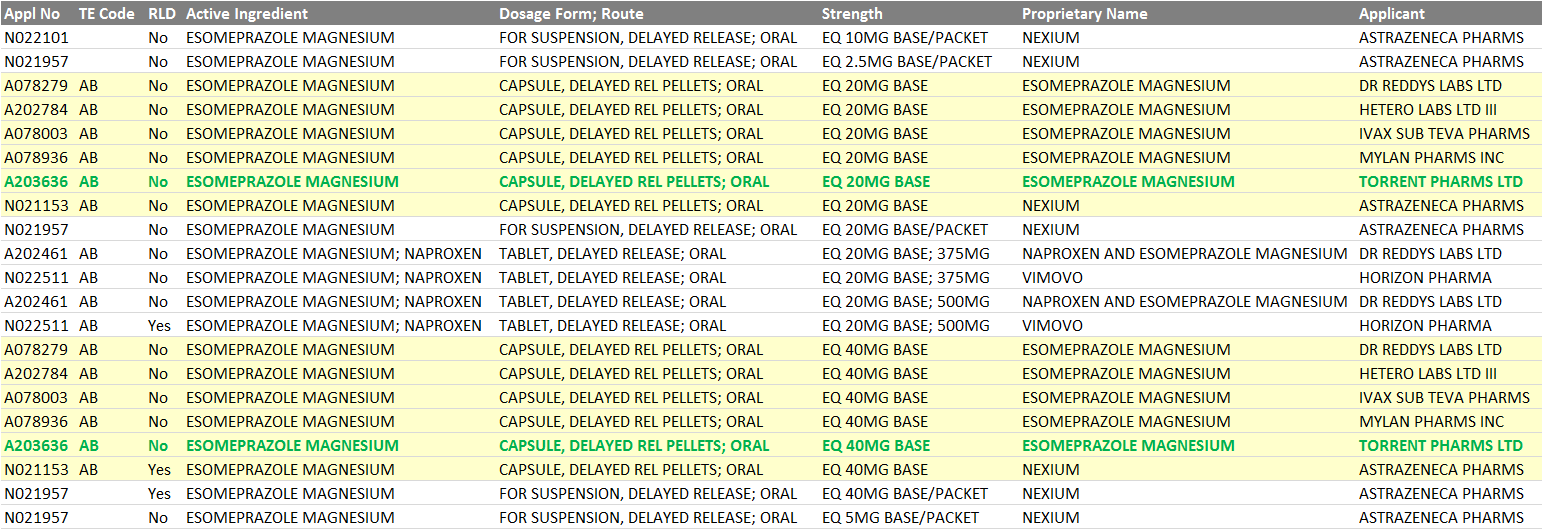

Before the entry of generics, the size of nexium was 6 billion USD. Now torrent gets approval and it is the fifth company to get approval for the molecule according to their NSE announcement.

The questions that need to be answered are:

What kind of price erosion has happened/will happen?

What % of market share will torrent be able to garner since it is fifth co to launch the drug?

Overall looking at the size of the molecule and limited competition, it augurs well for torrent if they can capitalise on this approval.

3 Likes

dr reddy got the approval around three weeks back and couple of research reports came out which tried to quantify the sales for dr reddys.

the reports mentioned that dr reddy’s can have revenue of USD40 mn in 2H FY16 and arnd USD 60mn for FY17 from nexium.

Torrent’s reply to the Nexium approval question posted by exchange-

Here Analysts are expecting 50mn$ for FY16 revenue. The icing on the cake is the margins which is expected 75%

Expecting more details from Concall for this quarter.

Torrent is gaining significant market share in Detrol. According to bloomberg data, market share of torrent in detrol has reached 7% for the week ending Oct 10.

Torrent has maintained 10% market share in Abilify. Alembic has lost market share after entry of Apotex. alembic mkt share now stands at 4%.

2 Likes

Vaibhav - where can i see the numbers?

Torrent Pharma Q2 profit seen up 153% on Abilify boost

1 Like

Any member having conference call details, please share.

Thanks in advance.

Dhiraj

30th Oct 2015 - Torrent Pharma @ 5:00 – 022 3938 1028

2 Likes

Great results from torrent pharma.

Atleast it has beaten my own expectations/projections by a wide margin.

Looks like abilify and detrol have contributed majorly to US business besides the base US business.

Cash and equivalents show a good jump.

There is still a lot of disconnect between standalone and consolidated numbers.

Concall would be interesting to listen in to as these guys give out more info than alembic guys on concalls.

13 Likes

Yes…Fabulous results.

Short term borrowings are NIL now. I was expecting some repayment of long term debt but management has parked money in current investments.

Tax expense is down (164cr vs 410cr) as indicated by management in Q1 concall.

1 Like

Consolidated Q2 2016 results:

Top line growth: 39%

Bottom line growth: 187%

India: Flat (Due to discontinuation of certain promotional schemes and hygiene initiatives)

US: 326%

Brazil: -18% (+19% on constant currency basis)

Quick updates from the concall today:

Ambition: to have best EBITDA margins in India.

Changes in domestic business (one time correction): some hygiene initiatives (stopped bonus offers).

Abilify: 6% share in Sep data. Some customers do not report data.

On a contracted basis, estimate close to 15% share.

350-400 million tablets. Next 12 months high favourable.

H2: share could be a bit lower.

Nexium: more than 6 players in US market. Large attractive market.

Manufacturing intense. Target to have high single digit market share.

Shelcal: expect price rise 10% in November. 45% growth in volume terms.

Detrol: next 12 months - 3 more players to come in.

Long term loan 2200 cr. No plan to reduce LT debt in near future.

Brazil: impact due to currency devaluation. 10% growth in value terms.

Steps taken to mitigate:

- Work on pricing (Improve)

- Work on cost base (decrease)

- Distributor margin (reduce)

Foreign exchange gain on net basis.

Receivables: Outstanding now 3 months and 9 days as compared to 4 months earlier

Inventory level is low.

ANDA filing: no filing this quarter.

Close to 20 products filed. Out of these expect 5-6 launches in next two years with limited competition.

Dahej facility: expect production/shipment to start before Xmas.

Expect increase in European tender business

European market:

Germany: main business in Europe. 16% growth in constant currency terms.

UK & Romania: short term slowdown.

Focus remains on Germany and UK.

Portfolio Derma close to 70 crore. Number 1 in face wash category.

19 Likes

thanks amit agrawal.

U seem to have covered most of the concall.

Some additions

US base business (ex abilify) remains robust)

Nexium… After approval co is in final stages of approvals with various players. Target slightly lower market share in the lower single digit.

Shelcal expect to take price rise in Nov. (it is 15% cheaper than competitors in India). grew 45%. Chymoral grew 78%. These brands are showing good traction even more than their glory years earlier when they were flagship brands of elder.

They dont share margins of individual products.

About balance sheet, they said ST loans have been paid. LT debt in immediate future, no plans to retire it. Internal targets set for keeping aside some fund for WC management. Implied that they want to be ready with war chest should an opportunity arise for M&A.

Abilify likely to remain attractive in US for torrent for next atleast 12 months. Since launch is at risk, too many players are unlikely to come up.

Detrol current competition is with mylan and teva. 3 more players may come up. But overall opportunity likely to remain attractive.

Chhatral last inspected in June 2014.

Change in domestic business aimed at improving long term health of co. in domestic biz. Co wants to be the highest margin co in domestic biz. (someone asked about comparision with Sun and they told that they want to reach and better that)

On MAT basis, co is No 1 growth co in domestic market.

In Brazil, every April govt fixes ceiling prices for products. Co is likely to raise prices where possible .

On R&D side, co plans to increase resources and add 1000 people. aim to take r&d expense to high single digit of turnover. (? a la alembic?)

Aim of increased spend is to increase filings in US. In current qtr there were no filings. But aim is to file 15-20 ANDA beginning next year. And increase complexity of products.

In India aim is to build a strong pipeline and copy whatever is possible in Brazil.

Zyg acquisition is meant to get a toe hold in derma segment. Co plans to shift its own derma division and brands to Zyg. Its face wash (I think they were alluding to ahaglow face wash) is no 1 face wash brand in India. derma sales was 70 crores. Zyg is not into big opportunities. But is mainly to open its account in dermatology and not score a straight century.

Outlook for next 2 years. pending filings at 20 and 5-6 products have high chances of providing attractive opportunities.

In abilify co is in market share preservation mode. It is taking care of bigger customers and making them stick. Smaller customers are being addressed by newer players who have entered late. Abilify used to be a 30 dollar tablet for innovator.

Dahej nearing completion. EIR expected anytime soon and shipments to begin soon to USA and other markets before Christmas.

Dahej facility helps co in increasing supply and market share in existing products. Also it helps co to bid for bigger quantities in the German tender business. Its German arm Heumann has strong expertise in the german market. Germany remains an attractive market despite being tender based. Germany growth was 16% in constant currency terms.

UK and Romania have shown some slowdown. But in Romania due to changes in govt policy, generic players are likely to benefit.

Zyg sales 10 crores and profit more than 50 lacs. 2 NDDS preparations in dermatology in foam preparation to be launched soon.

Co is optimistic about Crestor whereas in Viagra they didnt seem confident. But they already have Sildenafil launched in US markets for off label Uses mainly in pulmonary hypertension where it si seeing good traction.

Complex NDDS evaluated for ROW and Brazil. At a later date even launches in US and Europe may be considered.

Overall the management commentary seemed fairly confident and positive.

29 Likes

hi hitesh,

the market reaction took me by surprise. (i know pe based valuation is not correct considering the one off huge earning. but still its 15 pe when almost all other pharma companies are > 30)

any views?

gautham,

Initial knee jerk reactions are often difficult to decipher. I recall even after stellar q1 results for torrent stock corrected next day and then after some consolidation took off.

I think one of the reasons for the correction could be concerns about FY 17 and beyond as the pipeline of products in US for torrent is perceived to be not so great.

But my take is that after listening to the concall the co seems to doing quite well in the base business in the US and with increased shipments from the Dahej facility, the base business might get additional filip.

The company’s aspirations in the domestic business also seem to be quite high and even if part of it materialises there could be much higher profit growth as compared to sales growth.

And again the Dahej facility could facilitate the company’s business in Germany and europe due to enhanced capacities.

Valuing the company based on fy 16 numbers would not be the right way. In fact its very difficult to value a company where we know bcos of off and on US blockbuster molecules earnings will be lumpy.

But looking at the kind of batting the company has done on a favorable wicket (abilify in the US), it seems to have done a brilliant job and increases the confidence as an investor in the company’s ability to exploit favorable situations in the US market.

16 Likes

Crestor is a quite a big molecule for fy17. it is $6b and a growing molecule, They seem confident of doing well here.

They also mentioned in next 2 years there will be about 20 launches of which 5-6 will are very lucrative launches with limited competition.

Besides that, they are hiring a lot of R&D people of around 1000, and increasing the filings. The increased filings will start from q1fy17.

So from fy17, we will see increased filings with increasing complexity of ANDA filed (like cream and ointments and some would that would require clinical trials too) . Oncology green field plant is another positive.

They would also be launching many first timers in india with innovative dosage and combinations ( I think this is ajanta like strategy) and then replicate this india model in brazil.

Tax rate was 36% in 1H and will from fy16 point of view, it will be 25%. so, H2 there will be reduced tax rate.

21 Likes

A recent report from Motilal Oswal

http://www.motilaloswal.com/site/rreports/HTML/635820540119163918/index.htm

Discl: Invested

2 Likes

TORNTPHARM - Torrent Pharma’s new Plant at Dahej Commences operations https://t.co/9R64kDb0Gs

6 Likes