I think general market growing at 14% n unorganized to org should add further ad per CRI|SIL estimates. also , once young India starts getting old , I think after 8-10 years there could be sudden spikes in above normal demand growth . Remember, Mr vellumani citing this in an interview . Demand for sure not an issue unless disrupted .

Underestimating Jubilant was one of my mistakes of 2017  . We learn every year

. We learn every year

I did some comparison between Dr Lal and Thyrocare.

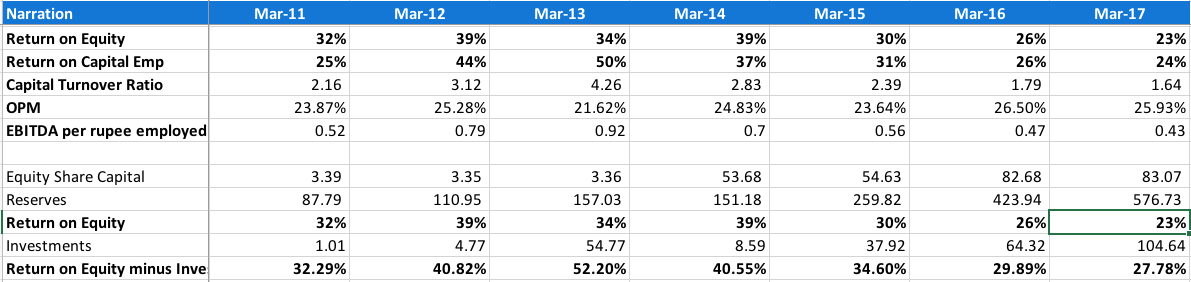

For Thyrocare, RoE is at 18% because of the large portion of equity is locked in investments. The metric without the investments is not bad at all (at 60%) and is in fact improving. I don’t know if there is a need for this cash. If there isn’t maybe a part of it can be deployed in marketing to improve the topline.

Although the OPM is dropping down from high 40s to low 40s, the capital turnover ratio is in fact improving (1.38 in FY10 to 2.41 in FY17) so the company is actually generating more EBITDA per rupee of capital employed. Current Net Block (89 Cr) + CWIP (2 Cr) + WC (33 Cr) of the company is only around 125 Cr. With 290 Cr in cash, the company clearly can fund its growth going forward quite easily.

Now looking at the same data for Dr Lal Path labs

The difference is night and day! Although optically Dr Lal has higher RoE, EBITDA per rupee of equity employed has been deteriorating along with its RoCE because its Capital Turnover ratio is falling along with its OPM unlike Thyrocare where the Capital Turnover Ratio has rescued declining margins.

Similar to Thyrocare, Dr Lal as well is sitting on investments making its RoE low but not to the same extent as Thyrocare. RoE without investments is at 60% for Thyrocare but is only 28% for Dr Lal.

15 Likes

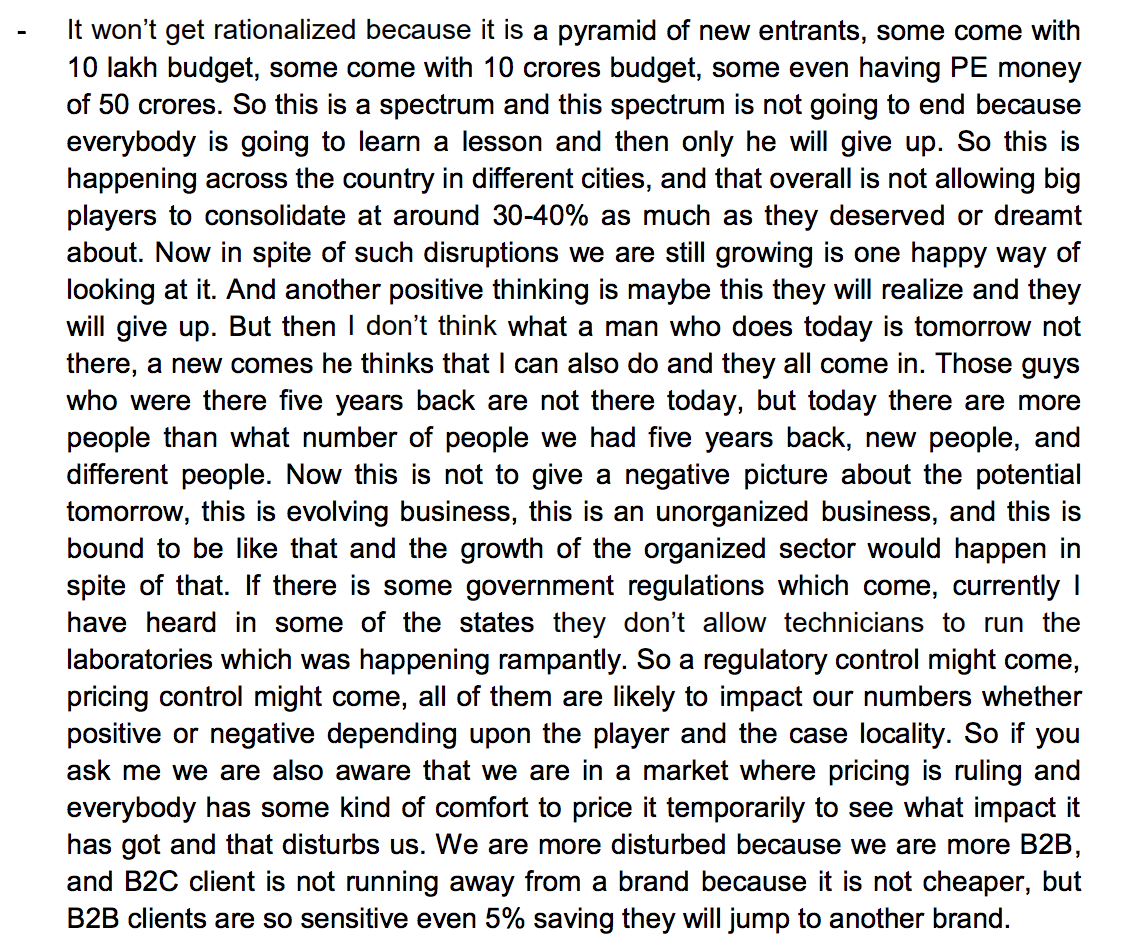

@phreakv6 Buddy, coming to spending on marketing, there are lot of interesting insights in concall transcripts. If I remember, the two most important insights (but let me recheck n confirm as I don’t remember exactly which quarter ) -

- Mr. Vellunani said advertisements ROI has not been so lucrative and hence they are cautious about it

- Promotional discounts is something which he uses it to balance between top line growth and margins . Last quarter , Mr. Vellumani focus was more on margins and he said he will explore if they can use it to drive top line based out of two , which one needs immediate focus.

There is lot of business information in concall transcripts and I am sure you will go through it.

Coming to Lalpath and thyrocare, I think both in terms of products and target segment market, there are noteworthy differences and that might be reason for the same though I have not done an item to item expense comparison. One more thing, I was not very happy with lalpath salary and remuneration distribution and that’s where Mr Vellumani seems far ahead of competition in overall governance. Last thing, thyrocare was investing a lot in cancer MRI diagnostic but latest tone has been more conservative as they feel they are too early in game to generate good return on capital . So, I see lesser possibility of relatively higher capex deployment

2 Likes

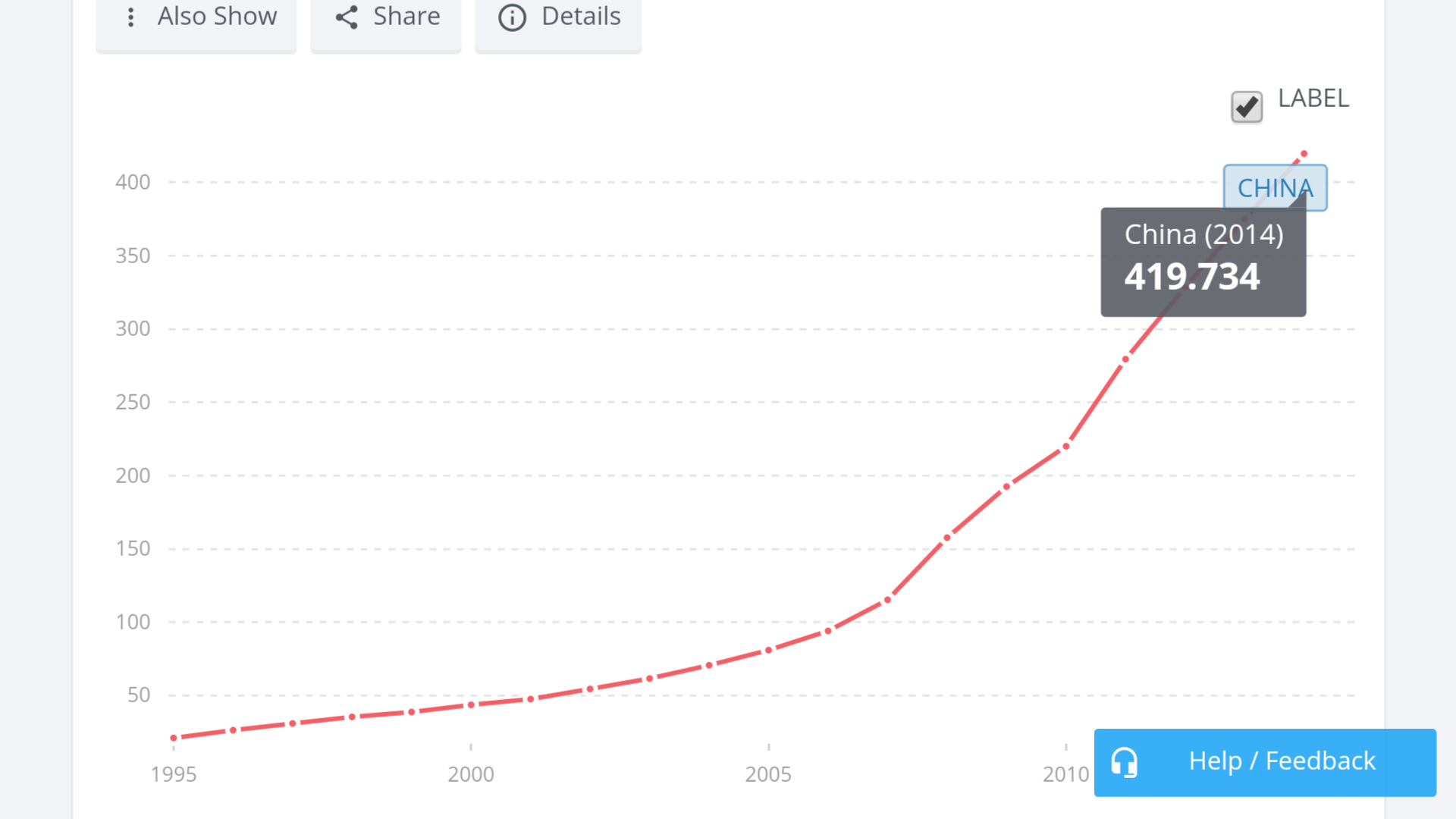

In China, between 1995 and 2007 per capita health expenditure grew at 15.2% CAGR.

But, 2007 onwards there was acceleration in spending.

Between 2007 and 2014 per capita health expenditure grew at 20.2% CAGR.

The median age in China crossed 33 in 2007.

It’s likely that quickened expenditure on health care is because of rising age.

India is expected to cross median age of 33 years around 2030.

It wouldn’t be wrong to expect a steep rise in spending on diagnostics in India as well by then.

Technology obsolescence could play spoilsport.

7 Likes

True @shreys

This has been rightly pointed out by Mr Vellumani also in Indian context. After 8 years , he is expecting a similar spike fueled by ageing population , higher awareness, better insurance penetration n more spending power. We ve highlighted this here somewhere above in the thread .

Thanks for your detailed analysis,your views r very useful to me

Why is Velumani hoarding cash. If he cant deploy it he should return it to shareholders right?

I like businesses that hoard cash instead of deploying it helter-skelter. If there isn’t a better opportunity for the cash, why not wait? When the PE funds go on a spending spree, you never know what you may have to do to defend market share. I see the same behaviour in another company I am invested in, in Info Edge (Naukri, 99acres). They too hoard cash ready to deploy in 99acres when their competitors go on a spree or in Investee companies when a good opportunity shows up or for subsequent rounds in Zomato or Policy Bazaar.

I don’t see anything wrong in hoarding cash especially in a growing business where indiscriminate spending won’t directly result in topline growth. That’s the difference between linear businesses and non-linear ones. In linear businesses, more cash spent in capex or marketing will lead to more sales but in non-linear ones, you must wait until a competitor makes a move, or until the market is ready (- For eg. 99acres spending money on marketing during demonetisation would yield no results) or until a better strategy is ready. As long as you trust the management to deploy cash wisely, I don’t think it should be a problem.

8 Likes

Not many companies are generous enough to return cash. HMVL, another company with significant cash languishes at relatively low multiples because of the high cash retention. They kept assuring minority investors that they were accumulating cash which would be deployed in favourable opportunities. Also, at one point it was said that cash would be returned to shareholders once a threshold was crossed. Threshold was crossed but there was no mention of rewarding shareholders.

So, more often than not company won’t distribute cash.

1 Like

There is a plethora of cos and business models in the organized diagnostic space due to the opportunity size. Business wise, the diagnostic segment is an adjacency

For e.g - a pharma co can easily enter this market to shore up margins and create growth for itself ( e.g Mankind Pharma - https://www.pathkindlabs.com/). Another example is Apollo Hospitals ( https://www.apollodiagnostics.in/)

This creates a ever changing business environment which is ripe for consolidation because thats the only viable route to grow. SRL and Dr Lal to my knowledge are the the only Rs 1000 Cr enterprises. Thyrocare is about 1/3rd the size with a revenue of 330 cr.

Metropolis’s Ameera Shah is also upcoming and appears to be a very growth oriented entrepreneur.

Similarly there are very good diagnostic chains with different pricing structures across the value chain ( for e.g Krsnaa labs provides MRI scan at Rs 2500 - a steep 50% discount compared to other places )

My calculations suggest that the overall market size is about 50,000 - 60,000 crores which is quite large and attractive. This has attracted a lot of PE funds including the ones who invested in Thyrocare. About 20% of this large 60k cr market is served by the organized players , so about 10k - 15k crore. The existing large players are all vying for this slice while new players are being created through adjacencies making it tough to generate volumes.

While the overall market size is large , the sheer competitive intensity should cap market share for any individual player slowing down growth in the domestic market. However, the export of services remains a possible growth area which is currently untapped.

Assumptions while calculating size of market.

Population of India : 128cr

Urban ( 35%) & Rural ( 65%)

No of people who cant afford any tests : - 40% ( Urban Poor ), 60% ( Rural poor )

Age bracket 0-24 dont need tests, 25-54 - 1 time per yr ( urban ), 55-64 ( 2 times a yr, urban ), 65+ ( 3 times a yr, urban )

Rural people are 4 times healthier and require 1/4th the times the tests required by urban counterparts

Cost per instance tested - Rs 3000 ( urban ) & Rs 1000 ( rural )

A good report to understand the landscape is given below

https://www.edelresearch.com/showreportpdf-36374/HEALTHCARE_-DIAGNOSTICS-_SECTOR_UPDATE-APR-17-EDEL

The other two threats one should factor in is technological disruption and government interference in the pricing as already indicated in the Economic Survey 2017-2018 (https://economictimes.indiatimes.com/wealth/personal-finance-news/over-1000-difference-in-medical-test-prices-across-cities-will-govt-standardise-rates/articleshow/62696175.cms)

In my view, one should try and get a sense of how the future is likely to unfold in the diagnostic space before considering an investment opportunity.

Best

Bheeshma

Disc- Exited Thyrocare a few mths back

4 Likes

Would you please clarify the following ?

Was this assumption (that any individual player will have only slow paced growth) the primary concern for exit when you compare with other opportunities ?

Disc: no investments. Looking at Thyrocare and diagnostic sector and trying to understand the sector.

The primary reason was that the business landscape in the diagnostic sector is such that scalability is difficult for any individual player ( even if low cost ) due to the commodity nature of the tests, low entry barriers and presence of a lot of players - all looking at the same potential customers. Established players have had a good run in the last 10 years due to the lack of competition & rivals but things are changing in the sector with the rise of a lot of players with different value propositions. This is evident in the way sales growth has panned out for both Dr Lal and Thyrocare. The trend indicates a definite slowdown/reduction and i expect that to continue. The return ratios are good for both the cos, but if we are paying a high multiple - there needs to be evidence that the co is well positioned to reinvest incremental earnings at those return ratios. The ROE trend does not indicate that the cos have been able to do that.

Dr Lal Sales Growth rates

| 3yr | 4yr | 5yr | 6yr | 7yr | 8yr |

|---|---|---|---|---|---|

| 38% | 33% | 29% | 27% | 25% | 23% |

Thyrocare

| 3yr | 4yr | 5yr | 6yr | 7yr | 8yr | 9yr |

|---|---|---|---|---|---|---|

| 37% | 32% | 27% | 25% | 26% | 26% | 24% |

Dr Lal ROE trend

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|

| 31% | 39% | 34% | 34% | 28% | 26% | 23% |

Thyrocare ROE Trend

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|

| 55.2% | 36.8% | 34.1% | 35.5% | 22.4% | 17.6% | 15.7% | 17.8% |

2 Likes

I will talk about Thyrocare only. ROE, as @phreakv6 said is visibly low as it has 300 cr investments. ROE would have been much higher if this cash would have been distributed or was just not there. Capital turns are increasing here, so capital is being used efficiently.

As per Du Pont analysis, it is financial leverage which has fallen drastically (due to investments), making ROE low over last 4 years. I will not get too much worried about this as what matters to me as an investor is above average margins, good asset turns, good capital turns, at a decent price.

There are big tailwinds for this sector -

- Population growth

- Median age

- Medical insurance penetration

- Regulations will come in at some point making life tougher for smaller non compliant labs

- Low cost players and efficient models will be the winners.

- Opportunity in neighboring countries

Imagine, if price regulations come in at some point, who would get hurt the most? Player A with 40% EBITDA, Player B with 25% EBITDA, or Player C with 10% EBITDA?

As per Velumani, this business is at the moment all about volumes. Reducing margins by few hundred bps would give them much needed volumes and above industry growth.

Regarding Edelweiss report, it is lopsided. The analyst had made up his mind that this sector would go downhill due to competition even before he started working on the report. Competition is everywhere (where margins are supposedly higher). Leave apart competition, i see disruption as a major risk, which this report fails to mark as threat. The report doesn’t even talk about profitability of new players. Just talks about plans and volume growth. Are they profitable? What are the pricing points? Are they cheaper than Thyrocare? If they are cheaper than Thyrocare, what are there margins? Can they sustain without p/e funds (for how long)? If margins shrink, will pe funds still stick with the businesses despite lack of profitability (like what happened with other sectors like food startups, e-com players) while these guys burn cash?

Velumani has worked up a model, which is working like a charm.They do not need much capital to grow! They don’t want to advertise much as that advertising impression doesn’t make a lasting impact (they tried). So, traditional (costly) advertising is basically waste of money for this sector. Cash/Investment gives more security when i think of my investment. This can be deployed whenever there be a need. The guy understands that incremental return should match the existing returns or should be better. Opportunities will come. The guy understand the business very well. Look at how they stopped expanding MRI machines as he felt the growth wasn’t there as was expected. So he is not going to spend cash recklessly just because he has it.

The stock has corrected from 54 p/e to 35 p/e due to these deemed sectoral headwinds. But if i am getting a 50/60% ROE player, with zero debt, cash of 300 cr, growing at 25% cagr, at 1.6% div yield, in a growing sector with increasing competition, with Category A management, i will take it anyday.

18 Likes

I took it at 54 PE for the same reasons. I think market perception matters a lot in commodity kind of businesses. I would have liked to have more dividends (may be 80% of profits) since they have enormous amount of cash.

Disc.- It is my largest investment by amount invested

Hi @Mridul

If one nets out cash from equity to compute return on equity then in case of thyrocare that comes to about 57 per share of cash. The book value is 91 per share. Net of cash the book value is 34 leading to a price to book of about 19 -20 times albeit with a higher ROE - which in my view is quite high. As far as financial leverage is concerned it wasn’t too high to begin with so am not sure that meaningfully impacted ROE.

The growing pile of cash suggests that company will probably have to grow through inorganic means to scale up but its unclear at this point how.

The good part is that the business size is quite large so it should not be a challenge task to find a good use for that cash.

In any event differing perceptions make the market like they should.

Best

Bheeshma

4 Likes

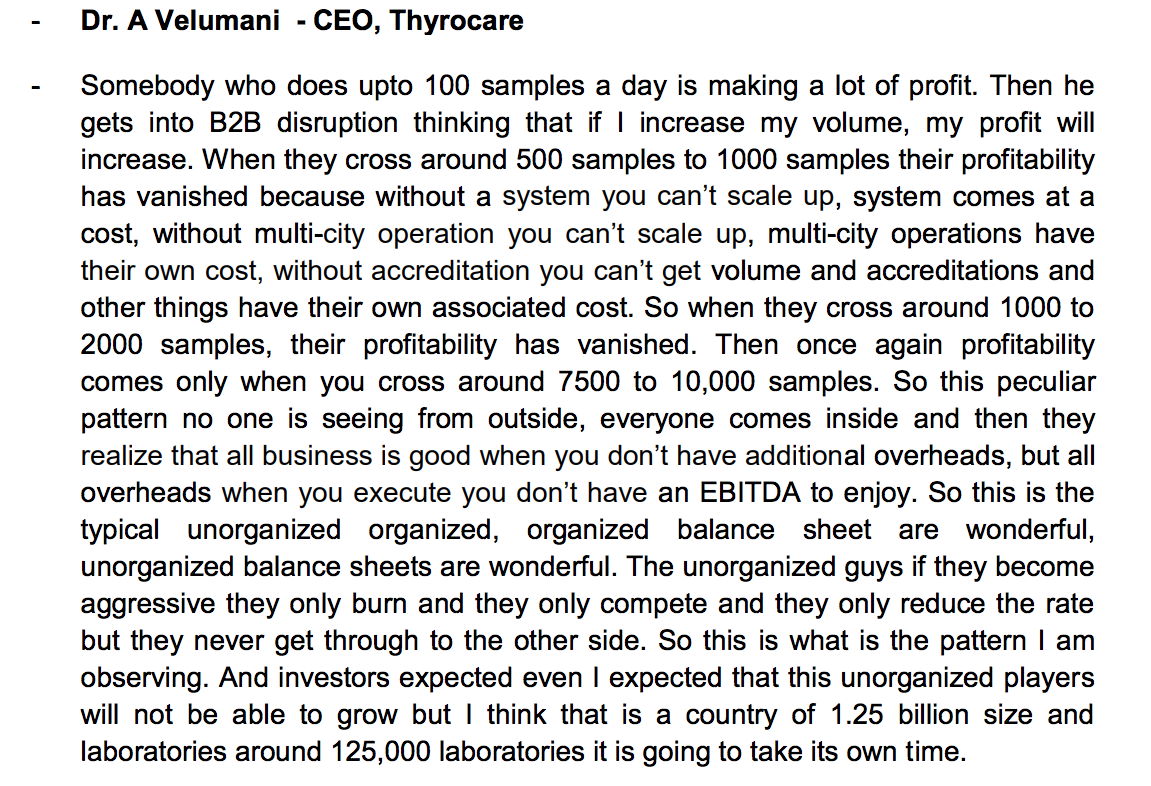

Some important parts of the latest concall that I thought was relevant for the discussion we were having. There are parts were you can sense Velumani’s annoyance and tinge of disappointment with the PE money in the sector.

On PE players and their deep pockets.

This was very deep insight on scaling and why it is difficult for new players. The systems and processes come at a cost. You cannot merely throw money at the problem.

On sacrificing EBITDA margins for volumes

He seems to have a problem with marketing spends as it hits margins at the cost of topline growth and this can be seen in Q2 and Q3 of FY17 where OPM dropped to 18% and 28% levels from 40% levels before and since.

I think I sort of disagree with him here as I think in a business like this revenues may accrue in subsequent quarters as well. Someone who sees an ad for Thyrocare may not have an immediate need but in the next 3-6 months he may give a business, so judging based on individual quarter where marketing spend was done I think is unfair and short-sighted. I might be completely wrong but having done analytics extensively for online marketing and tv/radio spots by attributing subsequent revenues to day of airing of a spot and sometimes even to station/channel and times, actual business in terms of lifetime value comes much later than the time the marketing spend happened for businesses like these.

And then the final one where he explains that what they are doing in terms of “illness” is not actually illness at all - as in like diagnosing a fever but its an à la carte test under the wellness package.

This whole wellness vs sickness thing sounds like evidence of absence vs absence of evidence to me. One is easy to do - absence of evidence is what Thyrocare is doing while evidence of absence could involve more involved testing where a series of sub-tests may have to be done.

10 Likes

Certainly. There’s scope for expansion in neighbouring countries as well as outsourcing of testing from foreign countries to India.

But, foreign companies, experiencing saturation in their home countries may also expand in India if there’s enough promise.

And, Quest Diagnostics, one of the largest clinical laboratory companies in the world has already set foot.

These foreign companies don’t require PE money. Their parent companies are deep pocketed, experienced and worthy competitors.

Let’s not discount the growth of global laboratories in India.

With time there definitely will be growth of the organised sector. But, its entirely possible that foreign diagnostic companies will offer tough competition.

And, I feel that no company will be able to occupy a major share of the business.

In the US, Quest Diagnostics, a company with sales exceeding 7 Billion$ had a 9% share.

And, they were the market leaders serving 1 out of 3 American adults.

Even the US diagnostics industry is a fragmented one.

Just my thoughts-

Over the next few years, the share of organised sector in the business will increase.

But, the competition in the organised sector will also increase.

And, the numbers sure are impressive.

But, in my limited understanding, when margins are very good it seldom sustains.

Other players would also want a piece of the pie. Supply increases and numbers moderate.

As always, I may be completely wrong.

3 Likes

A simple filter to use here is from the WB quote: Would you still buy this stock if right after the purchase the stock market were to close for ten years?

My personal view - I would not. As @bheeshma said, this is a commodity type business with high competitive intensity and low barriers. In 10 years time there is a high chance that this will be disrupted.

@phreakv6 your marketing comments reminds me of a famous marketing analytics quote, "I know half of my marketing budget is useless. Problem is I do not know which half " ️. Usually , in analytics data driven world , we do this by something called a market mix model which can be intelligently designed to take care of lag effect (the point u highlighted ) ,interaction effect (TV adl eads 1 , billboard ad leads 1but when Both happen leads 3 due to interaction effect ). I would still say there are higher chances that the man running the show with full attention would know better than us but to get further insights we may ask him in concall his ad ROI decision making process in more detail.Many times beyond a point even data does not suggest anything significant and many times business experts do not buy data driven arguments as data works under many hidden constraints about which the business experts are aware and sometimes they get biased by their own intuitive process. Tough world

2 Likes