https://www.bseindia.com/corporates/anndet_new.aspx?newsid=20e14769-091c-446f-98bd-068c97a19dde

A decent result in Slowdown

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=20e14769-091c-446f-98bd-068c97a19dde

A decent result in Slowdown

Dont think you are alone when you say this business does not have moat and barrier to entry aspects and I think quite a few have raised the issue. Think highlighted the same point on this thread on 5th or 6th post (early days of investment journey with serious interest as well as hands on activity and hence could make lot of mistake those times). Also, that time I was of opinion Lalpath is better model but what later on did not like is some of management acts. Post all research, ended up selling both IPO positions due to concern over valuation the kind of PEs these were trading at

Now, why I am tracking it again with a small position. In fact for me, whenever a discussion happened on Thyro, my main issue was what is a sustainable margin and where the fall could stop and the only reason I could see is one at which some of existing players start getting out of market who compete directly with it.So, we agree on lot of parts but differ mainly on ability to see things clearly few years down the line and investment styles. Also, had it been super attractive by valuation, would have picked a higher stake but do not feel that either. Personally, identifying winners in advance is not my skill and hence try to work under limitations and hence what suits one may not suit other. Like to go more with execution, buy in bad times, sell in good times kind of guy. There are multiple ways of making money and multiple styles - some do through concentrated and some do through diversified and some do just by timing index investing also. Key is knowing our strength and sticking to it. Also, if only high moat businesses has value,then, market will be left with 20 stocks and other wont find buyer but it does not work that way.if we simplify, there could be category A+ companies (if one could identify them), A,B and C on business model, keeping management quality, longevity, growth etc aside. Thyro might be in category B is my mental assumption and I could be wrong. Also, I am not a believer of moats in this disruptive world. Moats look good till earnings are intact and prices go up. At least, it is not my cup of tea as of now. So, principally agree on stock view and differ on investment style and skill set. Coming to Lalpath, I have issues with Lalpath corporate governance. Look at the kind of things they have done on compensation side through stock allotments. When stock does well, market finds reasons to appreciate and when it does not, it finds all the flaws in the world. We need to choose which flaws we are willing to choose and live with. Infact, on Thyro too like Mr. Velumani’s honesty but think he needs to get over lot of this other stuff and focus more on core activity. All in all, currently it remains a 0.5% allocation which I am tracking closely as well as relatively with other options and see how they execute over a period of time and how valuation attractiveness emerge. Infact, if one tracks US counter parts, diagnostic trades at ~15 valuation. Considering in India, still there is enough scope in terms of coverage and age factors for market size to go up, a 22 PE may not be obnoxiously priced. Now given, we agree on business quality and all, would like to know, how would you like to valuate Thyro and what is the valuation range you would provide? In case, your model is not at all to look at non-moat companies at any valuation, that is also an investment style and totally respect. My estimate is keeping other assumptions intact , I would like to double my position every 10-15% fall with max allocation threshold of 4% which means average price come around 360 Rs which comes around 16-17 PE with a hope that bottom margins would have formed by that time and loss making players would get out of market

Some notes from annual report:

Company provides 51 test profiles under arogyam brand

Revenue up 12% and PAT down 9%. PET CT grew at 33% but yet in losses. 53% revenue from preventive care

30% increase in workforce , 300 new hires and 1210 employees now, yet to contribute on top line side

Plan to grow more on B2B (78% of sales) than B2C(22% of sales) as B2C needs significant customer acquisition cost

Following points led to under performance:

Wont invest further in PET CT till it break evens. Oversupply in PET CT market. Currently, 14 PET CT scanners

New focus areas: TB Diagnostic (2.8 million annual count of people who develop TB)

and prenatal screening test (non-existent in India due to high cost, offering at 8k against 25k market rate)

Management continues to take low salary and promoter stake increased by 1.75%. Mutual funds reduced stake by 5.3%

Open questions/concerns:

Just price being lowest is not a strategy for new business lines, what different they will be doing that they can make profit on that low pricing and other can not or what stops others from doing the same?

What lessons learnt from PET CT which will not get repeated in these 2 new lines of business and if they are asset light why wont others do the same? Realizable market size opportunity?

Company talks of removing middlemen as they are not passing pricing benefit to end consumer. Is not the overall business well connected through IT, systems and processes? How come it is getting bypassed?

Number of B2B partners has doubled but revenue growth is not inline. What should we infer from this , scope for growth or stress on revenue per partner?

5841 customer complaints received. Would be interesting to compare with competition on an apple to apple basis

There is 30% increase in sales incentive but revenue growth is only 12%

Can anyone explain the exposure towards equinox and rationale?

Disc: tracking position around 0.5%

Hi Saurabh,

I wanted to get your opinion on two points:

So, basically both should have different machinery and different markets. And hence they are not competitors.

In short, he forewarned that he is going to slash the rates and get the volumes. And that makes some sense.

Thanks.

I would like to disagree on this front. Every city has local players with age-old reputation but with fewer diagnostic centers. In my city Kolkata there are Drs.Tribedi & Roy Diagnostic Laboratory, Ashok Laboratory, Quadra Medical Services etc. which draw customers based on their name (brand). I have seen many preferring those over nearby low-cost players, & even Thyrocare / Lal Pathlabs because of prolonged reputation.

I believe in this space word-of-mouth marketing works better than traditional A&P via media, and that takes years to bear fruit.

In that case, Mr.Velumani is probably thinking on correct lines. To beat the local players, cost and incentives are important factors. Thyro is reducing margins and expects to rope in more business. If volume continues to increase along with cash from operations over the next several quarters, then one could assume that the ruse is effective.

The local players may not be able to fight the mighty listed company, Thyrocare, which has access to cheap funds. The machinery is fairly expensive I hear. And providing good quality at low cost could be effective. On that front, lets see what happen over the next few quarters.

I think the share price should face corrections since the management has given a guidance of lower margins. This is a growth stock, but not in the standard way.

Its website looks up-to the task; determined for disruption.

I believe, Thyrocare, Dr. Lab like players can still get enough volumes, driven by their own campaigns and the aggregator apps like 1Mg, Pharmeasy. The forementioned local established brands have smaller number branches & won’t able to serve too many customers in metros. Also, the free home service, collection, delivery & real-time tracking will make life much easier at a more affordable cost. Indians being cost conscious & the new-gen populace being more devoid of time, these added benefits would attract them.

I reckon the inclination towards the established local brands would remain limited to elders & the conservatives, as the inquisitive young generation can quickly understand that there are not much differences between the facilities & services provided by the established and emerging players.

However, some of the aggregator apps like 1mg & Medlife has started their own diagnostic chains too, like private labels of retailers, & they are supposed to promote those more because of greater margin. Sastasundar on the other hand is not an aggregator & has its own diagnostic chain Genu Path Labs.

Not sure whats happening with the independent valuation of PET CT business? There was no mention of it in the concall as well.

Established and larger players in the diagnostic industry in India have a long run way in my view and they will gain at the expense of smaller labs. Also, I think many hospitals will start to outsource their lab operations to firms like Thyrocare. Also ageing population and high prevalence of lifestyle diseases (due to poor diet, lack of exercise and increasing awareness) in India will also aid the growth of diagnostics industry.

Thyrocare valuation has come down significantly (due to the drag from PET CT business).

Discl- continuing to accumulate from IPO (now in the top 200 investors)

Thyrocare’s new website about pre-natal screening tests during pregnancy

Such a genuine promoter… No salary…socially responsible thoughts… But As per AR Co spent only 1cr for CSR against 2.3cr it is required to statutorily… Doesn’t effect valuation but reflects on management …given the public image they have created

Disclosure- Invested

With its IPO out only in 2016, I feel the market has still not “discovered” the right price range for the stock.

Margins too have reduced, Thyrocare being a midcap stock, I would like to see what this does to the stock price.

Not sure why market is only giving half of the valuation that market giving to Dr Lal and Metropolis.

Though the business / model is little different but run way and economic characteristics for all three are more or less same .

Would appreciate if some one can help share their views .

Since most of the revenue of Thyrocare comes from hospitals (B2B) so i do not find it surprising that it gets less valuation than Dr Lal. An individual customer of Lal path will not know how much profit company is making from these tests but a hospital will always know how much profit Tyhrocare is making from the tests so hospital will allow it to charge only cost plus x% only and this x% will be dictated by hospital, not Thyrocare. This is true for all B2B businesses and that is the reason market gives less valuations to B2B.

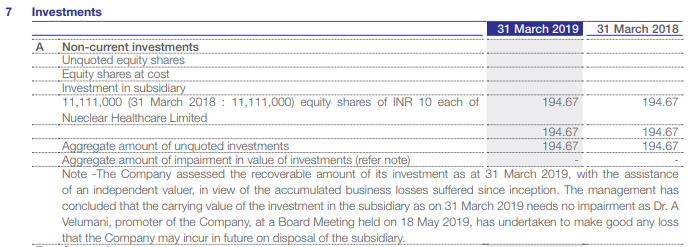

Whatever the drama happend 4 months back for buying back the business and all just because the promoter is too emotional comes to end thyrocare is not proceding with the selling of neuclear business to Dr Velumani it seems his focus will shift and he will not focus on listed Thyrocare and might focus on neuclear business holding the share from 2 years i will sell and get out i don’t like indian serial drama in company @vivek_mashrani Request your view on to that if possible

Any resolution happened in this matter? Is neuclear contributing to Thyrocare revenues today

Board meeting outcome as conveyed to exchange:

The Board of Directors met today to discuss about the offer of Dr. A. Velumani, Chairman,

Managing Director & CEO to acquire the shareholding of Nueclear Healthcare Limited, the wholly owned subsidiary. The Audit Committee, which discussed the matter prior to the Board Meeting, had reviewed the valuation reports received from Karvy Investor Services Ltd. and noted the long gestation period of this business in terms of returns. The Committee also felt that accepting the offer of Dr. A. Velumani may result in dilution of his focus and time, which is not in the interest of the Company .

In view of the above, the Audit Committee had recommended that it is not expedient to accept the offer of Dr. A. Velumani at this juncture.

BSE Notification: link

Key questions that crosses my mind in context of above development:

Call it hindsight wisdom or anything, Q4 concall was enough to suggest how it is going to unfold. Except one passing question, no analyst worth its name bothered to probe management on such an important strategical decision.

Tarun

True its such a waste of time

Dr. Velumuni offers to buy Nuclear -> External Agency decide worth -> External agency decide whether to buy or not -> At the end business stays with thyrocare i was happier in the first place if Dr. Velumuni haven’t put this offer on the table

May i suggest you to follow-up with Thyrocare’s customer care about this ?

So either they clarify the reason for such abnormal values that makes a customer worried or they acknowledge that its a error on their part.

From what i have read, they test their machines 4 times a day.

I am a doctor myself and believe me most doctors in Delhi NCR have absolutely no problem in reading reports from thyrocare. Actually more than the name of lab I would more interested in knowing if lab is NABL certified or not.Yes some doctors do have reservations about any labs including thyrocare which charge substantially less than the traditional ones. There is no material reason to believe that the reports from thyrocare or such labs is faulty except that it’s in the mindset of the people and some doctors who are obviously deprived of their share of commissions(As high as 50%/70% in some cases).I personally believe thyrocare is doing a great job in charging substantially less for reports. The success of preventing check ups is defeated if the cost of screening is too high. You do screening tests in larger populations to screen for hidden ailments which may not manifest in symptoms. 90% of patients with high lipids don’t have any symptoms and at your mother’s age I would be more surprised in finding normal lipids. So screening test at cheaper rates help in uncovering high lipids although Don’t produce symptoms but may still require treatment. Also most labs including drlalpath lab does at times produce wrong reports that’s the reason for the disclaimer beneath such reports that these reports are not to be used legally.