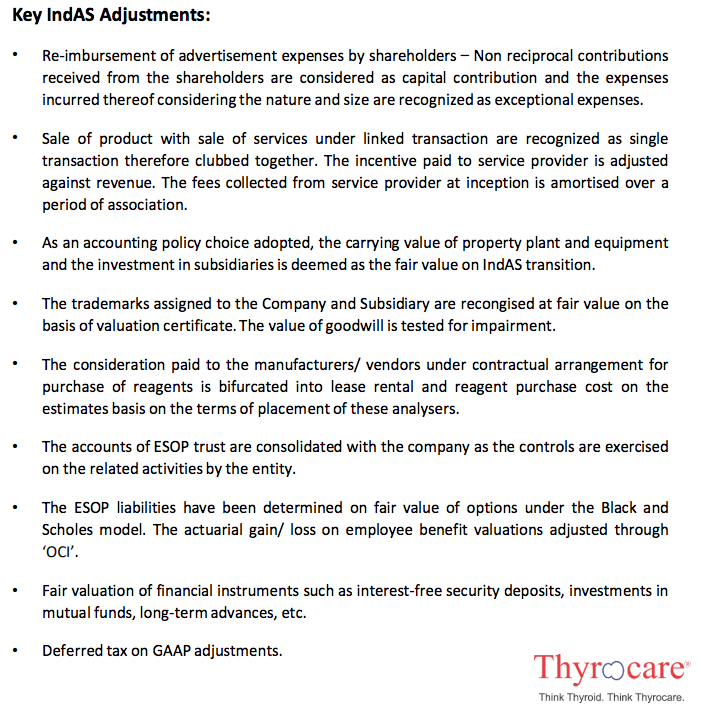

The key discrepancy I found was in the expenses. I can’t claim to understand the clarification provided but maybe the online promotional discounts provided were considered expenses earlier but are not considered so anymore? I remember Flipkart used to do something of that sort where they considered discounts as expenses and were paying less taxes in the process but the taxman sent notices asking them reclassify those promotional discounts as capex as it helps build their brand for the long-term. I suspect this is the key item in the discrepancy.

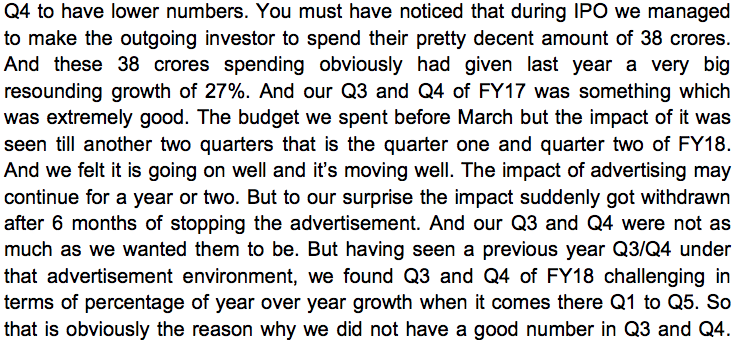

Looks like the ad spend was on almost every question during the concall. This is something I suspected - That the revenues would trail for 6 months or so after the ad spend.

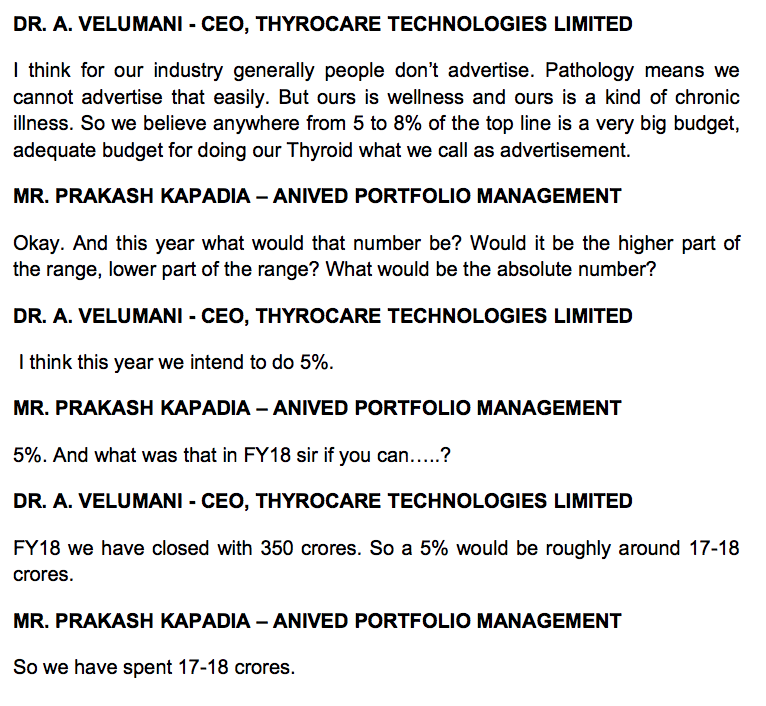

I am getting the uneasy feeling with the ad spend business. I think so far Velumani’s fixation on EBITDA margins has helped Thyrocare greatly. But past a point, you cannot grow and remain the biggest player without spending on branding even if it doesn’t reflect on numbers immediately. Let’s see if the 5% ad spends this year help with the 20% topline growth.

Is it only add spend or the commission passed on to the doctors also a part of it?Because the later part in any case has to continue as per the prevalent practice in india

Dr.Velumani in the Q4 FY18 concall mentioned that Thyrocare is again going to invest in radiology business (Nueclear). I was surprised because in the earlier concalls they had mentioned about going slow on this business.

Similarly, 2 other announcements which were concerning:

Committed to spending 5% of topline on ads (after saying each quarter that ads dont really drive the core pathology business growth)

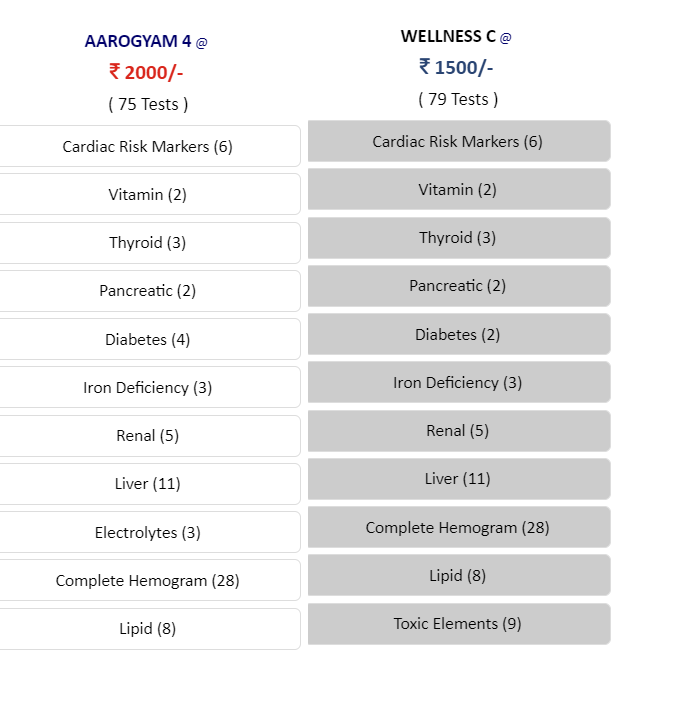

Price reduction in Arogyam wellness packages by 5% due to competition (if Thyrocare is the lowest priced player in the market as they keep claiming, dont see the need for this)

I was trying to book a package for my mother and see that there are two different packages available. 1. Aarogyam 2. Wellness. But I don’t see any difference in tests that they are carrying out in these packages. Also, I see there is big price difference in the packages even though most of the tests are one and the same. Somehow I am not feeling comfortable the way their website is being designed.

Sachit, The company is facing intensive price competition in the northern region, especially Delhi. Dr. Velumani spoke about in Q4 conference call. The article below might also be useful.

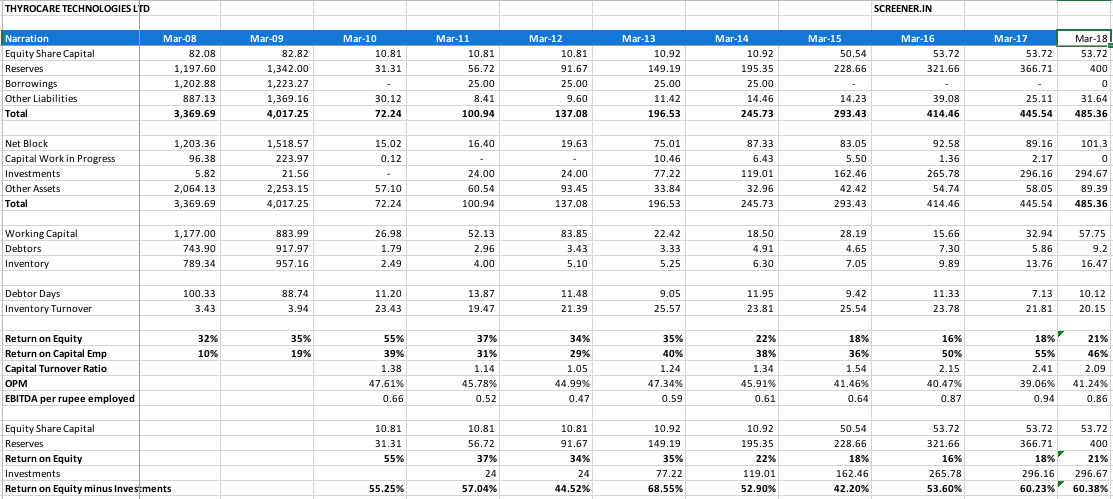

RoE minus investments at 60% levels just like FY17. EBITDA per rupee employed still at stellar levels of 86 paise. Not many businesses generate this sort of metrics (Page Inds at 78 paise) but the problem is demand side of the equation. I continue to believe this business needs to increase ad spends instead of holding onto cash and stellar metrics.

Hypochondria is a benign beast that rests within each one of us. A sustained TV ad campaign that raises awareness on Vit-D deficiency, Thyroid deficiency, Diabetes, fatty liver etc. could perhaps drive sales. Hypochondria is contagious but needs a nudge. While its impossible to drive sales to the diagnostic business (unless you are a anti-virus software maker that generates demand by writing malware), the preventive healthcare business I feel can generate demand - something like De Beers campaigns.

Investments/cash etc with thyrocare are substantial and they should be taken as part of the capital invested in the biz in my view. They are not doing anything with it as of now. In future they may but we have so many cos which if you minus cash investments etc all have stellar ROEs. Unless they return all that cash to investors its all part of capital invested with low returns at this point. At least if they give back investors will have a chance to deploy in other businesses - an opprtunity not available to them. Just my views

@bheeshma - Board is considering buyback. Looks like they heard us. However, I think the cash could be better employed in growing the business but I think buyback is not a bad move at all.

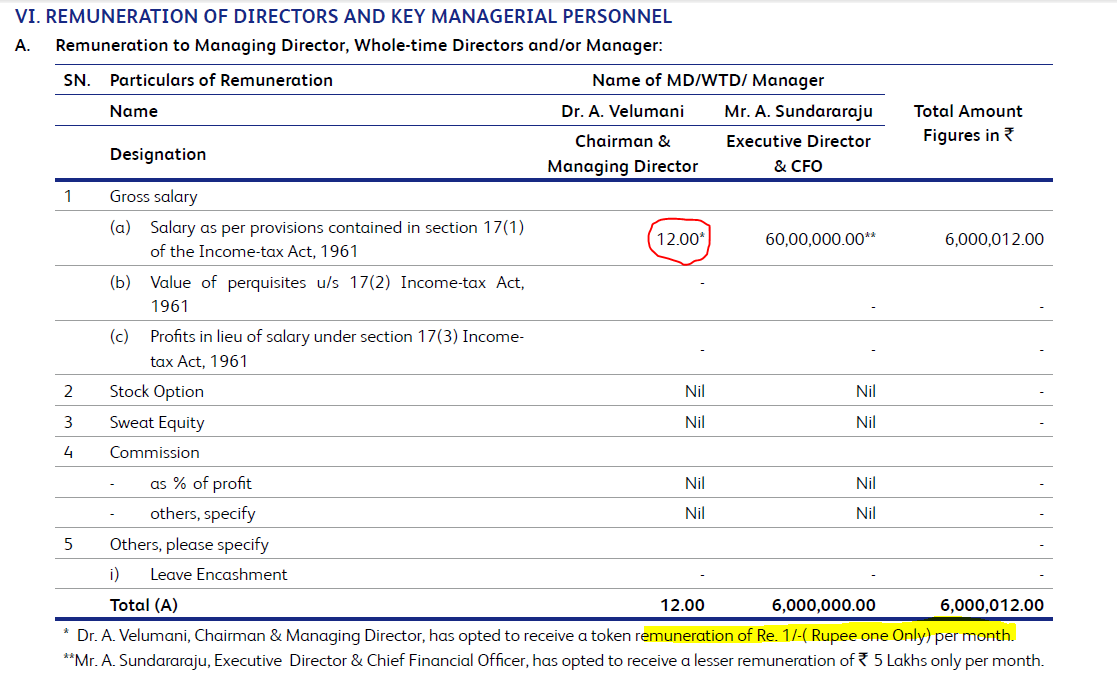

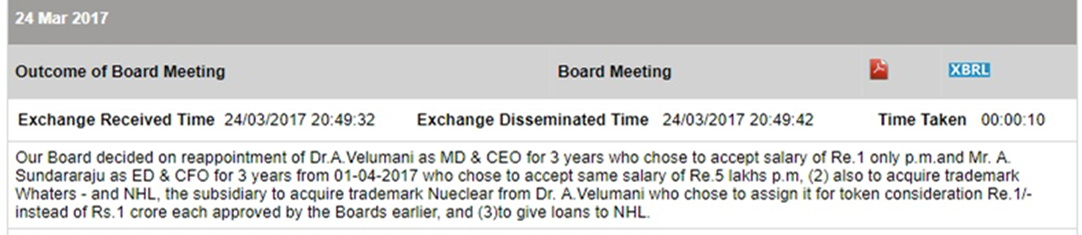

What a great gesture…Dr. A Velumani has taken only Rs 12 (Previous year as token 1.2 Cr) remuneration for the year 2017-2018. Hats off! (Good deeds do not go unnoticed :))

Its really great gesture…

As per the news company annunoced buyback at 730… Is’t it great news…At CMP of 630 promoters themself telling company is value 20% more the than at current levels… But why the market is not reaponding any positive

Am I missing anything here??

If any senior members through some light on the impact of the Buy back …on this shares and also in general Buy back implications and market reactions…

Not just the salary but Dr Velumani also gave away trademarks in his name to the company for token consideration of Rs. 1 despite board approval for Rs. 1 crore each.

On market buy back is good news indeed. Important to note that promoters are not participating and which means that their stake will increase! Also the minimum buy back is for 31 crores (approx).

Institutional stakes are already very high and many mutual funds got in at higher prices I think and they have been gradually decreasing their stakes since December 2017.