Hi Siddhant, I didn’t mean to say to buy over valued stocks. I meant to say that one should start looking at companies which are established in their space with little or no competition and also have a long runway ahead for growth. At a time when small companies are priced relatively much higher than these established companies it could serve better to shift some money from these small caps to the largecap established companies.

Agree, with your view. Sorry, I took it other way.

@hitesh2710 @Donald please let us know at present other than HDFC BANK and TCS, which are the bluechips that will stand up and compound in the years to come

I think you can look at nestle, asian paints, pidilite, britannia, bata, 3m, etc.

6 Likes

ITC tobacco has biggest wealth creator in US over 4 decades

@hitesh2710 Sir. Are these buys even at today’s prices? I mean not to load up but buy a little every month types? I keep waiting for some decent correction. How to approach buying such stocks to build a portfolio of only the blue chips sir.

1 Like

If you see near decent returns from a three year perspective then entering at corrections would be profitable… Else… you know the story.

1 Like

I am not sure if Indusind can be considered a blue chip company, but i work with the bank closely and feel they can be the a large wealth creator in the coming 5 years specially with their rural push.

Can some VP members share their thoughts on Infosys? It’s available for a reasonable PE right now

Regarding buying these bluest of blue chips, I think the prudent approach is to keep buying at regular intervals maybe for next 8-12 months. Historically most bear markets tend to get over within 12-18 months so that should be the time frame to be kept in mind while buying these kind of companies. And then what remains is of course sit on them.

7 Likes

Hi

@valuestudent trying to build my case of almost always being on the look out to buying the businesses in my Compounder portfolio. But buying more aggressively when chips are down. Also I don’t think it makes sense to hold a business for ever as businesses age and perish. I don’t want to be on the declining curve. Furthermore there are two aspects which often get mingled - Building a portfolio vs Showing returns on a portfolio. We need to appreciate that drawdowns are a natural outcome in this line therefore the waiting game to optimize purely on returns has an opportunity cost. Always staying on the sidelines and wishing that ‘as I jump in the returns will go skywards’ is a rare possibility. Better to be systematically ready for opportune moments with the Compounder portion of a portfolio. The optionality of liquidity is understated and at times when the market is getting mauled it helps to add aggressively in the compounders because that is the time to bet big.

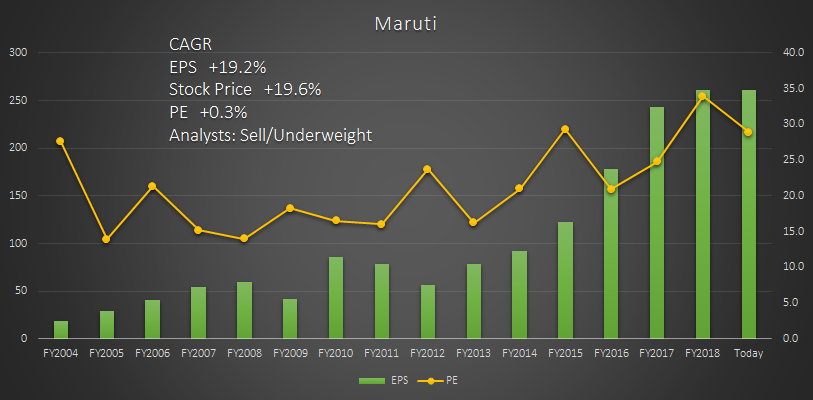

Lets take a bluechip for example Maruti if we consider it to be a bluechip for instance.

The median numbers since 2004

Maruti PE: 21

Maruti EPS Growth YoY: 33%

Today Maruti trades at 28-29 PE. To fall to its median PE of 21 we can either drop the price or raise the EPS. Skipping the math the output of a simulation basis historical data of price and eps will yield the possibilities. Now the worst fall Maruti has seen in its price FYoFY is -20% currently from the FY18 number its down 15%. In the last few weeks it was even down 25% in price. Now if we look at it from an EPS growth perspective. Half the times from 2004 to 2018 the EPS has grown as much as 37% which is the required number to touch the median PE of 21 without any further drop in price.

Therefore even if the market looks very high on an index PE level. Maruti as a bluechip compounder is fairly at median levels or perhaps even with a likelihood of recovering purely on this quantitative method. In this period if we thought we will buy when say index is below 20 PE then everytime barring once Maruti would underperform the index the next year.

Obviously its much much harder. The main point is the qualitative analysis which is the detrimental factor for the future. All this PE etc analysis is in hindsight. But yes if you have enough data points and believe in reversion to mean yes this quantitative flavor to our analysis does help us to buy systematically even when overall conditions look overvalued. Nifty’s CAGR in the same period is less than 13%.

For Maruti since 2004 if you were given an equal sum of money and told to invest in three ways:

Case 1: Buy every year

Case 2: Buy in those years when PE is below median level

Case 3: Buy every year but if in the year PE is below median level buy double the amount

If you do the numbers we realize returns is Case 2>Case 3>Case 1.

So while the Nifty PE looks on the right edge of the probability distribution curve Maruti on these terms was an aggressive add in mid October. Did we add more than we would have in a month is a question to ask.

I personally try to find buying opportunities in my Compounder portfolio always if the qualitative factors hold true ie I am convinced more than 50% that the business has runway for growth or a positive future pivot. And if this qualitative factor held true I would always be on the look out for a long add in the stock.

Regards

Deepak

8 Likes

Portfolio looks very good indeed.

1.Can you kindly share what screen/s did you use in screener. Unlikely that one screen can capture all names.

2.What is exactly meant by SIP candidate. Is it buying equal amount every month, quarter… Or its buying on dips

In addition, if invested at highs, he not only gets lesser returns* but also will have to face Drawdowns, and there is the rub. One’s conviction gets shaken when the loss is 50%. A less experienced investor stands the risk of being shaken out of his investment.

Several investors got shaken out of their positions in the recent Yes Bank crash. When we don’t understand the situation, we get fearful and herd mentality takes over.

*Comparing Maruti returns from 2008 highs and lows to currently. 22 vs 30% cagr.

Hi @deevee,

First, just a small note; I love these times when many of the top contributors are helping us with the thoughts behind investing and not only stock specific answers :). Stocks we will learn about with you talented guys and gals, but the emotional or logic side of the portfolio discussions make my heart glad. There is much wisdom that is to be imparted and we need a fair bit of that too to become better investors.

On your thoughtful post above; this is where I am trying to figure out one of the following;

Let’s say the FMCG index used to be around 18-22 and is now double that. So I am wondering about 2 conflicting ideas…

Thought A. The FMCG stocks (in general) will revert to mean. Currently, I have become open to buying a little bit, so I am thinking that, am I becoming like the frog in boiling water and losing my will power to wait? Is that what is happening as a collective to the buyers of blue chips?

It’s just a thought I am running with. Why would I be willing to buy something whose fair price should be half of what it is currently?

Thought B. The buyers are smarter and right. They understand that Inflation is low and will not (knowing our history) remain low. India’s average inflation is 7.7 percent or thereabouts and inflation is what will revert to mean. So then, these PE multiples or whatever way we want to use to judge pricing, will normalize with these stocks never correcting more than 20 odd percent during some mild corrections like October.

If I think that A is more possible then it is better to invest only the interest of Fixed Deposits as the return on portfolio will be zero in 5 years. No loss, but no returns. What you mentioned about opportunity costs basically from another lens.

If I think that B is more probable then buying the dips and sips; and adding slightly more during mild pessimistic bouts makes more sense. In these businesses we only need to get back inflation at normal levels (today the FD is attractive because the interest rate is higher than inflation) so I get some real returns in FD’s, this is an anomaly in our country’s history because FD is not supposed to beat inflation

I am wondering what from the above is real; A or B

So, I like what you and @hitesh2710 bhai mentioned “Almost always be a buyer, buy more aggressively when the chips are down and buy over a period of next 8-12 months”.

This line of thinking is making some sense because we cannot sit and predict the interest rates and inflation etc, but only take logical and rational actions that also hedge us against a bet on only one side of the equation.

With regards to the many other gems in your post, I think it is impossible to discuss them with you and learn in one post reply, so I will make a separate answer to touch on those nuances and thoughts on investing. They are an amazing line of thought. I do hope people read that post many times to understand the depth of ideas in it. I sure will.

Barring the sentence above, I am wondering if my thinking is seriously flawed on a and b. They seem most important for the bluest of blue chips. Getting the price approximately right, or getting the logic approximately right. Which one is truer, I don’t know.

3 Likes

It is justified to buy only those stocks from which you expect to get 15% CAGR in the next 3 years.

The Nifty PE range gives a perspective about the returns one will get in the near future, 5 years. If you buy high PE, returns will be less and v.v. However, over the very long term 10+ years it doesn’t matter. Provided, the market doesnt succeed in shaking you out of your position.

I, personally, would find it very hard to stay invested when the sky is falling, and my portfolio is 50% down. Which is a strong possibility from these levels.

India is a nascent market compared to the US, where in the early years vicious falls did happen each time the markets were over extended.

1 Like

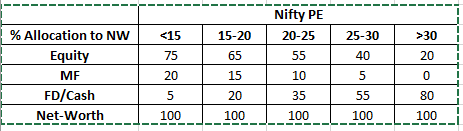

Nice analysis. I think we should be buyer, most of the time, but the intensity of buying and cash allocation should change depending on Nifty PE. Having said that buying of stocks should be majorly basis individual stock valuation and little to do with Index level. One can follow a broad level asset allocation model to always stay put in market. At individual stock level, buy on dips for quality names can be used, not indefinitely. once core portfolio is made- A stop loss/ trailing stop loss of 30% fall from high can be placed. As often 30% correction in a stock, that too after averaging down for a while, means something seriously wrong fundamentally. Exit and protect capital. So using some Index level indicators and stock level stop loss, we can always stay put in the market, play long and yet manage draw-downs effectively. Quitting the market completely and getting back is not worth, neither easy and will often miss the clustered gains. I have not done back testing or deeper analysis though.

Asset Allocation Model- Sample

Ulta Karo… When Nifty is high and gold is down, like right now, SIP in gold…

1 Like

ITC

Quality FMCG, Sticky Cigarette Business, Diversified and value pick

Avenue Supermart

Best Retail Play

Asian Paints

Undisputed paint leader, super brand

Britannia Inds

Brand, Value pick

Nestle India

MNC, Product strength, Long term sustainability

Titan Company

Best consumer discretionary, rising income play

Bata India

Best shoe company, rising income play, repeat usage

Colgate-Palm

Repeat usage, MNC brand, weakening competition

HDFC Bank

Best Pvt bank, leader by a big margin, PSU to Pvt value migration, Pvt bank competition weakening

Hind. Unilever

Most diversified FMCG, Population & rising income play, Top brand

Pidilite Inds.

Virtually monopoly, low ticket size but very useful product

5 Likes

Hi @deevee

Maruti has clearly done very well and its core business is top notch with excellent economics. However, all this excellence has piled up in the balance sheet which now has more financial than operating assets.

If this goes on for a few more years, technically Maruti will resemble a investment company with a quality passenger car business which contributes a lot of qty of cash every year for it to invest in financial assets. In my view, the valuations will thus trend towards its book value one would not pay more than a rupee for a rupee carried in the book

At the very least, one should be cautious about Maruti and wait for it to be available at far lower multiples even below its long term average so i am not too sure about the strategy of following a calibrated SIP plan.

Best

Bheeshma

4 Likes

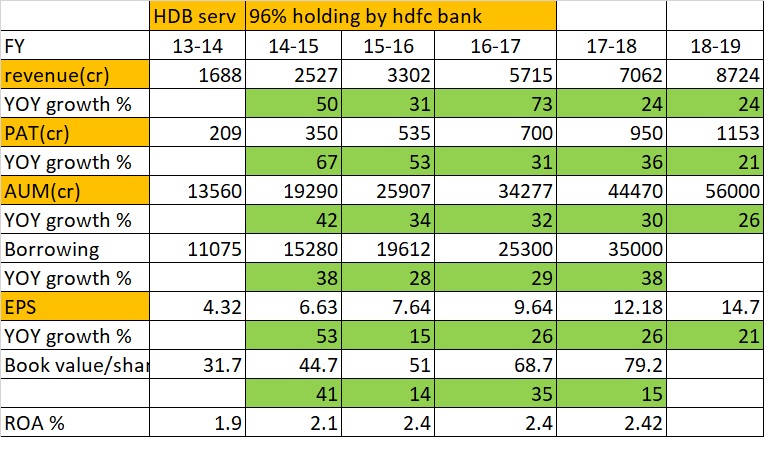

HDFC Bank: outstanding results once again

Update on subsidiaries

For FY19, HDFC Securities reported total income of Rs 782.1 crore, which was less than Rs 800.1 crore in FY18. Profit after tax for the year came in at Rs 329.8 crore. This was also lower than Rs 344.7 crore reported for the year-ago quarter. In the case of HDB Financial Services, NII grew 17.2 per cent to Rs 3,378.8 crore in FY19 from 2,882.2 crore in FY18. Profit after tax came in at Rs 1,153.2 crore, up 23.6 per cent over Rs 933in FY18

HDFC bank is the next HDFC bank IMO…next big wave of growth is going to come from the 96% subsidiary HDB services, the NBFC arm…in major electronics stores, I see them along with Bajaj Finance…revenue and PAT both growing 25 to 30% YOY…this can compete Bajaj finance neck to neck given HDFC groups pedigree.

Below are the financials I prepared for HDB from its Annual report

10 Likes

Let’s say you can get 1Lakh worth each of 10 stocks for free. Which 10 stocks would you pick & why? Which stocks do you think have a long lasting moat & solid growth?