This is the engineering division website

Scaffolding website with aait usa

http://scaffolding.technocraftgroup.com/

E commerce website

https://tdf.drdo.gov.in/project/development-dual-flow-jt-cooler

Can some seniors have a look at this what is the defence product awarded to technocraft industries lf any info pl share

1 Like

A recent interview by Mr Sharad saraf

Textile division restructuring is happening but demerger will take time

New capex 400 cr to add 500 cr topline in fy 24 and margin on conservative estimate at 20/25

Textile is still challenging alluminium form work is coming up new products in drum closure.

Let us wish a honest industrialist luck.

1 Like

I attended Technocraft AGM on Sep 27, 2023. Here are my notes -

Scaffolding

-

Prospects in US : We did about $48 mn of sales in US in CY22. US business continues to be quite strong and growing. In CY23, well on track to do around $65 mn. Next year CY24 should be able to increase it further to $80 mn. Have expanded distribution setup in US. Recently opened new distribution centre in Miami. Overall we have five different distribution location across the US. We are now the largest scaffolding distributer in US. Prospects are quite good.

-

Competitive Advantage : In scaffolding there is not much of product specialisation. It is more of a commodity product. Unlike drum closures there are 1000s of cos worldwide making scaffolding, primarily in China. Our competitive advantage in scaffolding is sales distribution. We cut across the entire distribution chain and keep stock in countries like US, Australia, NZ, Europe, etc and sell directly to the end user. The competitors in local distributors here get their products made in China whereas we have our own manufacturing facilities so we are able to provide better quality, better reliability and end-to-end service. Also able to command some premium pricing.

-

It is well known that steel is more expensive in India than China. We have disadvantage of 15-20% over China. Also the tariffs are gradually pulled away from US. Inspite of these we are able to sell our products at good margins because of our bandwidth, our distribution channel and also China+1 strategy that is going along in the US and other countries

-

Europe Sales : We are not well penetrated in Europe yet; it continues to be small market for us for now. We addressed this by hiring a very senior sales head in Europe in our Poland office from competition. We have little setback in Europe right now because of economic crisis there and market is right now quite dull. We expect this to improve. By end of this year, we will have certification in place for our scaffolding products in Europe. This will be a major breakthrough for us to increase our sales there. By next fiscal year FY24-25 we should see significant pickup in Europe sales and I think Europe market in FY24-25 and FY25-26 has the potential to be as large as the US market for us. So prospects are very good. Currently the Europe is only about $5-6 mn but it has prospects to be at least 10 times the present size based on we getting the certification which we will get by end of this year and market picking up.

Formwork

-

Formwork is far more specialised product than scaffolding. Formwork involves precision engineering, fabrication and site support. The kind of work we are doing in infrastructure in India is very high end Engineering. There is competition in formwork but part of the reason we are putting Aurangabad plant with backward integration of aluminium extrution is to put in place entry barrier. That by itself is quite a significant entry barrier. We will be first co (in India) to have our own aluminium extrusion plant with forward integration of aluminium formwork. Our specialisation is we cater to niche high end Engineering sector like infrastructure.

-

Capex and Timeline : 350 cr new capex in Aurangabad, primarily for formwork. Will be fully completed by end of next year 2024. Production will start by Feb ’24 in stages. The entire aluminium extrusion plant will be fully commissioned by end of 2024. We should see the full benefit of new plant in FY25-26 and we will see some benefit in FY24-25 as well.

-

Sustainable Margins : 15-20% in formwork business is doable in the segments we play. This will increase by 5% to about 20-25% once the Aurangabad aluminium extrusion plant is up and running, specifically for aluminium formwork business. Overall 20% is quite a sustainable margins for formwork business.

-

Export Plans : We do have export plans. Currently we do very limited formwork exports in Middle East. As we increase capacity in Aurangabad we plan to increase formwork exports. US is definitely going to be key market for us, so is South America.

-

Construction growth is strong in India. In India, we are primarily selling formwork, not scaffolding. And that is the reason why we are doing capex in the Aurangabad to increase the capacity to cater to increasing demand in India.

Scaffolding + Formwork

-

Sales breakup : In Fy23, export was 62% and domestic 38% of business segment sales

-

Export revenue breakup : North America 70%, Europe 13%, Australia + NZ around 8%, South America 3%, Middle East 1-2% and Asia 1-2%.

-

Raw Material : Steel is our main raw material for scaffolding. We buy hot rolled coil steel. We have our own ERW tube manufacturing capacity. So we roll the steel into tubes. We don’t sell tubes at all (used to sell long time back; have come out completely). All our tube product is 100% captive consumption, in making scaffolding. The other raw material is aluminium extrusion used for making formwork panel which we will soon in Aurangabad start making in-house as well, for that the raw material will be aluminium scrap.

-

Revenue from aluminium formwork in Fy23 was about 188 cr which is about 20% of Scaffoldings business segment reported revenue of 889 cr.

Textile

-

Investing in new mill in Amravati; capital outlay of ~150 cr. Govt incentive : Generous benefit in Amravati; co gets 25-30% capital subsidy. In process of complete shutdown of yarn mill in Murbad as it has high cost of operation (power, wages) causing bleeding in textile division. Will continue to be producing fabric in Murbad because have process house there and affluent treatment plant which cannot be shifted is also there. Out of the capex plan of 150 cr in Amravati, we have already spent 108 cr. We expect to start the production within couple of months. No immediate future plans of more capex in textile .

-

Demerger: No talk of demerger as of now. We keep getting proposals. The board will decide as and when appropriate time comes.

China Capacity for Drum Closures

- In China we have 18 mn sets capacity that is on one shift basis of 14 hr. China capacity is fully utilised as of now. China capacity can be expanded if we increase the shift hours. May expand as and when needed.

Defense

- It takes lot of time. So far we have total order worth 20-21 cr. In future defence may pickup at faster pace

Technosoft Engineering

- This business is doing very well. We are seeing strong growth in FY24. First qtr was not just the one-off qtr. We will see similar or better qtr going forward in each of the qtr this year. We expect FY24 to be very strong year. And going forward for FY25 the prospects for this business is quite strong in US, UK and in the European market. Post covid even the small and mid size manufacturing cos are very open to outsourcing large part of their Engineering work which earlier they were not. We are also expanding our sales staff in US, we got very senior VP of sales who has joined in US. We are expanding and are now entering into larger accounts. Overall the prospects are quite good.

Disc: Invested. No transactions in last 30 days.

29 Likes

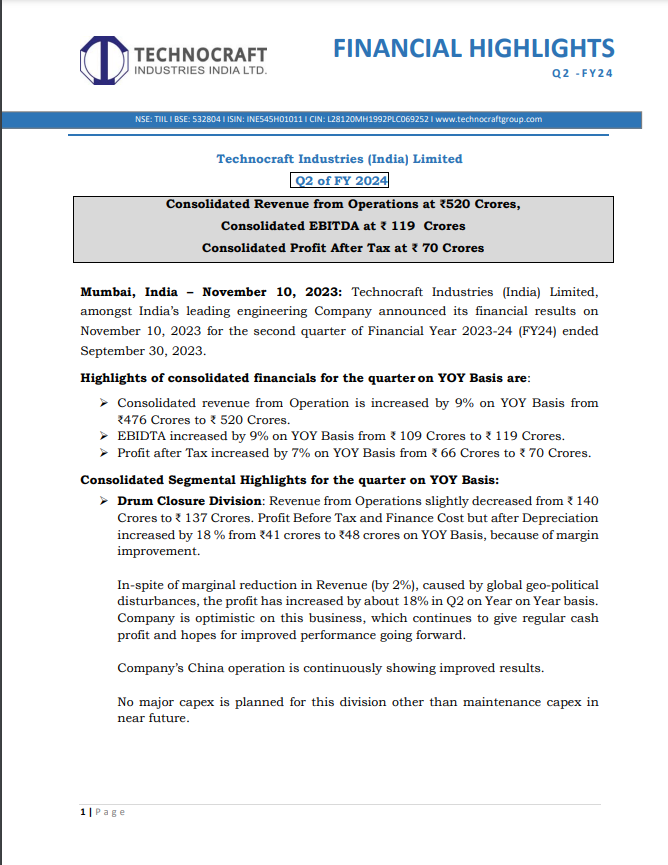

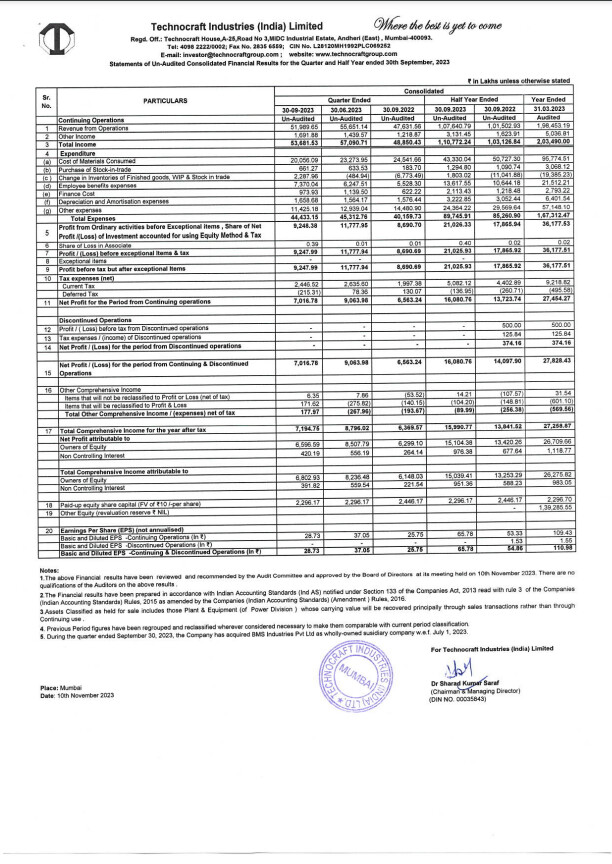

Technocraft Industries has reported its financial results for the second quarter of the fiscal year 2023-24 (FY24)

Financial Performance (Consolidated) for Q2 FY24:

- Revenue from Operations: The company achieved consolidated revenue of ₹520 Crores for Q2 FY24, representing a 9% year-on-year (YoY) increase from ₹476 Crores in the previous year.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): The consolidated EBITDA for the quarter reached ₹119 Crores, reflecting a 9% YoY growth from ₹109 Crores in the corresponding period of the previous year.

- Profit After Tax (PAT): The consolidated profit after tax stood at ₹70 Crores, indicating a 7% YoY increase from ₹66 Crores in Q2 FY23.

Segmental Highlights (Consolidated) for Q2 FY24:

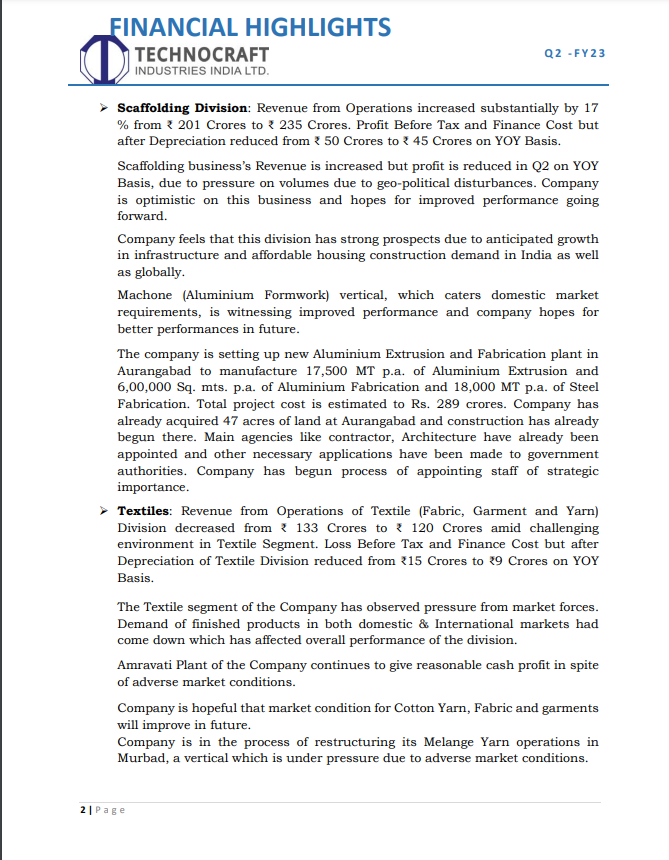

1. Drum Closure Division:

- Revenue from Operations: This division’s revenue slightly decreased from ₹140 Crores to ₹137 Crores in Q2 FY24, a 2% decline.

- Profit Before Tax and Finance Cost: However, the profit before tax and finance cost, but after depreciation, increased by 18% from ₹41 Crores to ₹48 Crores YoY due to margin improvement.

2. Scaffolding Division:

- Revenue from Operations: The Scaffolding Division experienced a substantial 17% YoY increase in revenue, rising from ₹201 Crores to ₹235 Crores.

- Profit Before Tax and Finance Cost: In contrast, profit before tax and finance cost, but after depreciation, decreased from ₹50 Crores to ₹45 Crores on a YoY basis.

3. Textiles:

- Revenue from Operations: The Textile Division reported a decrease in revenue from ₹133 Crores to ₹120 Crores, primarily due to challenging market conditions.

- Loss Before Tax and Finance Cost: The loss before tax and finance cost, but after depreciation, reduced from ₹15 Crores to ₹9 Crores YoY in the Textile Division.

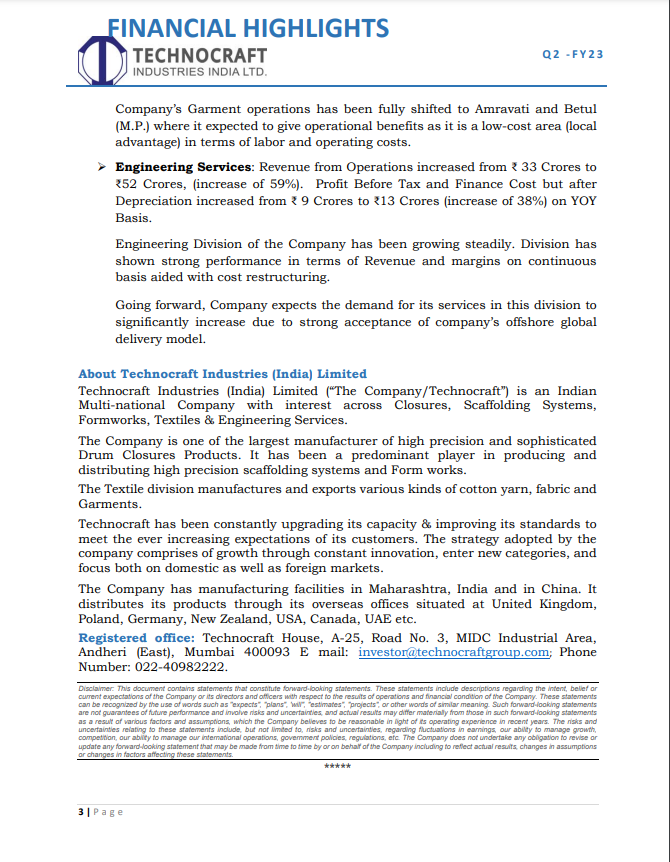

4. Engineering Services:

- Revenue from Operations: The Engineering Services Division saw a significant 59% YoY increase in revenue, rising from ₹33 Crores to ₹52 Crores.

- Profit Before Tax and Finance Cost: The profit before tax and finance cost, but after depreciation, increased by 38%, growing from ₹9 Crores to ₹13 Crores on a YoY basis.

Key Observations and Outlook:

- Technocraft Industries reported growth in consolidated revenue, EBITDA, and PAT in Q2 FY24 compared to the same period in the previous year.

- The Drum Closure Division saw a profit increase despite a marginal reduction in revenue, attributing the growth to margin improvement.

- The Scaffolding Division, while experiencing increased revenue, faced profit pressure due to geopolitical disturbances affecting volumes.

- The Textile Division witnessed revenue decline due to challenging market conditions, leading to lower profit.

- Engineering Services showed strong growth, with increased revenue and profit, driven by cost restructuring and a global delivery model.

- The company is optimistic about the growth potential in its various divisions and anticipates improved performance in the future.

- Technocraft Industries is actively focusing on expansion, as seen in the setup of a new Aluminium Extrusion and Fabrication plant, with a total project cost of ₹289 Crores.

- The company expects increasing demand for its services in the Engineering Division due to its offshore global delivery model.

10 Likes

Hi , where can I get technocraft industries agm recordings or agm minutes

The company will start the commercial production of aluminium fabrication which has even more realisation compared to Steel formwork/Scaffolding now

4 Likes