…we are comforted by commentary around pipeline being at the peak and conversations that it is having with both Telco and enterprise customers on 5G. In recent days,we have seen more activity in the US Telco space on a faster B2C 5G roll out after the launch of iPhone 12. From 5G being touted largely as a B2B play we think there is a shift to the B2C side, something that could accelerate Telco rollouts, globally. TSMC, the Taiwanese chip manufacturer raised its revenue guidance for 2020 recently partly on the back of increasing demand from 5G phone manufacturers.While it is early days, TML’s partnership with Rakuten on being the preferred systems integrator (and also likely key reseller) for Rakuten Communication Platform (RCP) could also be a game changer. RCP seems to be a likely global disrupter in the 5G equipment space against players like Ericsson, Nokia and Samsung. And in the absence of Huawei and ZTE from the market because of geopolitics, it has a fair shot at the opportunity. However, much of this would depend on the success of Rakuten as a 5G operator in Japan where it is a new entrant with disruptive pricing. … We believe that recovery in the Communications segment will be gradual (led by 5G) and Enterprise will drive growth.

Tech Mahindra has made multiple acquisitions during the year to strengthen existing lines of business. These include the acquisition of Eventus Solutions Group in April for $44 million as part of its business process services (BPS) business and a $120 million acquisition of cloud automation and DevOps services provider DigitalOnUs. In March Tech Mahindra bought 70% stake in Perigord to strengthen its healthcare BPS business.

Seeing not much activities here for long, and trying to bump this topic up looking at current valuations and the recent quarter performance.

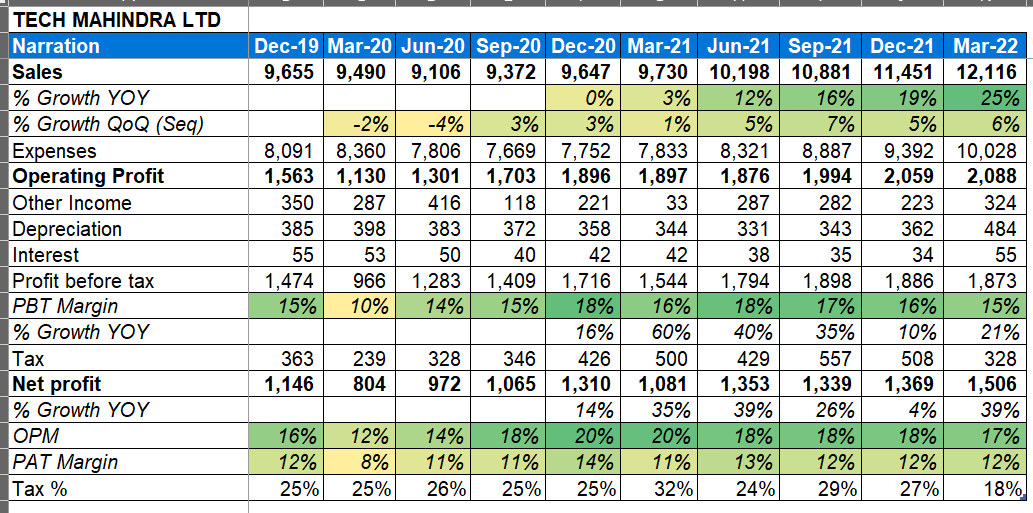

Margin is stable, except for the fall in current quarter. The following was the clarification by Rohit Anad (Glo.B.Head, Finance): From a margin perspective, let’s backtrack on what we said. I think we said that we will be closer to the vicinity of 15%. The main difference from us being there versus current 14.6% number is the amortization charge from an accounting perspective that we had to take on some of the M&A activity that happened in the last few months ending of the year. So, that caused a little bit of a headwind, which diluted the benchmark that we had outlined for ourselves. As we look forward for next year, I think good part is the actions that we’ve outlined for ourselves for giving us a positive momentum are starting to kick in. The structural action on ‘juniorization’ we have taken has already given us the headwind on the utilization being lower. Now, I think, that will start turning around.

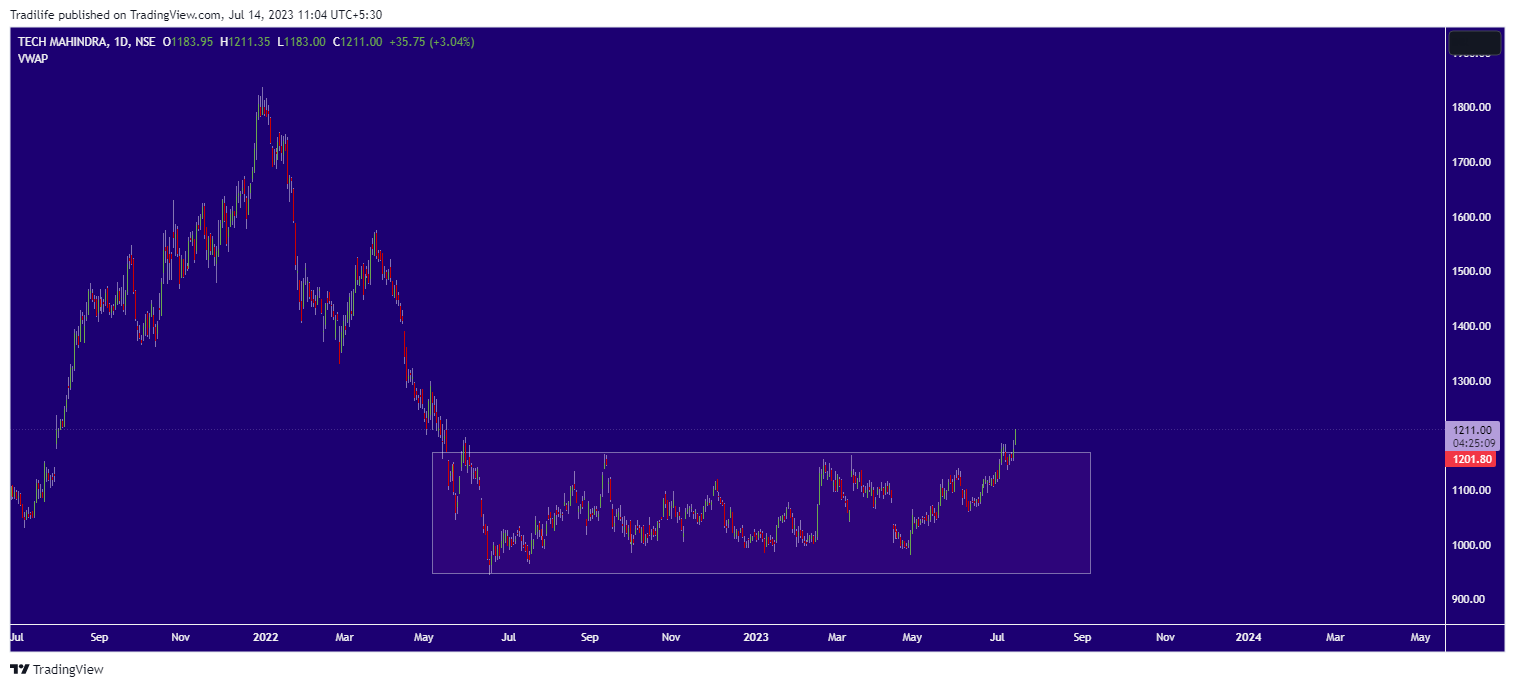

Weekly timeframe chart: It has traded very few times below RSI 40, and currently trying to sustain the support zone of 940-960. Another sell-off in market may drive it below that zone as well.

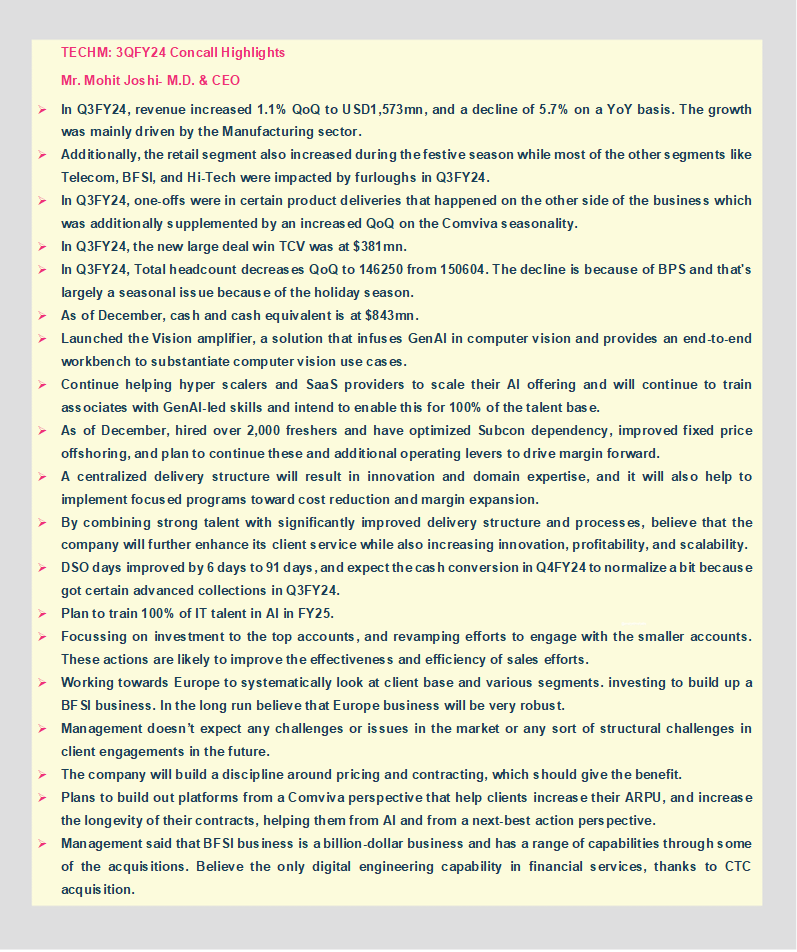

The following are few more comments/extracts, that found interesting from the Q4 concall held on May 13, 2022 and some snippets from the investor presentation.

Mr. CP Gurnani, M.D. & CEO: My focus for FY’23 and my management team’s focus is organic growth, continue to look in our EBITDA improvement programs, and continue our focus on wave-2 and Metaverse. Connectivity wave-2 and Metaverse will continue to be our focus leading to business transformation.

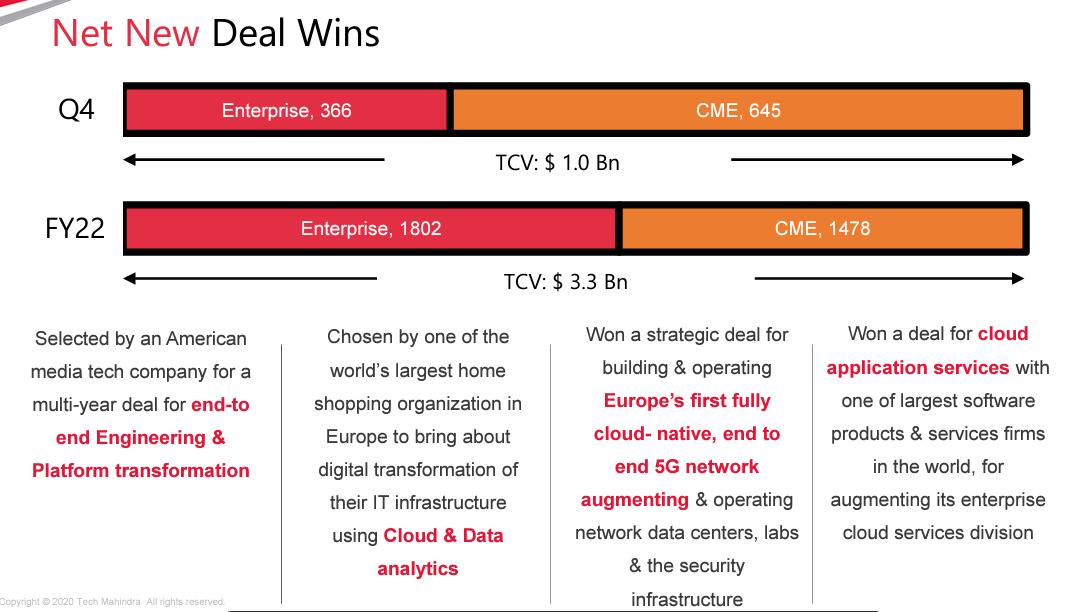

Manish Vyas, President CME Business: Overall trend as we have been saying through the last year, has continued to play out exactly, in that fashion, which is the digital transformation driven by 5G and the need to be ready for 5G revenue growth, whether in the consumer realm or in the enterprise, that continues to drive the transformational activity within the telecom ecosystem. What also continues to drive growth for us is the adoption of cloud.

Vivek Agarwal, President, Corporate Development: From a BFSI perspective we had a good deal with a 19% year-on-year growth and that obviously takes us on a certain trajectory as we look into next year. Q4, obviously, included the CTC acquisition. And as we explained in the last earnings call, with that acquisition, we’ve now created a standalone focus team to drive insurance growth and drive synergy with the new acquisition, and we’re making good progress there.

The utilization level seems to be fair considering the hiring numbers (10,000+ in FY22); though the attrition levels are concerning. Here is what Rohit had to say about it: In terms of freshers, we’ve added more than 10,000 last year and as I mentioned, one of the big levers that we will continue to drive is ‘juniorization’ and addressing the pyramid. So, I think that’s an area we will continue to pursue while we move forward into this year as well because it’s an important area for us to structurally address the cost structure.

Disclaimer: Invested recently, (around 2% of PF) and Trying to learn more on this sector and co., Post purely for discussion purposes only, Not a recommendation to buy/sell.

Hello,

Good to see some action in this thread, after recent correction from 1800 to below 1000. After trading between 700-800 for almost 5 years, stock price moved up mainly due to momentum in IT stocks and also due to some better revenue and Net profit growth post difficult period of 2014 to 2017.

As compared to its Large Cap peers, one should be cautious while doing valuation of Tech Mahindra. Though most of the growth in recent years is Organic, Management has a history of doing aggressive acquistions with focus on increase in revenue and which is not always margin positive.

Since its business model also involves low end application support and maintenance services, BPO there would be pressure on margins, as compared to its peers. This is the only large cap IT business trading below P/E of 18 which is better way to value IT services sector.

Though OPM has moved up from 15% to 18% during FY 20 to FY 22, due to various tail winds like digitization, 5G deals and pick up in BFSI segments, going forward OPM may revert to mean which has been close to 15% to 16%, and P/E of 18 should be looked at with caution.

It would be good to keep a watch on June 2022 quarterly results and see the margin trends.

This is relatively high risk business compared to most of the other large cap IT peers in India. One may look at similar low margin IT service businesses and consider lower P/E band while arriving at Fair Value, in my opinion.

Disc : No investment as of today, but on watch list due to reasonable valuations. Rupee depreciation may help sustain margins for some quarters.

IT services industry experience of over 25 years.

Tech Mahindra’s revenue from 5G services may touch $1 Billion in FY23.

Good brokerage report here

Struggling with Telecom/ Communication vertical. Revenue has gone down but expenses are Creeping up/staying elevated.

I like the New CEO. He comes across balanced. Aggressive but thoughtful. They are taking actions to reduce cost while investing in new capabilities.

I am invested and will stay invested burt valuation, in relative terms has gone up. Need to work out what is the right price to buy again.

I am looking for management’s plan on Apr 2024 but it does not look like there will be material change in short term. company may likely struggle for for more quarters or a year or so.

Any inputs?

For anyone looking for an overview of Tech Mahindra:

Was the past year the worst possible year. Decreased Margins, Sales decreases, I think one of the only big consulting company to report yoy decrease of sales. Profits are evaporated 51% decrease YOY. Is this extremely overvalued?

https://www.bseindia.com/xml-data/corpfiling/AttachLive/50792df3-fab1-40b9-a1ab-77f9bfd20aed.pdf

Tech Mahindra is very different from their peers in terms of their revenue model. Their business is heavily concentrated in telecommunication sector which has seen a slowdown in spending in western market, (mainly in the US which has been most impacted). But the same cyclicality and concentration creates tremendous opportunity for the stock as what goes down must come up. So when spending in their main customer segment picks up, the recovery in stock prices could be swift.

In terms of valuations, it’s still the most undervalued stock among its peers with market cap at twice the sale (as opposed to 3-4x for the peers). P/E looks high because of drop in profits. Once they go back to the lower end of their historical average operating margins (18-20%), P/E should drop to 18-20 levels even on a modest top line growth.