Can we compile the list of all relevant questions (apart from what I mentioned in the above post) which others have and then can narrow down by deliberating answering those questions, which our member know.

Once we finalize the list of pertinent questions, then we can ask them with the management.

I am not sure how to reach out to this company’s management team, since I guess they don’t have quarterly earnings call??

Even though I like the business, I never invested in the business because I was not comfortable with the valuation when I first discovered the business about 2-3 years ago.

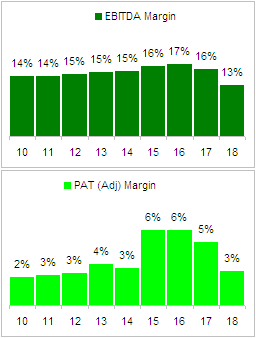

Between 2014 and 2016, EBITDA margins remained flat at around 16-17%, net margin almost doubled from 3% to 6% and stock price followed.

Source: Capitaline

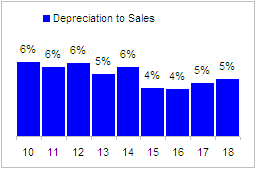

Most of the change in net margin was simply because of change in depreciation

Source: Capitaline

which has reversed over last 2 years causing net margins to decline. I was actually surprised to see EBITDA margins decline so that’s an additional risk. I think market price does not fully reflect the risks so will stay away for some time.

Most important metrics to focus for this company is cash flows, as due to nature of converter business it would remain depreciation heavy. For the first time in recent years, Capital WIP has moved higher while reducing long term debt (FY18 end), which signals something very positive.

Overall the RM pricing in paperboard remains a cause of concern and might need a few more quarters to stabilize.

Correct me if I am wrong. The concerning part is that the OPM has been declining for last 5 quarters including this quarter too added to what you have said ie revenues have fallen this Q2 over Q1.

FCF has been negative in all years except 3 in the decade.

Q1 results is a mixed bag. Sales is holding up but there is a sharp drop in gross profits (y-o-y). Looks like gross margins will remain at 40% going by trend over last 4 quarters. 60% PAT growth is due to low base which in turn was due to impact of GST last year. On absolute basis, net margins of 3% is low.

I agree with @deevee about free cashflow or lack of it. Company is generating healthy operating cashflow but reinvesting all of it plus some more in assets so it has to borrow money every year to keep up with the capex. Trouble is, with all these heavy capex, we should expect sales growth of at least 30% which is not coming in. Sales growth over the last 5 years has averaged 15% which should be self-funded without any additional borrowing. Debt should have gone down instead of going up.

Such companies should be valued at close to book value (or lower) given their heavy debt load and low margins. I will value the company at 250-300 Cr compared to current market cap of 450 cr. Prior to 2015, this company was valued at book value.

From Q2 results there are signs that this is finally turning the corner after a bad set of results over 5-6 Q’s.

What was most likely happening over the past few Q’s -

Their timing of flexible packaging plant was bad, they commissioned the plant and got hit with DeMo. At the same time their packaging board business started seeing higher input costs which they were not able to pass on to customers who were themselves coping with reduced demand. This was followed up by GST related issues in a couple of Q’s

In the meanwhile overheads for the flexible packaging coupled with depreciation ensure that they were EBITDA negative on this since the volumes weren’t taking off. Hence EBITDA tanked from a level of 16%+ to 11% at the lowest point. Logically they must have been positive at gross margin level (management has indicated that flexible line with operate at an OPM of 10-12%), hence it was a question of enough volumes kicking in so that the line turns EBITDA positive. Looks like this has started happening from this Q2 onward. Else paper prices continue to be high and I do not see how the paperboard packaging line could have reverted to the EBITDA of almost 17% that one saw in 2016.

For Q2, top line is 210 Cr at an EBITDA margin of 14.5% and PAT of 11 Cr

Company is sitting on net block of 390 Cr inclusive of WIP, D/E at approx 1.2

Currently trading at 370 Cr (less than net asset value)

Operating cash flow continues to be healthy, their working capital terms will not change too much since the buyers are FMCG companies where terms are more or less standardized

I don’t think this will ever be a low debt company since reinvestment into fixed assets will always be needed to keep the growth engine going.

One more Q of decent results and this should look interesting. Let’s see how the market reacts to this next week

Disclosure: This is one of my larger holdings and has tested my patience a bit over the past 2 years

TCPL has launched it’s second line this year. As planned, it is on track to install it’s third line later this year. In an economic downturn, results have also been good. Sales up 15% YoY, Net Profit 8% YoY and ebitda up 17% YoY.

Interesting piece of news. Warburg to buy Parksons for ~2200 cr. Parksons is TCPLs largest competitor in paperboard packaging. Based on ROC data, Parksons did an EBITDA of ~130 cr last year. Return ratios and margins also similar to TCPL. So Warburg was effectively happy to pay 17x 2020 EBITDA for Parksons. Even if we were to value TCPL even at 10x, potential upside from here is massive.

Any idea why Parksons being valued at such a premium to TCPL? Is there anything Im missing here, numbers and growth profile for both companies look very similar.

Parksons and TCPL though are very similar in their quality and cliental, even setup wise, both have similar capabilities but parksons has some niche cliental and are an integral supplier to many top brands. TCPL revenue is around 50% of parkson’s. Parkson is a bigger brand in short.

Last 2 Q had worst commodity inflation. Inflation flattening out now. Margins improved. Partly led by higher operating leverage : capacity utilization. RM being passed on to customers.

July-Sep is highest volume Q. Q1 is normally weakest Q.

Competition is entirely in private sector.

Mobile: Very low revenue currently. We can quadruple our revenue in mobile packaging revenue. Very big growth opportunity here.

EBITDA for carton is higher margin. Flexible EBITDA can improve. ASset turnover is much higher in flexible. Carton biz is more mature.

Innofilm capacity is only 1% of total capacity. Line can get booked out easily. There is a huge scope.

No greenfield needed for carton. Even for flexible not too challenging to add capacities.

Innofilm is technologically challenging material. Backward integration. Will look to sell film for exports. TCPL would be a customer for innofilm. WIll sell in market as well.

Looking at 3 digit revenue over next few years for rigid packaging.

Exports has grown at 25% CAGR for last 3-4 years. 25% of business now.

Big silver lining for us. Another sub in middle east. Marketing office there. Middle east & africa.

Western world is looking at opportunities beyond china. We are nowhere near there. Havent gotten benefit of china+1 yet. Potential is there. Both carton & flexible.

New customers being added, more biz from existing customers.

Focus on india as a geography.

Consolidation will happen. But slowly.

Dont need to do more capex to inc rigid film revenue.

My overall thoughts: base carton packaging biz should grow 12-15% on the account of some volume growth, some market share gains & some premiumization.

The real volume growth here will come from the

flexible packaging biz, the rigid packaging biz, the mobile industry, the recyclable plastic packaging demand. Should be possible for co to achieve 17-18% topline growth if they execute well…this is specially since they are into both paper & plastic packaging which makes them somewhat unique as a supply chain partner for their clients. The operating leverage, economies of scale in the new divisions, higher value added product mix should drive margins growth. What has been quite heartening to see is that at time of highest rm inflation in many decades co has been able to pass on the price increases to its clients. What has to be figured out is the client switching costs, the barriers to entry, the reason why clients prefer tcpl why tcpl is gaining market share. Export remains a big dark house. If they can replicate their 25% growth cagr in exports on this larger base of 25% it could become even more material part of revenue stream.

Lesson from this - sometimes you are just early, not necessarily wrong. 20% CAGR in spite of looking like an idiot for a period of 5 whole years. No P/E rerating in this counter yet, multiple is still in the same range, all gains are due to earnings growth

Patience does pay off, provided you are patient with the right businesses

Disclaimer: High risk, low liquidity legacy bet from 2016. Not part of the external capital I manage. Not an investment recommendation

TCPL Innofilms – a 100 % subsidiary - was tipped to be the “world’s first state of the art, innovative PE blown film line at our facility”. It manufactures recyclable flexible packaging and the management had said it is one of a kind and amongst the very few companies in India to be equipped with such capability. However, the foray seems to have run into rough weather. The company commenced trial production in Q4FY22 and commercial production in July last year. But the business has made a loss for the year. More importantly, the management said it is still facing some technical snags in the operation and will struggle for another couple of months. The decision to merge the business with the parent indicates a clear scaling down of expectations. Earlier, the management had said it was made into a separate company and a separate profit centre as they wanted to track its performance independent of TCPL. Not any longer.

Creative Offset (COPPL) was acquired in December ’21 and the current stake of TCPL in it is 89 %. The company specializes in manufacturing of printed rigid boxes and leaflets for the mobile phone and consumer electronics industry. In Q4 FY22 concall the management said we should be able to turnaround the company in a few months as benefit of scale, cost optimization measures, and other synergies start contributing to the performance. In last four months of FY22, the company earned Rs.9 crore and now for full year FY23, it has earned revenues of Rs.32 crore. But posted a loss. I think making this business profitable is going to be a challenge – it is neither capital intensive nor technology intensive, so one can expect supply will always be plentiful. Even though demand will grow, cutting profitable deals with manufacturers will not be easy. And this runs the risk of bringing down company level margins, which the market will not like.

The core business however remains stable – steady growth and steady margins. Here too, long term growth has come about only by taking on additional debt, so it is not exactly a cash churner. At around 14-15 times earnings (adjusted for exceptional items), stock seems fairly valued.

profit after tax jumped to 100+ cr which was in the range of 30 to 4o from years , what changed significantly in FY2023 that the profit jumped 2x ? and is it sustainable ? if anyone has deep dived in this business can comment on this …