Could anyone help me understand total number of shares?

As per annual report it is 3,395,850,719 and as per screener.in it is 679 crores!

And what are total number of DVR shares? And why it is not mentioned in annual report?

Thanks in advance.

Total number of shares are 3395850719 with a face value of Rs. 2 each. Total value of these shares is 679 cr when you multiply total number of shares with face value.

3395850719 * 2 = 679 Cr.

2 Likes

Tata Motors investing today is leap of faith like VC investing. I have mentioned it earlier in the thread too.

I got interested and invested in Tata Motors after reading on iPace and their massive EV program to leapfrog Mercedes, Audi and BMW.

So, risks are higher but it will not become a bottomless pit as there is an cash generating operating biz.

I also hope that EV investment will be supported based on valuations for Tesla.

So, I find enough margin of safety if I look at from sum of parts (Current operating biz + EV biz) perspective.

Let us see how it unfolds. Wait can be long like Biocon where nothing happened for 8 years and valuation wentup 5 times in 8 months.

4 Likes

In the attached video, Aswath ji has explained why a traditional auto company (serving developed market) is a bad investment.

All respect to prof. But let us not forget GM is in top 20 holding of Buffet.

Traditional auto makes money in India, semi-luxury and luxury auto makes money globally. That is what Tata Motor represents.

It is capital intensive biz, no doubt and has typical pitfalls.

It also depends on your portfolio. If you have 80% into cyclical biz in PF, adding TAMO adds risk to your PF. But if you are 80% in FMCG, adding TAMO may help.

1 Like

Tata motors revenue is JLR. They don’t sell many in India yet.

Domestic is loss making as we speak and it has not turned around yet.

If Auto companies do not make money. I wonder why maruti has become a multibagger.

2 Likes

Interesting debate so would like to add to views

Tata Motors as mentioned earlier - New Opportunity - Software becomes more important than hardware … Now strangely Tata motors is probably only auto company whose Chairman understands Software more than others and I see that as Big Plus

Secondly in this disruption – > JLR has very low Mks in cars and it has much less to lose and lot much to gain when it comes to shift from IC to electric vis a vis GM , Toyota and others . Hence it is one first one to built a competitor to Tesla -

Also In a sense JLR is not traditional auto company as it does not make mass market cars … It is like Apple vs Dell … They make beautiful cars and have been more brand driven rather than scale driven …

Betting so big in JLR at this juncture is BIG GAMBLE more like VC investing . Will it work I don’t know , but if it does and even if JLR doubles its Mks like say to 5% global car sales – That will be BIG profit earner of all times …

So Tata motors should be looked at as Long Term call option and not as stock …

1 Like

Read that again. Maruti does not sell cars in developed market. India is still growing and auto industry has not become a cyclical industry like developed markets. The discussion is not applicable for Indian auto makers.

1 Like

Likewise. In fact I firmly believe that I pace is the only real variable in the TaMo equation. On positive, there is not a single review that I read that was bad. Early booking reports seems great in California where 50% of their global salsa are likely to come from. And price is great. On risks - rave reviews is not same as early success and early success is not same as blockbuster product (remember Nano and indica).

Please read above and check last few months of sales data. Commercial as well as passenger are well on their to recoup lost market shares.

Until it reflects in the p&l statements, it has no meaning. We can keep high cost of platform development on one side and marginal sales on other side and they will not balance each other. Let them start making sustainable profits. Then we can applaud them.

1 Like

The results for Q1 will be very useful as Tata motors will reveal segment wise data for PV and CV for the first time ever. We can see where the cash burn is.

1 Like

When v r in red, did v really needed this?

Very critical to invest in fleet startups to influence future sale of their brands.

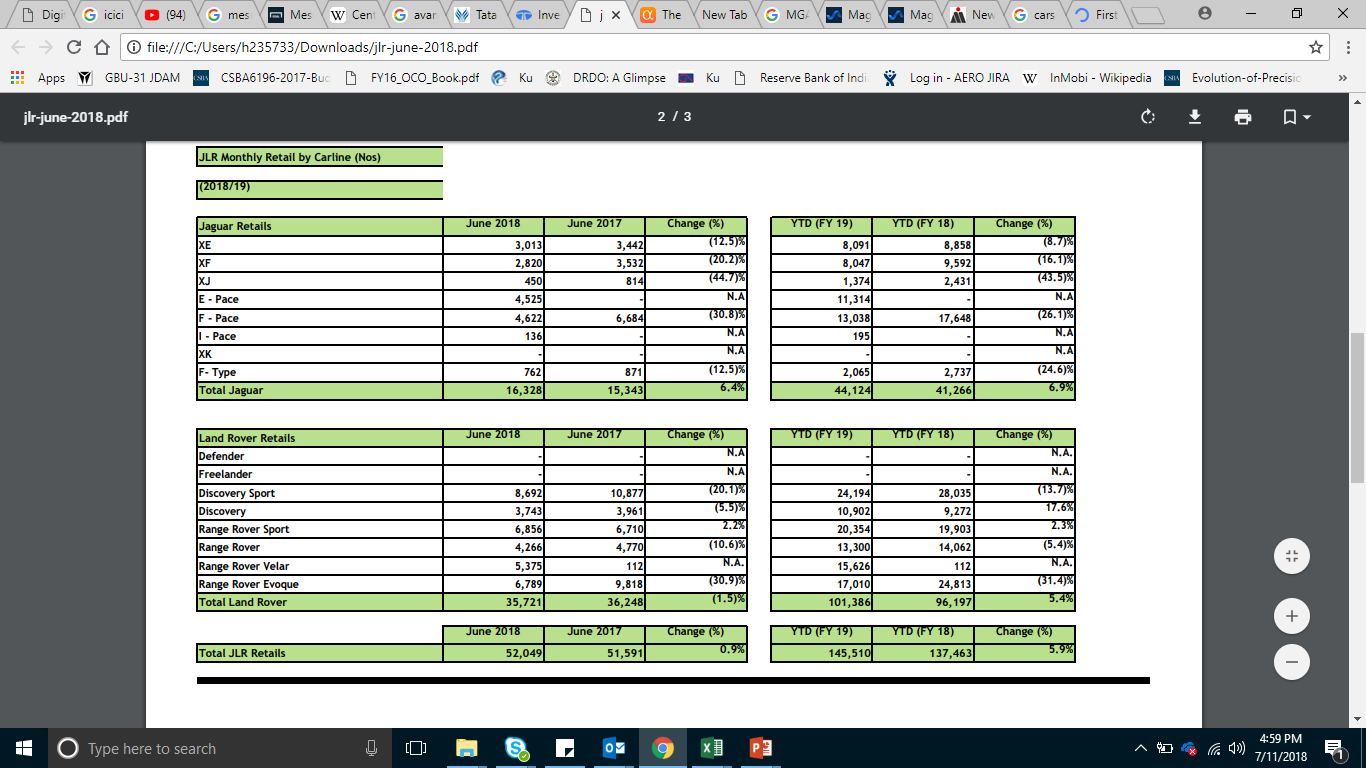

As some of our esteemed members have pointed that I-pace is a key variable in the overall Tata motors story. Has anyone looked at why ipace sales are so low even after 2 - 3 months of launch.

Ipace is manufactured by Magna (a contract manufacturer) from Graz Austria. Epace and Mercedes G-Class is also manufactured. Maximum capacity of the Graz plant is 200000 units.

If we go by the youtube videos, we get the feeling that i-pace is an awesome product. There should be significant orders.

Are the orders very low for i-pace or is there any production issue with I-Pace?

The first i-pace vehicle got delivered on June 6th. I guess the production is slowly being ramped up. We should see good numbers over the next 2-3 months.

https://insideevs.com/tennis-champ-andy-murray-takes-delivery-of-jaguar-i-pace/

1 Like

I don’t think receivables could be a big issue in this case, because ultimately they have to collect it from dealers only and not the consumer. Sooner or later they are going to receive it , and if its TATA we can trust them that they will not show fake sales which leads to increasing account receivables. I think collecting money from dealers should not be a big deal. Dealers wont run away overnight. Its not easy to open a dealership overnight, In short term it may affect cash flows but receivables should not be a problem here,

1 Like