Thank you Aman. I could see in the article, “The company derived around 60 per cent of its revenues from the automotive sector in FY19. JLR (Jaguar Land Rover) is its biggest customer, contributing around 21 per cent to its total revenue during the same period.”

update:

Con call is scheduled on 18th July

Dial-in Numbers

Universal +91 22 6280 1194 +91 22 7115 8095

India +91-7045671221

International Toll Free Hong Kong 800964448 Singapore 8001012045 UK 08081011573 USA 18667462133

If anybody from Bangalore has attended the company’s AGM today, please do share the managements commentary during the AGM.

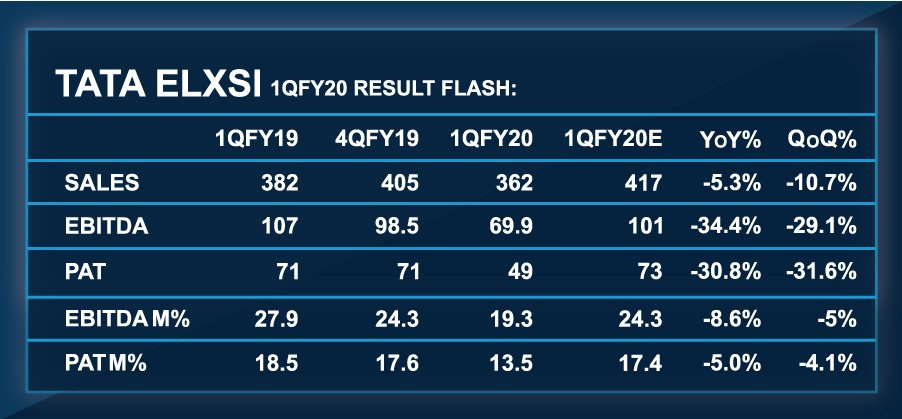

Horrendous results for a company planning to grow the top line 10% Q-o-Q. I think they should have mentioned this could be in either direction

Looking forward to the management con-call to see what has led to such a poor quarter!

Disc: Invested. 3rd largest holding.

Numbers are shocking. Moreover depressing considering company profile and management commentary.

Waiting for mngmnt explanation on such poor result. Please someone share if attended the AGM today.

Disc : Invested but not in top holding list.

Only thing would like to ask is Can we merge wit TCS . TCS has doubled in last 3 years and TElxsi has lost 30 t0 40%.

Hi,

Avendus has sold around 357,590 shares through a bulk deal yesterday

Has anyone attended the AGM?What was the reason provided such a steep downfall in revenue and profits?

Thanks,

Deb

Con Call Link (source Researchbytes):

Automobile Slowdown Effect

Loss of revenue from automobile companies (JLR & non-JLR, mainly JLR). It’s not that the r&d budgets were cut, or they were shifted to Elxsi’s competitors, but there were significant delays in decision making from these automobile companies.

Revenue contrinution from total JLR Business came down from 22% last quarter to 14-15%. Revenue contrinution from total transport business is down from 60% to 50-51%.

Substantial amount of IP & one-off revenues in previous quarter were not repeated, because of the general slow-down & the pace of decision making. IP revenues came down from 3.5-5.5% to 1% QoQ. One off revenues associated with engagements came down from 25-30 Cr to 2 Cr. One off revenues come from new engagements & in this quarter there were not many new starts in auto business.

Currency impact 2% overall.

EBITDA Margin declined because of revenue loss while expenses remained same.

Salary hike will happen in Q2 FY20.

Nevertheless, the Pipeline is bigger than before (mostly in Autos). There are a number of active cases for the IPs & other new engagements, which they hope to close for revenue.

Broadcast & Communication and Medical Business unit both clocked very high growth, higher than they have grown in two previous quarters. Broadcast & Communication clocked 10% growth from previous quarter, while Medical Business unit clocked 35-40% growth (revenue contribution < 10%) from previous quarter. However, these segments are not big enough to compensate for loss in revenue from Auto segment.

Got into a new country in Europe.

They are evaluating other completely new verticals. May enter after 3-4 quarters.

Disc: This is my first Con Call note. Sorry if there are any mistakes. I am invested in it.

Transcript of the entire con-call can be accessed here:

https://finance.yahoo.com/news/edited-transcript-tataelxsi-nse-earnings-190701463.html

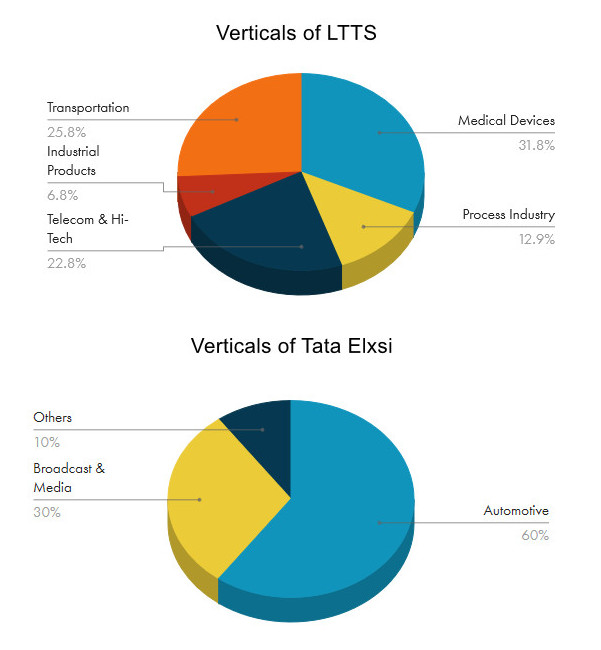

So far LTTS is stealing the show. TElxsi scoring week on marketing and risk taking ability. The agression in business seems to be placid and that is showing in valuation by market.

IMHO, the relative better performance of LTTS is because of its lesser dependence on Automotive sector. They are simply more diversified (see the breakup below).

Tata Elxsi achieved huge growth (~40%) in Medical Devices segment in this quarter but the revenue contribution from this quarter is <10%. LTTS has ~32% revenue contribution from Medical devices.

Disc: Invested in both. The graphs were copied from Tijori Finance.

True but on patent front and aquisition as well. LTTS is looking like a business run by promoter TELXSI is giving a feeling of a government run slow and sleepy. We are there in the race but not to win.

In my opinion, they must use this as an opportunity to build other non-auto verticals. However, they are continuing to say that JLR and other auto accounts will provide future growth. At the moment, not sure what to make of it…

Ltts transportation segment grew 20%. Cmp it is a hold but management is not proactively navigating through companies bad phase in the best growing futuristic business.

In this, N. Chandra says merger with TCS “is not a priority”.

Manoj Raghavan - the incoming CEO buys 2,000 shares from the open market:

Q2 FY20 Results

- Total Income reduced 6.5% YoY, grew 6.5% QoQ.

- Net Profit fell 39.3%, grew 2% QoQ.