I had a question to ask of you since it seems like you have done extensive research on Tasty Bites. What is the nature of agreement between Mars and Tasty Bites? Like does TB sells to Mars and then Mars uses its distribution channels to sell the product to the market at a markup?

2 Likes

Due to ongoing racial protests in the US there have been some change being taken by food brands whose branding is based on ‘racial steroetype’.

Like Aunt Jemima brand of pancake mix, syrup, and other breakfast foods owned by Quaker Oats subsidiary of PepsiCo. https://www.bbc.com/news/world-us-canada-53083664

Similarly, Uncle Ben, brand owned by Mars will have its own changes. https://www.whio.com/news/trending/uncle-bens-change-logos-following-aunt-jemima-decision/WAWJRZSGKZARZEULXC6YUEZXI4/#:~:text=The%20name%20was%20changed%20from,make%20progress%20forward%20racial%20equality.”

Nothing that directly impacts Tasty Bites, but its good to be aware of changes happening in the food industry in the US.

Disc: not invested

3 Likes

I was just looking at the stock on screener and I noticed something - why is there constant up and down movement of the stock price? You can see the stock price keeps rising and falling considerably continously. Is there any particular reason for the same?

@spatel

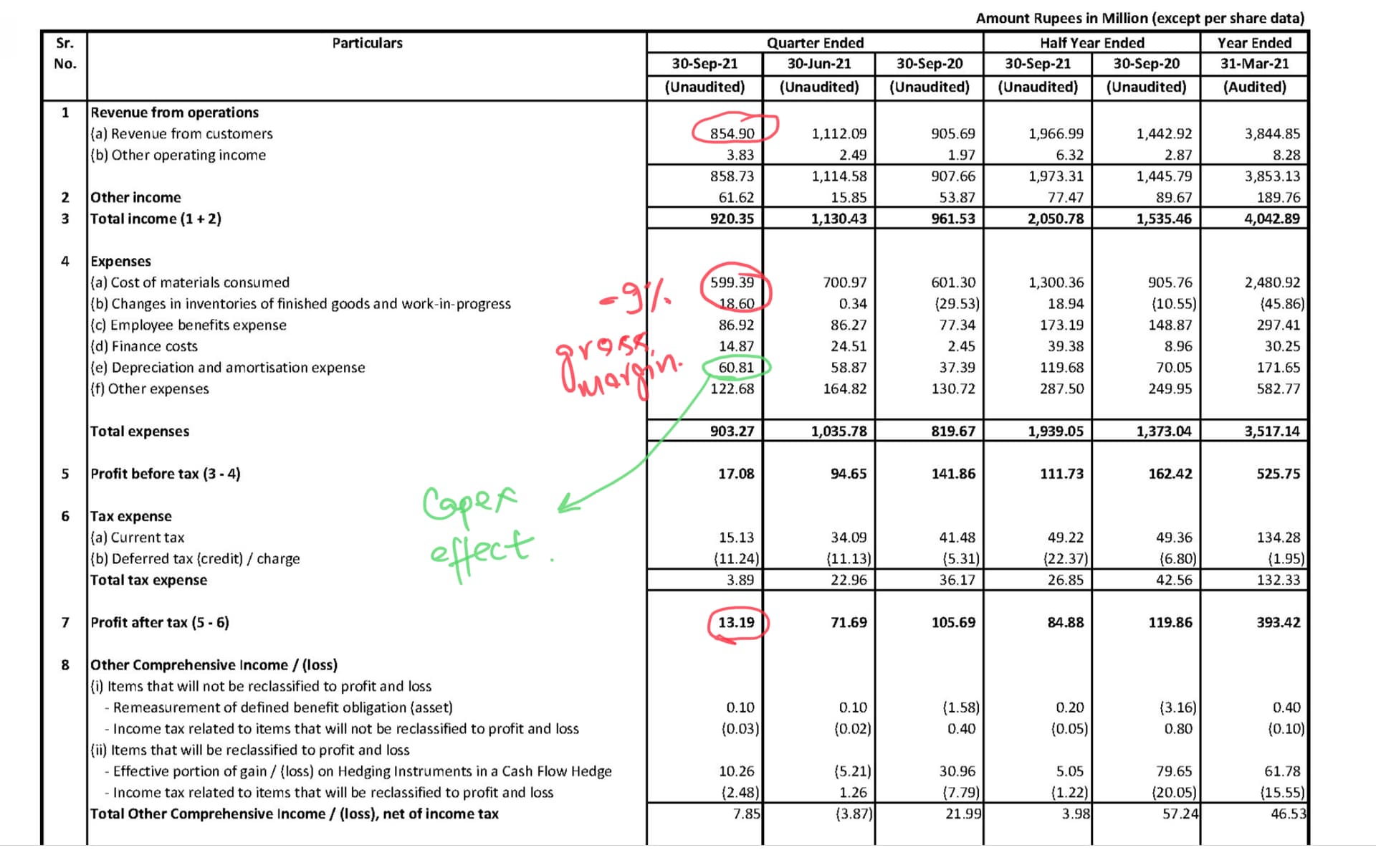

Tasty Bite’s Export incentives were 17cr in previous year . In this year it could be close of 30 Cr.

Mojority of EPS of tasty Bite is contributed by export incentives given by GOI So If Indian Government withdraw export incentives then there will be strong impact on cash flows .

ROCE will be in Toss .

What is your take in this risk?

2 Likes

Reason is low float ->

less than 6K people hold it shares -

4 Likes

Tasty bites is so overvalued right now why aren’t people selling(except for the buy and hold types who bought it in 2014 or so)? I mean if you think about it, it has a market cap of 3000 crores. If you are expecting even 10% return from this asset, fundamentally it would have to dislodge 300 crores in net profits annually. Even all the assets of Tasty Bites combined don’t equate to that valuation. It presently only does about 50 crores on its net earnings. Even if you argue that business grows at 26%(double every 3 years comment by management), it will take about 7-8 years to reach the 300 crore annual net earnings mark. By that time considering that the inflation itself averages about 6-7% annually, it will almost have to clock net earnings of almost 500-600 crores yearly. Thereby, another 2-3 years to reach to that value. Basically, you already seem to have got about 10 years worth of prospects baked in the present value. And if you are looking for returns more than 10% then the math gets even worse. Even though it seems to be a wonderful company for those looking at say a 30-40 year horizon, why risk it on the P.E. multiple speculation? Reminds me of this:

Insights, Criticisms, Perspectives?

9 Likes

Prime reasons of sky-rocketing valuation are low float, scarcity premium and sector falling under majority of people circle of competence. Yes, other factors like earnings visibility, low interest rate environment etc. are also at play.

Needless to say, valuations are pivotal in investment success, however nowadays that too has become debatable. Anyways, market folly can exist longer than anticipated. Best is to stick to investment strategy.

2 Likes

Looks like the company is expecting a huge uptick in demand and have announced a major capex of Rs 150 Crores(debt + internal accruals) over the next 3 years.

4 Likes

Mars opened the the World Market doors for the company in UK, Germany and Australia and many more to come. The reinvestments and ROCEs is already very good.

the management is targeting a massive scale up to 3X revenue from 400 crores currently.

The company has announced additional 150 crores capex for next 2-3 years, and this business has 3-4x asset turn. After coming of Mars, no capital problem nor any distribution issue. As distribution network of Mars if There’s no problem of Capital and no problem of distribution network.

2 Likes

Transcript of the AGM

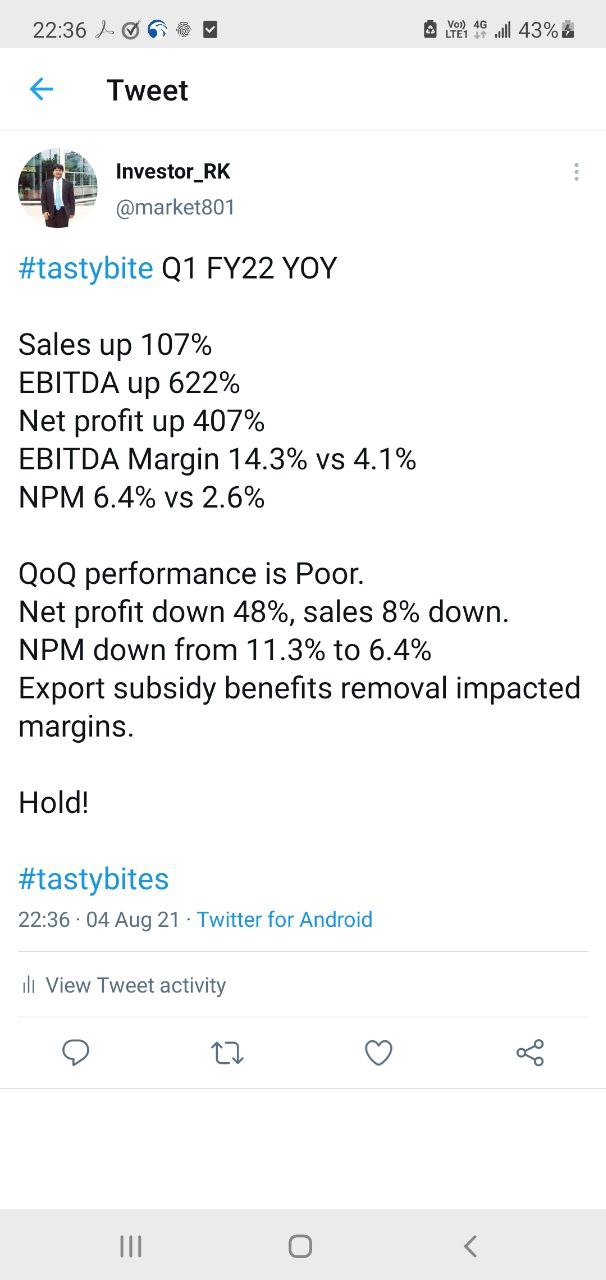

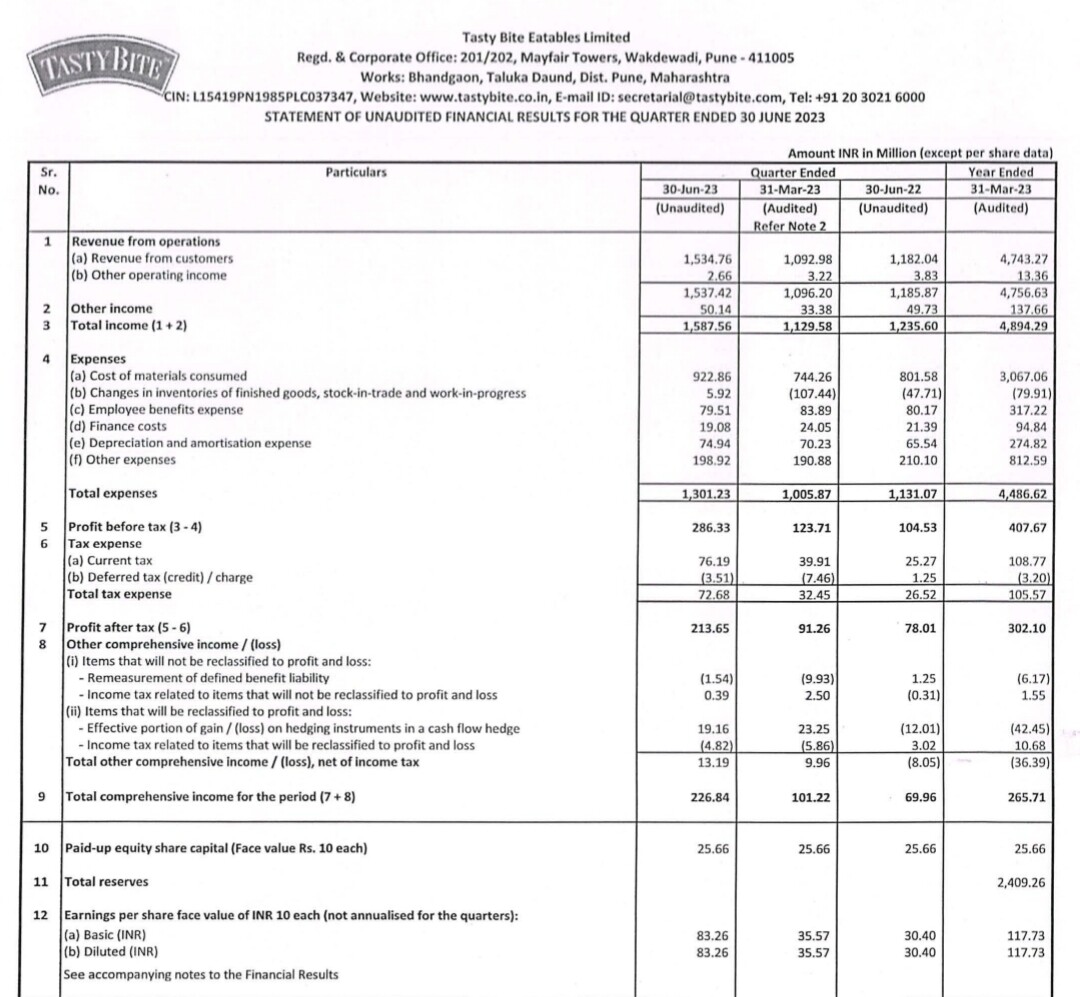

Any thoughts on the current qtr results?? What went wrong for them??

Just started looking at this - here are a few of my thoughts -

1 - The company did massive scale up between 13/18 with a CAGR of ~21% in sales and asset turns at ~5/6 times

2 - The capex plans got a little delayed and finally have come through - management expects the fully operational unit to start producing from Sep’23 / Stock halved during this period

3 - They has aspirations to deliver a billion dollar in sales in 10-15 years which translates to 32% / 21% CAGR respectively

4 - 70% of the business is outside India around the world - with Mars as the new guys, they might get a right to win in distribution

Happy to hear thoughts / feedback for folks who have tracked this

4 Likes

Also, who does distribution for Pedigree and Royal Canine in India?

Who is the MD ?

Co running without a Top management for 1 year +

Stock has halved, but what is the PE Ratio still.

Is the Old Chairman into competing business now ?

It is your letter to company. How answers are there . Answers shoud be in reply by company ?

The stock is already trading at 101 PE and if we expect 30-35% EPS growth in the coming 4-5 quarters do you feel there are still chances of PE expansion or will PE rationalise while mostly the return comes from earnings growth

Tasty Bite Eatables Video Recording of 39th AGM held on 09 August 2023

4 Likes