Looks like finally they are putting to use money collected in QIP.

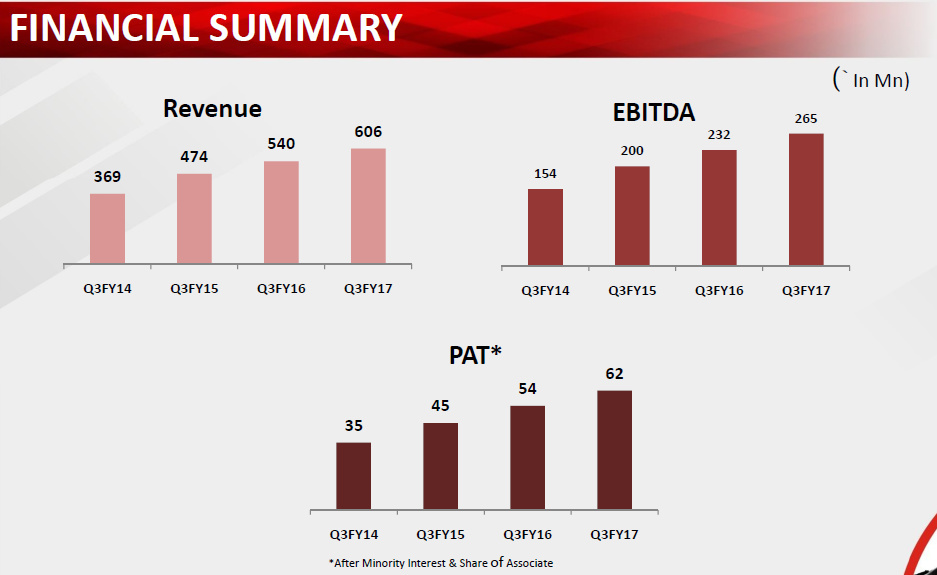

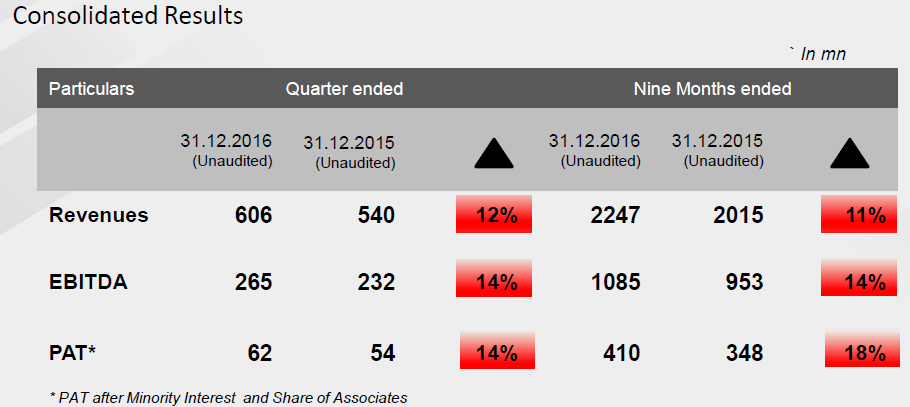

Their quarterly results were in line. Revenue up 11%, PAT up 18%. Margins at 53%. Quarterly PAT almost doubled in 3 years. Still the stock is ignored by the markets as it is available at 800 Cr market cap.

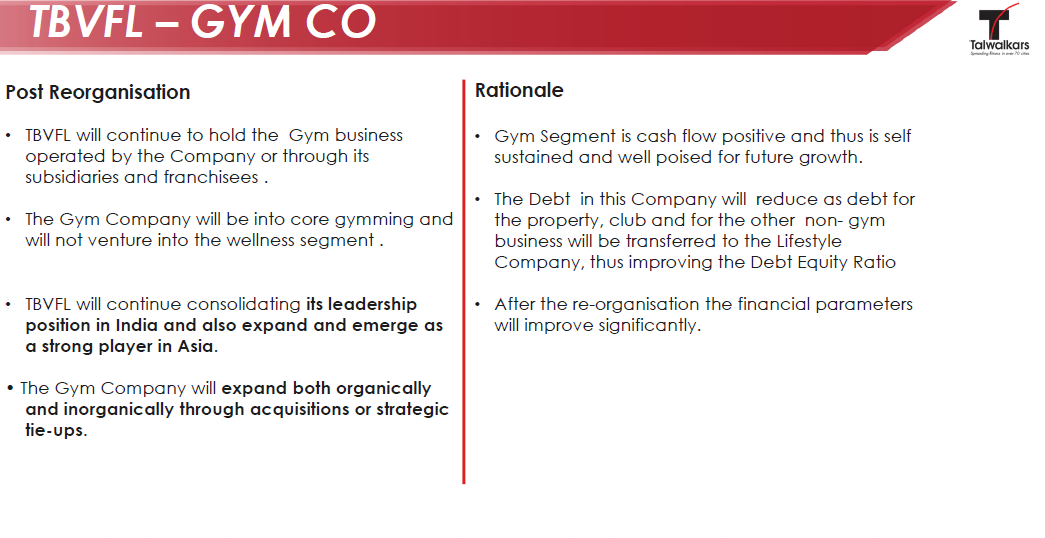

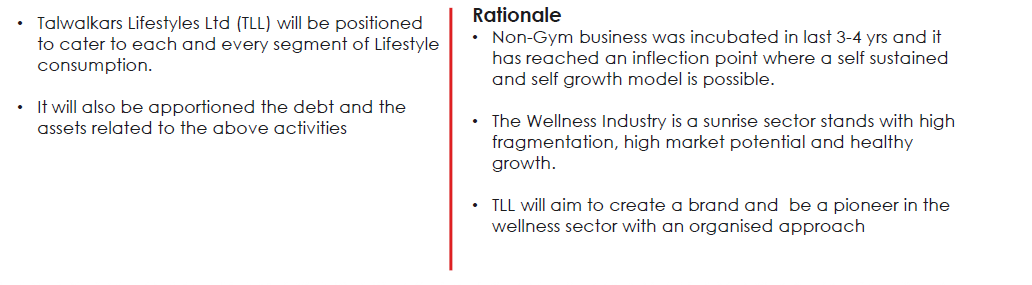

Company is proposing reorganizing into 2 companies - Gym company and Lifestyle company. Company organized conference call for the first time on Friday 11 Nov at 2PM

Real estate costs are make or break in retail esp true for gyms which ideally require 6000 sqft or so.

Possibility exists that long term leases are being recognized as capex.

Pure play Gym business will remain with TBVFL and rest “lifestyle” value added businesses like “Reduce”, “Nuform”, Zumba, Club JV et will go to Talwalkars Lifestyles Ltd.

Please see snapshots copied from investor presentation

This is illegal according to IFRS because revenue must be recognised in the period it is earned. The company should recognise a liability in an ‘unearned revenue’ which would be amortised for the duration of the clients’ memberships. Though outdated (I think) this also violates the matching principle as membership costs are recognised after revenues.

Can an accountant in the Valuepickr community please confirm this?

Not sure of the legality of the revenue recognition; but that is the reason you will note seasonality in their business with jump in Sep and Mar quarter.

Key negatives for me are:

frequent equity dilution, that is disappointing to note;

Frequent change in strategy. Until a few quarters back, they were trying to consolidate the nuform, reduce, zumba etc into main gyms to save space and bring in efficiency. Now they plan to demerge that.

super complicated group structure. Some legacy gyms that are owned by promoters but company doesn’t benefit. Then comes associates (in Chennai) and Lanka. Also, Talwalkar branded gyms are also owned by some other family members as well, which are not part of the company.

Not free cash flow positive: They have been saying that for a while now, but numbers disappoint every time. please go thru their CFO’s (Gawande) interview over last two three years (available on money control) and you will get the sense of what i am speaking.

It is difficult to hike the gym membership by 10 to 15% every year. The competition is tough in the market, especially from the unorganized guys and other chains including gold etc.

Despite all of the above, i am invested in the company at c. 220/ share (approx 5% of my portfolio). Key reasons:

At 200+ loose change, i see limited downside. Poriju bought in at c190/ share and we might see some further buying interest from big guys, limiting downside.

The business is in a way similar to restaurants, where we have seen increasing rentals killing the profitability. With slower rental increase, the company might just find breathing space to expand profitability.

The increasing push of digital payments and demonetization, will benefit organized players compared to unorganized, a benefit for them.

I agree with most of the points raised by you. But I have different opinion on your comment " business similar to restaurants". I think Gym business is quite different than restaurant as below

Membership fees are taken in advance

Gym can take more members than it can accommodate (as at least 30% members do not turn up in Gym)

Timing are far more flexible for Gym than restaurant

Gym is “better mousetrap” due to upfront membership fees. With restaurants, unless they have loyalty programs, people always love to try different restaurants.

Location - Gym has to be in residential area, in small corner of apartment complex whereas restaurant has to be in commercial area where footfalls are high. So restaurant rentals are always much higher than gym.

2017 annual report will be compliant with new rules. You would recall that only quarterly reporting currently is in new INDAS and that also, for few companies there is a grace period to comply

I am giving this a skip since it flouts some of my basic rules -

Some fuzziness in accounting. They have been doing a hybrid between cash and accrual accounting, taking whatever suits their interest best

Too much corporate action to my liking. Lifestyle club investment, acquiring a Sri Lanka based club while India remains largely untapped and now the demerger

Opened 20 gyms in Bangalore on the same day recently, something smells here. No better way to show sudden expense, if I were a promoter running a similar business and I wanted to siphon funds off this is exactly what I would do

Overall story and valuation look good but I am not comfortable for the above reasons

@Marathondreams my reference to restaurants was just with regards to real estate… personally I view this business as a hybrid of restaurants and asset leasing models, retaining the worst features of the two industries… apart from rentals, very capital intensive in nature to continue on a self sustainable growth path…

@zygo23554 agreed, more than a lot of corporate action it’s the contradicting actions that worries me… untill some time back, they wanted to merge nuform nd reduce, within existing gyms to save money and now this action…

New PWG gym contributed around 3.5% of revenue during the quarter.

The current quarter revenue was impacted due to Demonetization. The company opened 20 new gyms in Bangalore on the same day Demonetization was announced.

-New PWG gyms have a capacity of around 1000 members per gym.

This year CAPEX – 80 to 85 cr.

-David Lloyds Club- Still awaiting clearance from authority. The management is awaiting approval for all most a year now. It is a drag on the business.

January has been better than last year’s January sales.

Delisting process is going on. Hoping to complete this before March, but it may be delayed due to further approvals.

Intensify of CAPEX is reduced. PWG gyms have less CAPEX and more return hence will aid in high ROA/ROCE. Going forward, the company will push for this strategy more and more.

Going forward CAPEX will go down (?), ROE/ROCE will go up.

No plan to raise equity in the immediate future.

-Net debt- 240 cr.

As per concall, the management is focused on improving positive cash flows. Same store sales at 6-9%.

The company has a huge addressable market. Youth are already fitness enthusiast. But middle aged people of all income segments wish to join the Gym – they either look it as fashionable/trendy/impressive or the need arises out of any of the lifestyle disease. Whats more, post demerger, there will be a sharper focus on catering to the affluent Indians. Clubs, spa, message, health centers – where there are only a few listed players available at expensive valuations.

I became interested after watching a few people (whom I already knew for some years) got transformed into leaner and healthy individuals. Word of mouth is spreading fast…

Marquee investors like Prof Mankekar and Porinju are invested. Porinju had provided below rational for his investment in Jul16:

“So, today in the Indian market the market participants want numbers to come, then only they look at the stock. So, then it becomes expensive and people buy at very high levels, to get over-fancied. So, I always used to advice investors look for companies which are ignored and this theme of Adlabs and Talwalkars came to me because I was searching companies which have done very high level of capex in the last 2-3 years time. And on that capex numbers are yet to come. So, this is a theme. Not only these two companies, I am telling you, you can identify 30-40 very good companies especially in the midcap where these companies have done very good capex and I have seen some of those companies have done capex more than the market cap today and a reasonable debt. So, those numbers are going to come this year or next year or after two years. So, that is called value investing, that is where you can create multi-baggers and the stock may not be in fancy today because the numbers are not there.”

Read more at: http://www.moneycontrol.com/news/market-outlook/porinju-veliyathwhy-consumer-bizthe-tatas-is-doing-well_6963761.html?utm_source=ref_article

My biggest concern with Talwalkars is the presence of a lot of unorganized players in the gym segment. Nowadays in big cities, every nook and corner has a gym with decent facilities and equipment. I haven’t seen any of my colleagues go to a specific gym for brand value. If there is a good gym in their neighborhood with decent facilities they are happy to pay the membership fee.

I am willing to be convinced by fellow VPers on why a person would go to Talkwalkers instead of a gym 2 blocks away and I will be more than happy to join the bandwagon given the valuations now.

Talwalkars are expected to benefit due to GST driven move from unorganised players to organized players (as difference between them shrinks).

Gym membership is also driven by ego value in addition to the urge to look and feel good.

Another benefit being with chain like Talwalkars is you are allowed to exercise in any of their gym if you are a member. So you may go during the week in the gym near your office and at a gym near your home at weekend.

Organized gyms like Talwalkars has benefit of size which helps them to drive down costs and provide more standardized experience.

It might be useful by the investors to know that , country club members can use Talwalkars gym across India by just paying Rs 20/- as admin fee, per uses.

Disc:not invested but tracking

how will GST impact the small gym owners? Once gym equipment is installed only annual maintenance is required. The GST paid for the equipment can be offset against the small number of people who pay cheques. It is not like as if the gym owner is buying raw materials on daily basis. Most of the gym members are issued kaccha bills against cash which I think will continue in the future also.

Its about payment of service tax. Post GST, cost for unorganized players would go up by 15-20% decreasing cost gap between them and organized players, like any other industry.