Confirmed in the Q3 call that Guided 2200 cr for all of group sales by FY27. So, Talbros contribution is expected to be 1400 cr. So, Revenue is likely to be doubled in 3 years, approx 25-30% growth. Company do not have pricing power. Assuming 8% PAT, 20 PE, Market cap will be 2200 cr by FY27. About 35% increase. They are looking to increase exports to 35% revenue so lets assume 10% PAT, 25 PE, Mcap will be 3500 cr. So, essentially, 35% to 100% jump from current price in 3 years time.

They sold off the Japanese JV to Nippon for 81 cr (40% share). Their biggest customer is Maruti Suzuki. I would have preferred a Japanese company like Nippon on the board. Management said that the JV is growing very slow so they are focussing on businesses with 20+% growth potential.

With all this info, Risk Reward ratio seems tilted. I bought small tracking position since i did not have big exposure to Auto market and thought that diversified auto component player maybe a good bet. But now, I am wondering!

What do you all think?

3 Likes

current rev is 700cr pa. they are targeting 2100 by 2027. doesnt that make it 3x in 3 years?

I just listened to their concall. They said 2200 target was for group sales. Talbros has only certain JV % of subsidiaries, so, Talbros specific revenue target will be lower than 2200. Estimation is that it will be 1400.

1 Like

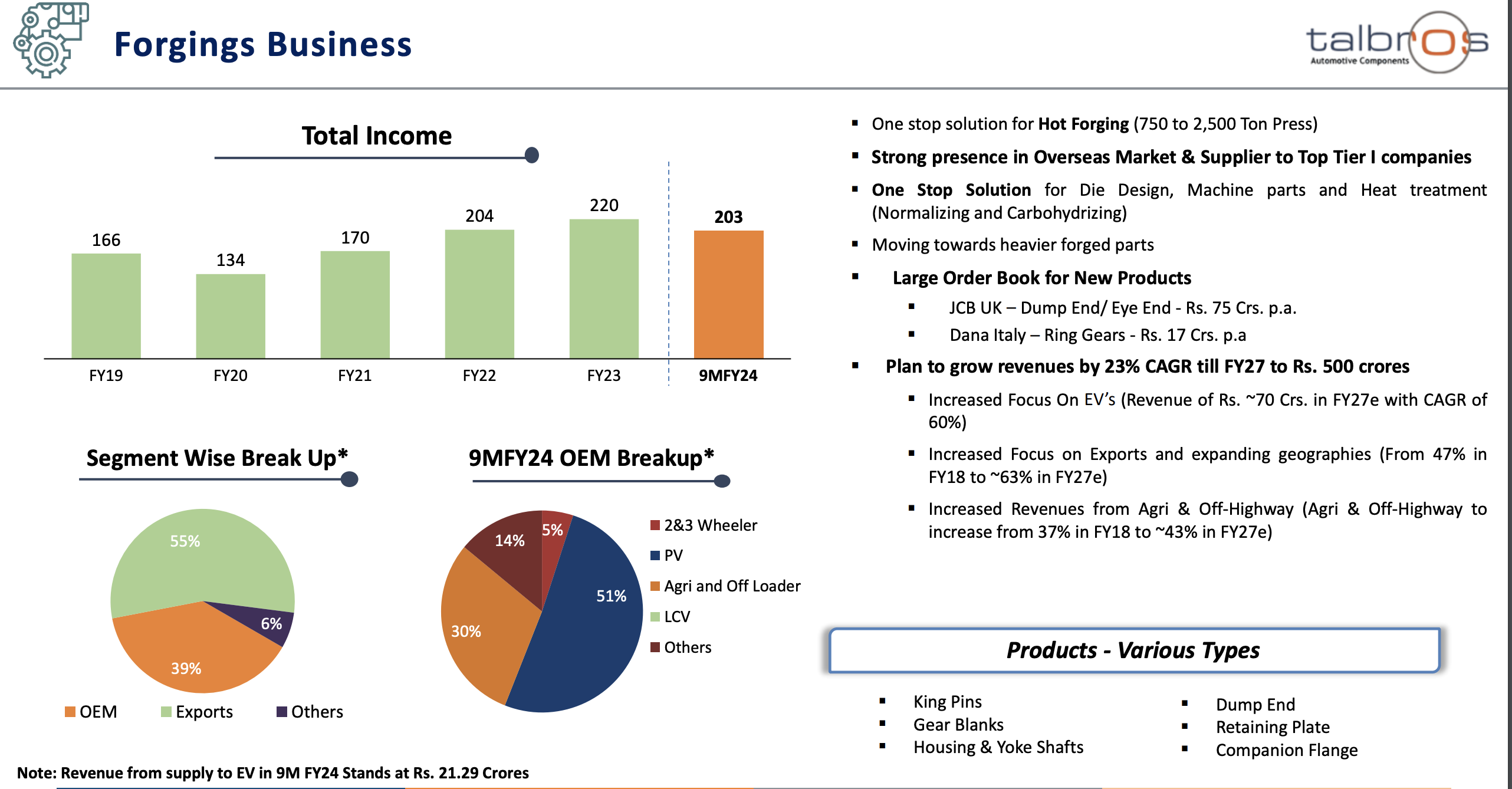

They have given the breakup in the PPT how they will achieve 2200Cr on group level.

700 Cr from the Gasket business, 500 Cr from the Forgings business. Another 1000 Cr from the JVs where they have 50:50 partnership, so we can assume 500 Cr revenue from the JVs. So Talbros sales could go to 1700 Cr if they can deliver.

As they have guided for EBIDTA margin of 15-16%, if they achieve that, PAT margin can go as high as 11%. They have achieved 11.3% in last quarter. That gives us PAT of around 190 Cr.

I haven’t accounted for debt reduction, which can further add to the bottom-line.

If we take peers P/E, most of them are trading at 30+ PE. In best case scenario, if they get 30+ P/E, market cap could go as high as 5500Cr+. In worst case, it could still reach 2400-2500 Cr.

5 Likes

Which indicator is it name please simple volume by

The only thing stopping me from buying at this price is stock being in ASM Stage 3 , can someone explain why it is in Stage 3