The love & attachment that Mr Jasti has on drug discovery has been a drag on the company forever. He has always focused on DD and neglected CRAMS, and the results are there for all to see. Suven has forever promised to do well but never really delivered on the promise.

If now, after the demerger, the CRAMS business, the one which actually brings home the money, is sold off, then I am not sure how the DD business will survive without any drug getting approved or atleast some form of revenue generation.

They’ve denied in the concall that they’re planning to sell the Demerged Crams business.

Quarterly Results Consolidated Figures in Rs. Crores / View Standalone

| Jun 2018 | Sep 2018 | Dec 2018 | Mar 2019 | Jun 2019 | Sep 2019 | Dec 2019 | |

|---|---|---|---|---|---|---|---|

| Sales + | 191.66 | 89.52 | 2.11 | 253.30 | 198.99 | 1.39 | 2.77 |

| Expenses + | 146.25 | 79.25 | 21.87 | 178.06 | 139.55 | 22.47 | 30.45 |

| Operating Profit | 45.41 | 10.27 | -19.76 | 75.24 | 59.44 | -21.08 | -27.68 |

| OPM % | 23.69% | 11.47% | -936.49% | 29.70% | 29.87% | -1,516.55% | -999.28% |

| Other Income | 8.13 | 6.59 | 6.74 | 3.75 | 3.01 | 2.38 | 5.86 |

| Interest | 1.07 | 0.59 | 0.00 | 1.58 | 1.69 | 0.11 | 0.10 |

| Depreciation | 5.51 | 5.56 | 0.99 | 5.46 | 5.55 | 1.42 | 0.86 |

| Profit before tax | 46.96 | 10.71 | -14.01 | 71.95 | 55.21 | -20.23 | -22.78 |

| Tax % | 44.59% | 63.87% | -2.78% | 47.30% | 52.54% | 2.03% | -0.18% |

| Net Profit | 26.02 | 3.87 | -14.40 | 37.91 | 26.21 | -19.81 | -22.81 |

| EPS in Rs | 2.04 | 0.30 | -1.13 | 2.98 | 2.06 | -1.56 | -1.79 |

Hello, Can anyone explain why there is a sudden drop in revenue in quarters ending Sept 2019 & Dec 2019 ? Am a novice and bit of explanation will be really helpful. Is it due to the revenues being assigned to Suven Pharma ? If so why had it happened in Dec 2018 too ?

I think mostly revenues would be in Suven Pharma - the demerged entity

Yes. Sept 2019 and dec 2019 have been moved to Pharma. But what about Dec 2018. I believe demerger started after Jun 2019.

Last year nos are re-stated when fresh results are declared

Appointed date for demerger was 1st Oct 2018

Suven Pharmaceutical Q4FY20

Concall Takeaways

We’ll be dividing the concall into 3 parts: Business, Risk, and Management. Since this is a little tricky to understand business. I will be giving explanations where I feel there is a need for it:

Business:

-

The business has been demerged between Suven Life sciences and Suven Pharmaceuticals. Only 6 months number can be compared, the yearly comparison is not possible as of now. The company has stopped giving the break up of Base Crams and commercial Crams.

-

Suven Pharmaceuticals consists of Process research, API, Intermediaries, Process development, Formulation, and CDMO.

-

The demerger was done to create 2 focused entities and moreover due to the fact that the market wasn’t realizing the value of Crams business.

-

Segmental Break up of Revenues

-

Crams business: Sales growth from 380 crores to 468 crores YOY.(23%)

-

Specialty Chemicals: from 216 crores to 304 crores YOY. (40%)

-

Forumulations& Technical Services: from 50 crores to 70 crores YOY(40%)

- For the quarter ended there was a small growth in topline and bottom line

On Capex break up

-100-110 crores for Vizag plant which is meant for Crams and Spechem

-90 crores for formulation facility.

-120 crores for Pashamylaram.

100 crore of capex is left which will be capitalized in FY21.

-Crams Business Updates:

-

New project acquisition to see some delays, as innovators are currently focused more on Development and not on discovery business due to the outbreak of COVID 19. Moreover, we cannot meet the clients, going a bit slow. Expecting things to normalize after summer.

-

Current projects continue as normal and expecting 10-15% growth.

-

The plan for CRAMS business is to forward integrate from intermediaries to Active Pharmaceuticals ingredients and to formulations eventually. Basically, moving from N-1 reactions to further down the chain.

-

Working with 3 more customers in the CDMO business, but it will take time before we can generate revenues.

-

Company doesn’t supply APIs yet, only into intermediates in the CRAMS business. There is a possibility odf converting intermediate business into API business in the future.

-

On Capex, one has to understand that the entire capex is not directly related to the topline growth in CRAMS business. Some part of the capex is done for the regulatory requirements. For example, Occupational Exposure Level, which is done on regulatory and clients requirement. If the commercialization happens, we will use the facility for what it is built for. Using it as a normal facility as of no. OEL (very little human involvement in production and fully closed atmosphere)

-

Seeing many opportunities, but revenues will only materialize when commercialization happens (basically, NCE molecule moves from 3 different phases before it is commercialized)

-

Color on capex: capacities are being created on the basis of future requirements and on the basis of interaction with the clients. Capacities are created on the basis of interaction with the customers.

-

Discussing the supply of API with a customer. Have made a proposal, they’re evaluating it. (major positive if it materializes)

-

Not expecting any new commercialization in the next 6 months.

-

As of now, the business has really high margins due to low volume and high margin intermediates we provide in different phases. When molecules commercialize(moves from Phase 3 to commercialization), volume increases, and sometimes the margins come down with high volumes. Despite that, sometimes margins remain at 40% Ebitda+ when a product is commercialized.

-

4 molecules are commercial as of now. Scalability depends upon their performance in the market, usually expect repeat business in 18 months.

-Not venturing into CRO, only do things at CMO side.

Formulation Business Updates:

-

11 ANDA’s which are under development. 3 ANDA’s to be commercialized this year, 2 have already been commercialized and expect 1 more to commercialize. 2 ANDA’s with Rising Pharma out of 11 ANDA’s.

-

Expect $2-4 Million kinds of contribution from each formulation. As these formulation target niche markets with not much competition. We have entered profit-sharing agreements. The bottom line contribution of these formulations is likely to be higher than the topline contribution. (value-added products)

-

Any conflict of interest with innovator: no, because these are generics and not in a blockbuster space, only doing it in small volumes and no confrontation with the customers.

Rising Pharma Strategy:

-

Rising Pharma: It’s a development and distribution company and has close to 40 partners. Company is in the process of filing 10-15 new ANDAs with the partners, some of those might fit the criteria of Suven Pharma, Suven will get the opportunity to bid for those first. Suven has acquired the stake in the company as a silent financial partner and this eliminates the need to look for a distribution partner for the formulations Suven will be launching. The reason behind the management fairly confident of growth in the formulation business in the next 2-3 years.

-

Reason for Acquiring Rising Pharma: good business which got into trouble due to issues between the promoter and the management. As management wasn’t running the business efficiently. Suven decided to come in as a silent financial partner.

-

Risings Performance: - The company has successfully turned around and Suven’s share in the consolidated Profits is close to 50 crores. Suven invested 250 crores in 2019 for a 25% Stake. From next year onwards, Suven expects dividends to come in from the company.

Specialty Chemicals business (Vizag Facility)

-

The second molecule company started a year before, has seen good growth and additional quantity for it.

-

2 more molecules are under development and will be launched by FY2021. Each of these molecules has the potential to contribute 50 crores to the topline. Expecting one major specialty chemical molecule to commercialize next year,

-

In specialty chemicals, have been supplying molecules that are patent protected. One of them has gone off-patent last year,

Management:

-

Guiding for growth of 10-15% in FY21. Growth can be between 15-20% after things normalize.

-

Bottomline share of specialty chemicals, Crams, and Formulation business to e 1/3rd, 1/3 rd, 1/3rd each.

-The goal is to move up from Intermediates to Api and formulations in the CDMO business.,

-Eventually will be using the cash flows that are being generated to acquire new technologies and to set up specifically dedicated units to innovator companies in the future.

-Guidance of 40%+ EBITDA margins remain despite changing business mix.

-No stake sale is planned: All rumors.

- Management hasn’t yet started the process of looking for new KMP’s. Busy in streamlining the businesses and covid outbreak has slowed down the process.

Risk:

-

No contracts for supplying to innovators, usually if involved in the process one can expect a 30-40% order for that intermediary. As innovator companies keep 2- sources of supply.

-

3 molecules that got commercialized in 2014, their patent will be expiring in 2025.

-Acquisition of any new project delayed by 6months,

-

Initially, Covid disrupted operations and supply, now business is back on track.

-

Capex necessarily doesn’t mean growth in CRAMS business, as some part of capex is also for regulatory and customer requirements.

My Views

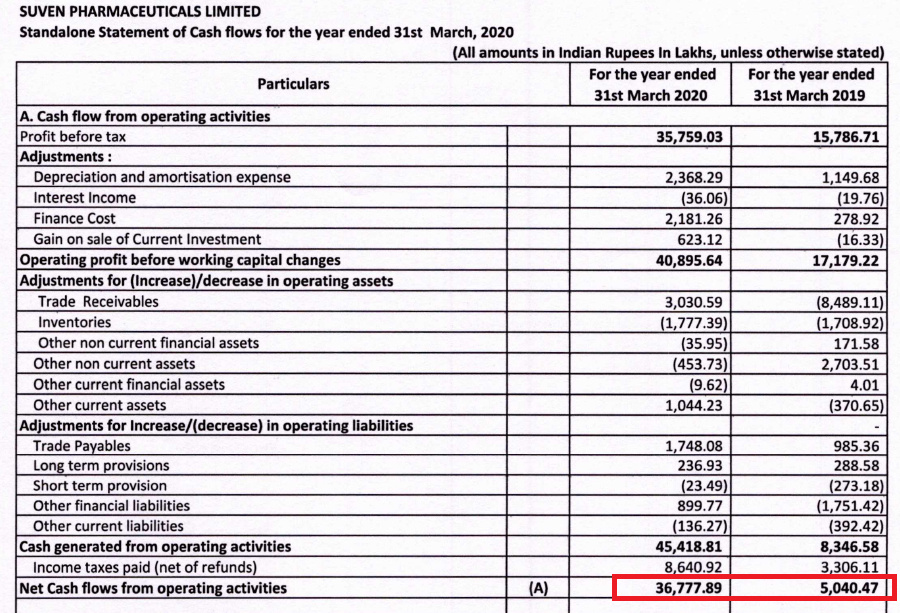

- How many businesses which have a ROCE of 30-35%+ and cash flow from operations of 415 crores (consolidated) you can find at such valuations+almost increasing the gross block by 60-70%, that too in a space where average PE has gone through the roof. Plausible for Suven Pharmaceuticals to become an end to end solutions provider as they focus more on the business. There are still some risks, as product concentration and uncertainty relating to the commercialization of new molecules is inbuilt into the business model.

Disclosure: Invested and this is not a recommendation.

Thanks @Worldlywiseinvestors for the summary. Its been mentioned multiple times in the thread that management focus has always been on the drug discovery (life sciences) business and CRAMS (pharmaceutical) business has been neglected for long time.

Do u think this remains a concern now also as the promoter of demerged entity is same. Wouldn’t it be great if some PE have been driven the co going forward?

@vivekbothra any comments?

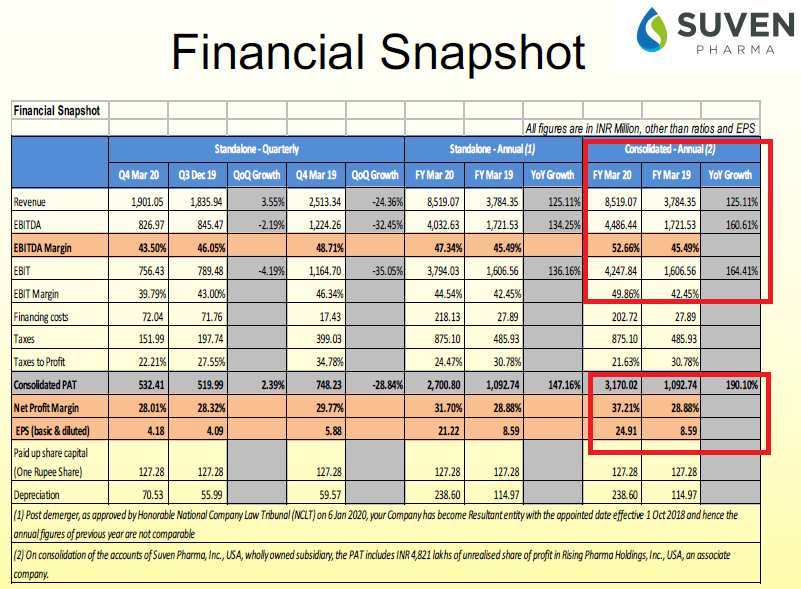

Q4 + FY20 Results

http://www.bseindia.com/xml-data/corpfiling/AttachLive/1d8b7001-8c8d-4af8-90f4-d63b8af9833d.pdf

Investor Presentation

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a4f36015-5b3c-434c-b547-f423e773f992.pdf

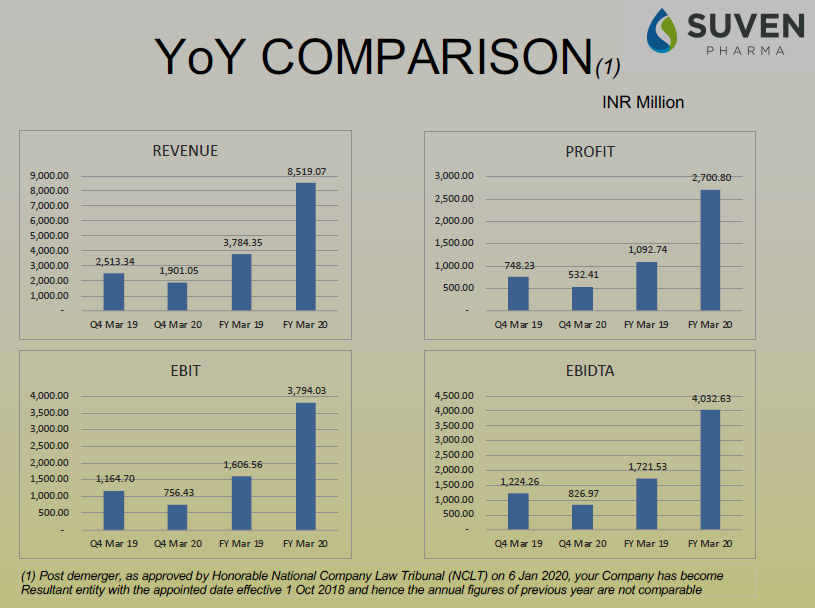

Post de-merger, the numbers seem impressive. Looks like the real value of the CDMO / CRAMS business is finally beginning to shine through.

Suven Pharma – Chemistry King

Written By – Jeevan Patwa

(21 June 2020)

Having worked on almost 840 unique projects till date, Suven Pharma is undoubtedly the king in chemistry with unmatched chemistry skills in India. Post demerger, the focus is getting sharper to grow on its strength. 840+ unique projects…because it works only for NCE crams and no generics…so every time it starts a new project, it’s different

Compare it with Divis, but Divis works on both NCE and generics…compare it with PI, PI is into Agro chemical space and now getting into pharma crams…Suven already commercialized two molecules in specialty chemicals and going to commercialized two more this year…in non Pharma - agro chemicals…. it started playing on its chemistry strength…Suven’s business is more than combination of Divis and PI …going to start formulations from this year but not like other Indian generic pharma companies with high volume and low margins…its focusing on niche small molecules where profits will be $2 for every $1 sale…focus is clearly on bottom line and that’s where it is able to generate 25%+ PAT margins and 40% RoCE…aiming to generate 1/3 profits from CRAMS, 1/3 from specialty chemicals and 1/3 from formulations in next 3 years

On CRAMS side, they are evaluating to supply APIs to customers which would be big positive, giving more value addition…

Investment in Rising pharma can give more positive surprises in the future…240 crs invested for 25% stake…in the first year itself, share in profits is 48 crs !!! it will also provide a front end for formulations in the future and revenue contributions to CRAMS vertical in addition to the dividends…

PI Ind is now getting into pharma crams, Navin Fluorine is re-rated because of pharma crams, though it’s still small…Suven is already into pharma and agro chemicals

Operational metric is far superior than Divis, Navin and PI … be it margins, RoE, CFO, Debtors and valuation is far more attractive than all the three above…far lower PE and EV/CFO…

Succession planning - Elder daughter of Mr. Venkatesh Jasti is a doctor and scientist and handles Suven Neuoroscience whereas younger daughter is handling Suven pharma…she is been the customer face since last 4-5 years handling customer negotiations…she is MBA from US and done engineering graduation in India…

Anyone has any color on what kind of value addition is there if one moves from Intermediates>API>Formulations?

Wrote a thesis note on suven Pharmaceutical-

Haven’t included the technical services business and the geographical location of the plants

Disclosure- not a recommendation. As I am biased.

Suven Pharma – Chemistry King – Part 2

Written By – Jeevan Patwa (23 June 2020)

In this part, I am going to delve little deeper into the business of Navin, PI and SRF to make a point how Suven should command valuations at par or may be higher than these peers…

As per company presentation, for FY20, Navin reported 1,022 crs operating revenue with 25.5% EBIDTA margins and 22% PBT margins…Important point is high value business which includes specialty and CRAMS contributed 54% to the top line…means 554 crs coming from specialty and CRAMS whereas 478 crs come from legacy business…focus is to grow specialty and CRAMS and hence the re-rating….Suven reported 763 crs from specialty and CRAMS in FY20…

As per company presentation, for FY20, SRF reported 2975 crs (41% of total revenue) from chemicals, 40% of which, is specialty…EBIT margins for the segment is 17%…films and technical textiles business contributes 60% to the revenue and EBIT….almost 1.5x than that of chemicals…and still it commands a PE of 28 !!! Cosmo films, Polyplex trades at 5 PE…if we give 8 PE to non-chemicals then market is giving multiple of 60 to chemicals business of SRF where specialty is 40% !!!

Market might argue about visibility of revenue and growth for the future…Navin won a contract of 2800 crs for 7 years…400 crs a year after Mar 2022…capex required 461 crs…means asset turn of less than 1…and company says it would have “Company level EBIDTA and ROC”…means 25% EBIDTA and around 20% ROC….will customer giving 2800 crs contract for 7 years offer handsome returns and margins? Look at PI, lot of long term contracts from MNCs with multi-year visibility…RoC is in the range of 20-25%…revenue visibility with sacrifice of returns and margins…

Now turn to Suven…11 ANDAs files till date with 6 more in pipeline…each ANDA to generate bottom line of $2-4 Mn …capex for formulations 160 crs …will be operational by Dec 2020…Calculate the ROC…and also the revenue visibility…4 molecules on commercial CRAMS side with patent protection till 2025….till then 3-4 more molecules may be commercialized since more than 30 projects in phase II and 1 in phase III…if they are able to move forward from intermediates supply to API supply… CRAMS number would be very different… specialty chemicals has been ramped to 300 crs in last 3 years with 2 commercial molecules and 2 more to be commercialized in next 18 months…doesn’t it provide sufficient revenue and growth visibility??? Even after the run up, its still trading below 20…

hi Mukul - The demerged entity has got very favourable economics - Superior Cash generation ability, Repeat Business , Multiple pillars of revenue sources . Management in last concall indicated that they dont intend to sell the entity. For me thing to watch out would be how will they allocate the surplus cash (~100 Cr) every quarter previously this was going to NCE division. So watch out for CAPEX that will be lead indicator for their success

I’m really ambivalent on the prospects of Suven lifesciences. Whiile the opportunity may be significant considering their play in the CNS market where there are unmet needs, I believe their current economics of being earning only interest income from Suven pharma along with the recent failure of SUVN 502 to meet primary end point looks a long shot.

There is absolutely no way to value a business as volatile as this and the only way forward seems to be tracking the clinical development and hopefully talking to mangement. Can we as a group organize a call with their management specifically for Life sciences. This is a relatively new space since drug discovery is more niche and indian phrma are more crams, api oriented.

This is a long shot but atleast worth considering. what say?

Seems an excellent & timely report. Kudos & big benefits to VPers who bought it. Valn still ok IMHO specially on compartive basis & 3-5 year POV. Good promoter & huge opp size. CDMO sector currently a fancied one.

Besides trigger of focus on CDMO after demerger ,2nd chemical molecule got commercialized & now a new chemical launch becoming commercial next year giving good growth even in fy 22.

One more trigger is the stake in Rising Pharma among precious few pharma distributors which they bought very cheap as 25% equity stake & gave 10 million USD profit already. New capex also pending to get commercialized of 120/320 cr is another trigger for this high ROCE,CAGR company where EPS & PE are both expected to increase leading to big wealth creation.

Discl- Invested with good qty post demerger & results

The customer and product concentration risk will be an overhang on the valuations as compared to Divi’s, Syngene etc I think. Tracking development of newer molecules will be key here as operational metrics look great