Why Susindar why? you did the utmost brave thing by booking loss and staying away from markets. Then You make a reentry buying mostly midcap and small cap companies. You could have waited for the election results and then made an entry as i have a feeling till the election is over the stock market is not going to go anywhere.

You could have added some bluechips market favorites or some big names in the mix. like say bajaj finance, maruti etc… which have corrected some 20-30 percent. Anyways its my opinion as a friend so dont take it otherwise.

Posiitives i see is so much value in these picks so downside is very limited but huge upside potential. Like say suntv, the results were good, they might come in power next election, tamil cinema market is getting bigger and they are making big budget releases and raking in huge profits

There are different styles when it comes to investment. However for someone with less than 10 years of successful investment career, it may be better to shoot for a stable and safe returns rather than risky high returns. Choose within your circle of competence and diversify in sector and stock. I notice that you missed to diversify in the past and now you are choosing bad quality stocks. In the long run, management quality is Paramount. A Nestle could give you a stable 12 to 15% cagr but a PCJ could destroy 90% in 1 month.

@bully - thanks for your comments. I do feel that the market is due for a healthy correction. This is the reason I am 50% in cash and another 15% in high dividend yield stocks where the downside will be limited to an extent. But isn’t the big question always when? I do not want to wait 100% in the sidelines and regret missing the upside. On top, all stock I have bought have corrected a lot and are much lower as compared to their recent historical valuations.

Regarding blue chips, I would have loved to add some. But unfortunately, they have not moved much in this correction and therefore are still much expensive than I am willing to pay. There are some sectors that I avoid like telecom, auto, airlines etc where economics of running such businesses do not make much sense.

@Uservijay - thanks for your view. I have provided my investment thesis where cigar butt stocks are simply mis priced bets for the short to medium term. I agree the quality in these are questionable which is the reason my exposure is very low at 10% which I am happy to risk.

PCJ is more of a hunch as it has more Facebook followers than Titan. People in NCR region would vouch for its quality. This kind of shows the presence of a brand which stay in people mind for long no matter what’s happening in share market (similar to what happened to Nestle during maggi fiasco). Still there is a definite risk that this could go Gitanjali way. So I am never putting more than 2.5% of my portfolio in this stock.

Cyclicals are where if my timing is wrong, I am willing to hold until the cycle turns which again is risky and would mean meagre returns for a long time.

Cash cows are high dividend yield stocks which could protect the downside in a bear market as I am feeling a correction is due. Typically I would want my portfolio to be all fastgrowers, but at this stage the price is still not right for quality fast growers to diversify.

I agree that I could hide behind some blue chips such as Nestle. But I do not know when the music will end and I do not want to be the last person holding the stock when the music ends. I have a strong feeling any stock more than 30 PE and that is not growing it’s earning at the same rate is a ticking time bomb. Best example is Page and Gruh which were oozing quality which many valuepickr members would have vouched for. A couple of miss hits or disappointments is all it takes for the stocks to crash down. Maybe that would be the right time to buy those stocks like a Page at 15k.

Sitting on 50% cash is something that someone would do in 2017. I would not sit on that much cash.

I think it is warranted to sit on 25% cash at a maximum in this market. You will never catch the bottom anyway.

If you think there is another 20% fall due in the nifty ask yourself

How much of that fall will hit small and mid caps? Since they have corrected very heavily as it is.

Assuming small and mid caps do get hit, how long will they stay there and will you buy aggressively at that point or wait for further fall making the whole point of sitting on cash irrelevant.

Are you willing to take a 20% downside by deploying more at current levels?

I would sit on 25% cash in this market. It is a buyers market. And yes it could fall more but we could also be at the bottom. Besides when you take a long term view, this small 20% movement wont matter as much if indeed it does happen. And moreover it wont sustain for long. Assuming you can never catch the bottom exactly why do all this drama of 50% cash and investing in dividend yield stocks to avoid downside. Now is the time to buy businesses at lower prices not hide in low beta stocks. You might as well move to 100% liquid/debt in that case. A Castrol isnt going to make you more than 6% cagr for the next 3-5 years anyway.

@dumboinvestor - I agree small caps and mid caps have taken a beating and is available at attractive valuations. But on second look, almost all stocks that have fallen are very low quality stocks with zero moat. The likes of cyclicals which have run up far ahead of their fundamental are the ones falling like ten pins now. You just need to check their price 5 years back to see how much they have run up. Honestly, the way things are going, if a commodity down cycle starts (it has not yet started), such stocks would probably fall another 100% from here easily. I would want to buy a cyclical only where there is a trigger like iron ore and valuation are around all time low in a normalised earning (not peak earnings).

I am not sitting on 50% cash waiting for a correction. I am rather waiting for the right price on my watchlist stocks. I don’t want to have all my portfolio as cheap and low moat stocks. Likes of LTTS and LTI would be good to add at 15PE or less rather than loading on Graphite and HEG at 3PE. Hence the reason I am waiting.

I agree Bajaj consumer would probably not make me rich. But Sun TV or Thyrocare can. So currently I am just trying to balance between risk and reward. When high moat large caps correct, I would latch on the opportunity.

Nobody has told you to look at cyclicals. There are many quality small and mid cap cos with good visibilty and a good competitive advantage available at reasonable if not attractive prices.

You have simply assumed cyclicals because they are trading at single digit PE multiples and FYI that is very normal for a cyclical during peak earnings. Nothing new. You also need to understand that value often comes at a price. You need to determine if you are indeed getting value for that price.

An Asian paints today at 35-40x would present value to many long term investors. I ask you the question can you ever get an asian paints at 25x? Highly unlikely.

Many companies look expensive but they arent expensive as you are getting value for them. That is what this market is giving you. Take a list of the VP favourites and look into them. A high quality company and business at 30-35x may not actually be considered expensive. You need to make a return. And a 15pe vs a 20pe makes virtually no difference in the long run if your idea plays out.

Cyclicals and turnarounds could be harmful for someone who is yet to learn the curves of stock market. Poor quality management stocks, even if they are 2.5%, will affect your outlook. Nestle was an example to show that slow compounding at lower returns is better than very risky short term bets. If you look at the market size for Nestle, they are not even 2% of saturation (taking developed markets as example). Price appears high if you look at PE but using it as sole valuation metric may be flawed. PE is good to look at payback period but NPV is much better metric to see final outcome. Of course a PE of 100 with no growth would mean a 100 year pay back period. But if you think that earnings will double or quadruple in the next 2 decades, suddenly PE looks cheap. There are many good stocks which could be at a PE of 30 and still have over 15 years of growth left in it. You could pick those with good management and steady earnings as they are certainly better than cyclicals. Turnaround is another big risk which can be played by really talented folks who love risk.

Thanks @Uservijay and @dumboinvestor. Your points have been well taken. No matter how much I try, I tend to keep an eye on the price and make decisions mostly based on valuation. I agree this has to change. Buying trash cheap is still trash. Also, cyclicals and turnarounds are best left for experts.

Therefore, I reviewed my portfolio and sold a few stocks. Accelya kale, Bajaj consumer, firstsource, irb, NMDC, PC Jewllers, satin credit care and rain are out. Not that I did not do my research before buying them. But I have decided to keep my investment thesis simple buying quality stocks for long term. I had low conviction in these stocks and my reason for buying them was mainly downside protection than long term view.

I bought LTTS, LTI at 5% each and AB Capital And MAS financial at 2.5% each. Still 50% in cash which I would be happy to allocate to double my current holding of 15 stocks at a more reasonable valuation.

Good Luck Susindar. One more thing I missed to state. During my initial 10 years of investment journey , I made a mistake of investing too much too soon. Now I invest in a stock and slowly add to it for 2 to 3 years. During this time, I sometimes have to pay a higher price but it helps me protect myself from making an incorrect decision. When our investment horizon is over a decade, we can take 2 to 3 years to accumulate the share!

@SlownSteady If you know your limitations then try and work around them. If you think you are unable to buy good companies due to whatever reasons then MF is always there. Investing is about discipline not stock picking. For people like you being disciplined can result in great returns. Leave the stock picking to the seasoned veterans.

Why did you buy MAS?

its a commodity business and has no moat. Can they raise funding at lower rates than peers? No they cannot because they arent a bank and have no CASA. They arent a bajaj finance either. So cost of funds wont be low for them.

Thier underwriting cannot compare to a bajaj finance/HDFC Bank/Kotak or even edelweiss.

They dont have a diversified business like edelweiss.

What is in MAS? It trades at 3.5x book vs edelweiss at 1.5x book and edelweiss is a solid business. They are paying a 20% div payout in a business where cash is raw material Why? Bajaj FInance pays out around 10% only.

They are growing fast apart from that I dont see much else. I also question your ability to track the company. So if something changes you may not exit and might take a hit.

Again AB Capital is a holding co. Why not consider their peers?

Sorry to be blunt but I think it is needed. We all are here to help eachother make a return and being blunt can help in many cases.

@dumboinvestor My reason for investing in MAS financial are uninterrupted growth for more than a decade of 20%+, management trust in their business (when they bought during the recent downfall), good ROE, improving margins, 5 year sales growth of more than 25%.

The company has some moat being owner operator with 74% holding and high quality growth being both sales growth and improvement in margins. MAS is currently a simple business. While Bajaj Finance is a great business, it’s high valuation and large size prevents me from buying it. I tend to stay away from 30+PE businesses. I am starting to look at high PE quality stocks. But it is still around the 20 mark.

AB Capital has a presence in five exciting businesses each of them have a long runway. The promoters need no introduction as they are among the prominent business families also known for good corporate governance. They have built a high trust for their brand which is very important for a finance company. Who would you rather trust with your insurance?

They have a strong promoter which would help in growth capital. They have business presence which complement each other. AMC can manage insurance capital. AMC will throw up free cash for their cash hungry financing business. On top, the biggest reason for me is a 3 year sales growth of 75%. They are growing at a great pace which means a number of levers are working in their favour.

I am not risking a big amount in equity investment yet and what I have put in, I can afford to loose. But doing my best to learn. My biggest challenge is conviction and holding for the long term which I am determined to do this time.

Valuing a levered financial instituition where cash is RM on a PE multiple in itself shows the lack of clarity in your mind.

You still did not define their moat. Promoter buying and high growth is not a moat. Being owner operator is no moat. You cannot call a big business a complex one.

Anyhow as long as you are convinced and have done research. Let us close this after your next reply.

I did mention their high ROE as well. In addition, all metrics that you would compare in a financial is good for MAS such as NPA, spread and PB. The negative is being a recent IPO, they are probably fully priced. Their growth history is available and impressive so there is no risk of insufficient data.

Regarding Bajaj finance, while there is no doubt it is an excellent business, it is fully priced no matter what metric we analyse it in. Having no strict comparison, it is also quoting at its own valuation and there is no way to say whether it is overvalued or not other than comparing to its historic valuation.

Strictly speaking, no financial institution Has a moat other than banks for their ability to create liquidity. But generally we can consider owner operators (data shows superior returns generated by such businesses) and high sales growth (ability to scale up) to be moats.

While I am not saying these two financial companies have impenetrable moats, they are a good balance of quality and value.

As you already know, there is asymmetry of information when it comes to these finance related businesses. We often catch the issues after it has happened and disclosed. Think about it. Do you really need to have financial company in your core portfolio? If you are in that Industry and are certain to catch an issue before others can react, you are good to go.

Hi @dumboinvestor

It is not always good to comment on any business just for the sake of commenting. It is better to understand their business rather than just assuming anything Read Annual Reports/thread to understand how company is different from other NBFCs. Their model is entirely different. The growth and AUM (growth of 40% CAGR) they have achieved is phenomenal. MAS has experienced 1995 Crisis , 2002 Earthquakes , 2008 and 2013 Liquidity Crisis. and have successfully navigated through it.

Company raises mostly through assignments and thus have No Asset liability match. Their cost of funds are below 9% (even most well known companies are not able to raise at such time) . They did not even faced any crunch during NBFC Fiasco . They work with lots of small NBFCs. Their Net NPA is below 1%. Management order of Focus : Quality > Profitability > AUM

In their words “To grow Top Line is easy but to strike a Balance between Quality , Profitability and AUM is most important for us”.

Promoters understand the business very well.

They have acquired their own shares from time to time , have high skin in the game and are generous to share decent amount of dividends from profit.

Don’t take it personally but i suggest , give your opinion only when you have read about the business.

Hi @SlownSteady ,

From your list of stocks , i own Mas and track thyrocare only. Both business are good though expensive. Can be bought in staggered manner. I believe both can do well in long run.

I would suggest to read more on this forum. Plenty of ideas can be found here. Also make a one page thesis for each of your investments especially the risks in those businesses and keep on monitoring the company performance from time to time.

No idea about rest of your stocks.

Though Yes Bank , PCJ , India Bulls does not have the best reputation in market. Edelweiss is still below its 2008 high and such volatile movements in its prices does not give any confidence. Since majority of stocks are correcting , it is better to have the best team when the market rebounds. These are the good times to study and pick the stocks.

I suggest you seek Hitesh Sir for his advice. He is one of the Gems of this forum and a very humble person to guide investors in a most sensible and appropriate way.

All the best

Thanks so much for a number of experts who provide guidance selflessly and assist amateurs in their investment journey. I am happy to say that I am one of @hitesh2710 followers. I am basing most of my investmet criteria on what @hitesh2710 usually advises such as to invest in market leaders, not to catch a falling knife, not to invest in a sector that is out of favour etc.

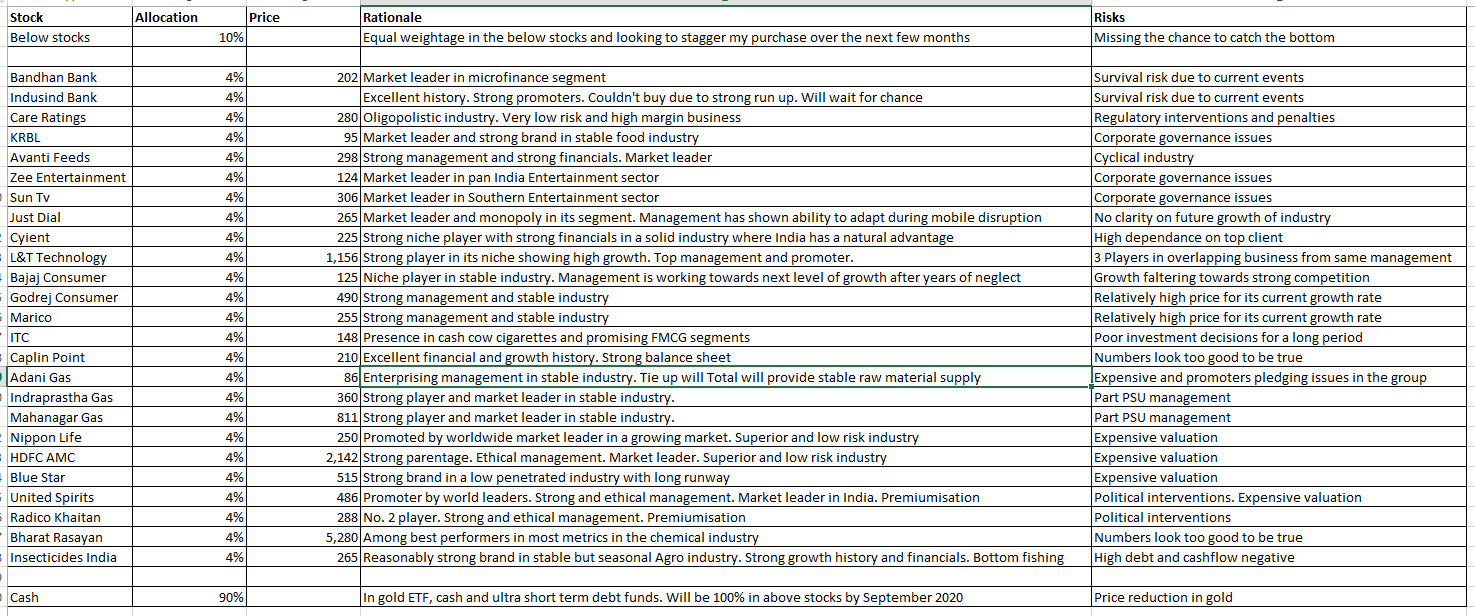

This is my second bear market as I have already seen 2007-08. I am lucky to sense what was coming (purely by chance) and hold 100% cash before the huge rundown. I am still down by 18% over a 2 year basis from 2018 which isn’t too bad considering my previous stocks picks like Manpasand, Dewan housing etc. I am starting to deploy this cash (first 10% yesterday) staggered over the next 6 months. I have already squared in on the companies I am looking to invest as below. Unless a quality stock falls to my investment criteria, I am unlikely to change the stocks in the basket.

I am also a deep rooted value investor (or I hate to say a bargain hunter). I have found that being a value investor is the worst thing to be in India as there is always a reason that a stock is available at a bargain. At the same time, I am one of those persons who can never buy Asian Paints, Dmart, Titan, HUL or Pidilite due to their sky high valuations. So here I am confused as ever looking to find a balance between Quality and Value. I hope that esteemed forum members would help me in this process as they have always done thus far. @hitesh2710 I am hoping for your feedback for the below portfolio of stocks.

I have to confess the below portfolio is an attempt to bottom fish due to the value investor mindset in me. So some stocks have risks which I have highlighted and I hope currently these risks are priced in.