Thanks Sujay, I was going through the coverage and come across Plant Growth Regulators

Looked up investor presentation to understand the product falls into this category , the product name is ProGibb (Application is mentioned as Citrus - May be widely used in Nagpur area where the only place in India that gives such high orange Yield - this is guess work ).

This product is from the parent company ValentBio (owned by SCL Japan - also you can see related party transactions ) , more details about the product can be seen here

As mentioned in the coverage their more focus is more on high margin products like this

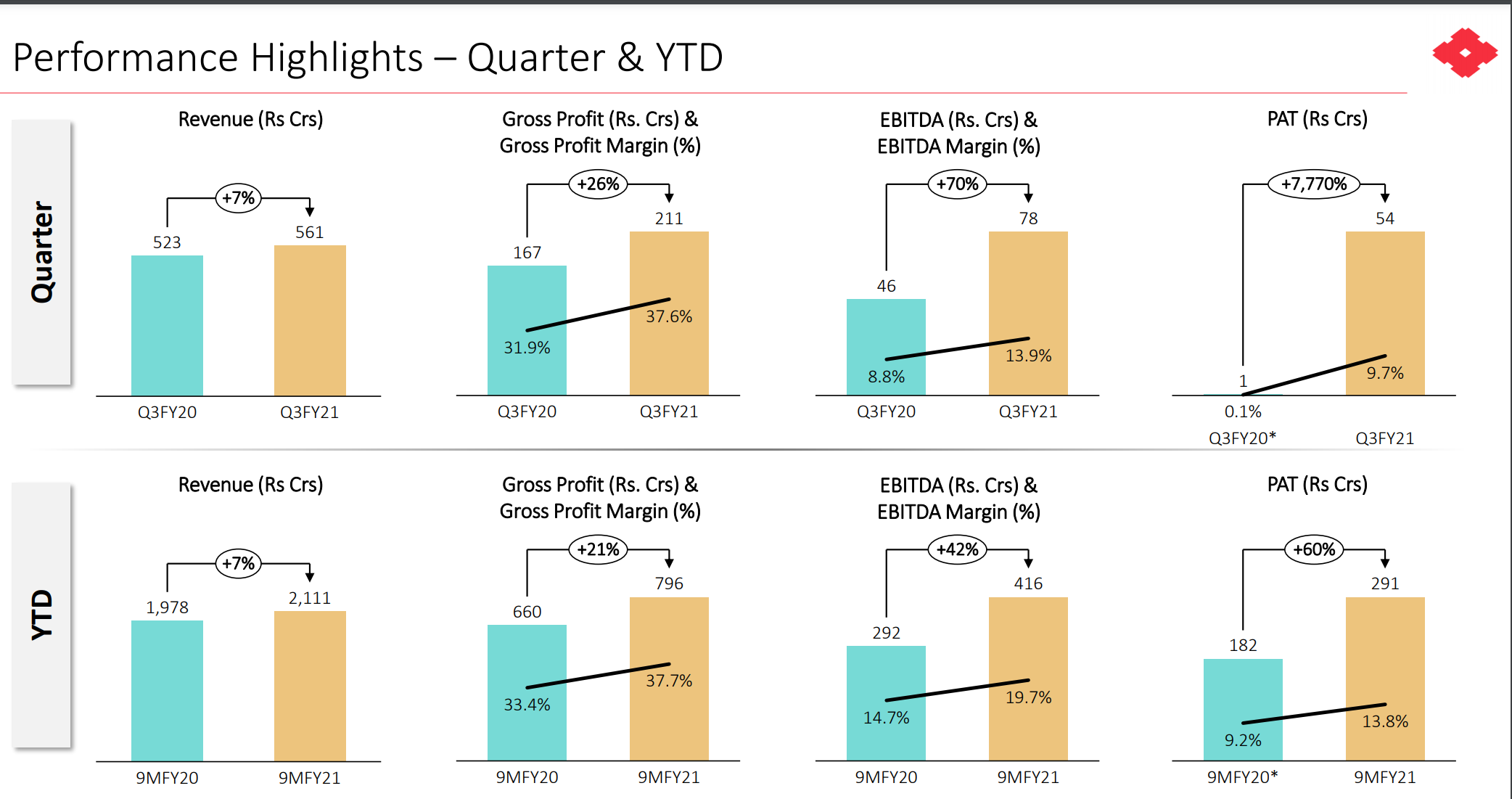

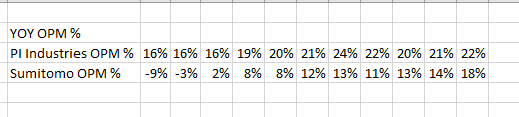

Topline growth is 7 % which is in-line with others. Rallis grew a similar 7%, Dhanuka 9%. Sumitomo margin improvement is due to inventory gains, so not as impressive as it looks. I think it will normalize in the coming months. What I liked is good improvement in working capital management, leading to strong cash flows. Concall is awaited. Stock is expensive and will continue to remain so in the current environment.

Exceptional growth seen in LATM markets (increased from 2% to 4% YOY , very bullish , this is playing out mostly due to parent company acquisitions in LATM )

Share of specialty products has gone up ( Launched total 7 new products out of which 2 are PGR - Plant Growth Regulators and two are Herbicides both of these are high margin products ) Link

Reduction in WC cycle

Cash, Cash Equivalents and Liquid investments of ~Rs. 532 crores

Capex :

75 crores capex is for the existing product portfolio capacity expansion

Additional Capex Rs. 100-110 crore over 1-2 years for 5 products, this is a trigger I am waiting for, CDMO opportunities from Parent SCC, expected to see the impact on the topline in 2 years (Expected to achieve more than 2x turn over )

20 acre privately owned land parcel adjoining our existing Bhavnagarsite and 50 acres at Dahej within PCPIR Zone(For future needs not for the current CDMO projects )

Growth Levers

CDMO for the parent SCC (5 products are already approved )

Also in discussion with many other global players (existing) for similar opportunities

R&D is also working on launching off patended molecules across LATM and SE markets, once these are ready to launch this might need additional capex

Current gross margins will be maintained , we strive to grow more than the current numbers

**Internal Process Improvements / Digital Transformations **

Deployed SAP S/4 - HANA solution for improve process efficiencies across the organisation

These will aid to run the data analytics and machine learning , observe the trends and manage supply chain efficiencies etc…

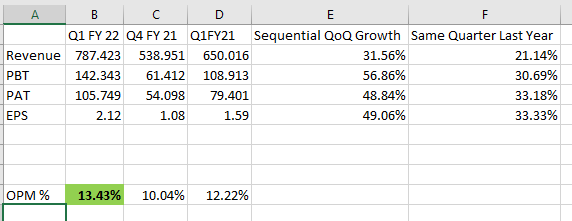

Someone in the thread asked earlier in the thread and here is the response from management : For Agro Chemical Company the comparison should be done based on the same quarter last year same quarter due to nature of seasonality in the business

Royalties

We don’t pay any royalties to the parent now and the same holds good for future as well

Strong support from the parent in sharing technical know how

Have full freedom from running operations from the Indian operations perspective

Exploring for inorganic expansion ( in the near future not immediate )

In my opinion winning this CDMO project from the parent for with 5 molecules is Pivotal moment for the company, if they can deliver this then un-limited opportunities follows after that.

Both are still important, YoY for usual progress and QoQ for comparing how business is doing compared to same Q last year. plus you will also understand the cycle this way, which Qs of the year are generally good for the business etc. but yes, no use comparing previous Q of same year.

From my observation, usually results from Apr-June and July-September quarters are good for Sumitomo due to monsoons and the other 2 quarter results are dull. But then for a stock trading expensively, revenue growth seem to disappoint me both QoQ and even YoY. Trying to understand the growth drivers a bit more.

Since this is a seasonal business, you should look at YoY numbers or numbers for the year as a whole. Prima facie, Q4 results look quite good. More details will be known from Tuesday’s concall.

Not a great report, just skimmed through there is not much to takeaway, no mention of CDMO opportunities highlighted in the Q4 FY21 concall.

Key Risks

Glyphosate ban, at the moment no impact as it is allowed to use in “pest control operators” but I looked up the list but can’t find mention of this (Latest link )

Interesting facts

Your Company is also into animal nutrition and

Environment health businesses – currently these are comparatively small businesses

"

The Company’s environment health business segment, catering to household insecticides players in the country, though small in size, is expected to grow at over 10% in the coming years. The growth of household insecticides market is driven by increasing awareness about health and hygiene, growing incidences of insect-borne diseases like malaria and dengue,

growing demand for professional pest control and ‘Swatch Bharat’ initiative of the government of India. The animal nutrition business segment, again small in size presently, caters to the country’s animal feed market, also has good growth potential

Some comments and observations from the Annual Report 2020-21:

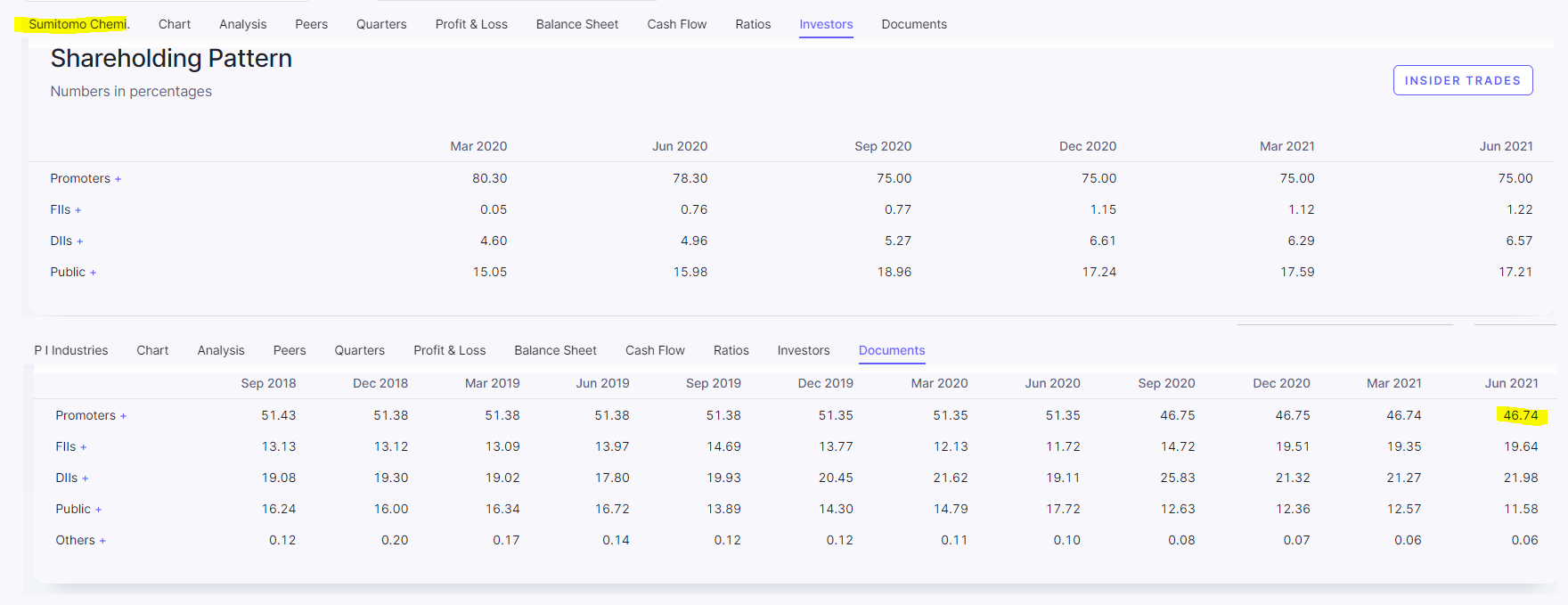

Sumitomo Chemical India Limited (SCIL) is primarily engaged in manufacturing and sales of household insecticides, agricultural pesticides, public health Insecticides and animal nutrition products. It is a subsidiary of Sumitomo Chemical Company Limited, Japan which holds 75% stake. The current company is a result of reverse merger between itself and the erstwhile Excel Crop Care Limited three years ago. It has two subsidiaries - one in Tanzania (99.94%) and Belgium (99% holding) with insignificant operations. Mostly legacy Excel Crop Care assets.

SCIL has a presence in all the product segments - insecticides, weedicides, fungicides, fumigants and rodenticides, plant growth nutrition products, bio-rationals and plant growth regulators. It is also into animal nutrition and environment health businesses – currently these are comparatively small. It does domestic marketing of proprietary products of its Japanese parent. It is also one of the few industry players having both chemical and biological products in its portfolio. It has strong portfolio of generics as well as specialty products and a strong marketing network and counts as a leading Indian crop protection company

In the year FY2020-21, business recorded all round improvement. Revenue was Rs.2643 crore, up 9% for the year. Profit After Tax was up from Rs.205 crore in FY20 to Rs.345 crore in the current year. Operating margin improved from 12.47% to 18.41% and net margin from 8.40% to 12.97%. Cash Flow from Operations more than doubled from Rs.221 crore to Rs.425 crore. Working capital position improved. Company became debt free, cash & liquid balances increased from Rs.168 to Rs.520 crore.

The company sells its products in both domestic markets and exports. Domestic markets grew 14% but there was a decline in exports. The reduction in export sales was mainly due to improved demand and attractive price realization in the domestic market as also the challenges in production and logistics posed by the pandemic and restrictions imposed in its wake in the first few months in 2020-21, says the report.

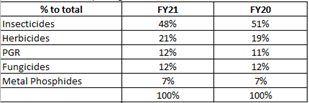

Further break-up of Agro Chemicals business is as follows:

In India, SCIL markets its products through a network of 65 depots, 14,000 distributors and 40,000 dealers. Though sales were up for the year, production was lower in the year (probably due to pandemic). However, the report says overall impact of the pandemic on the company’s operations is not material. During the year, the company expanded manufacturing capacities for one technical grade product, introduced a new formulation product and commercialized one new formulated product.

Inventories are a significant portion of total assets and therefore valuation of inventories is considered a Key Audit Matter by the auditors. RM inventories are generally okay but one has to look closely at the FG inventories. Total inventories were Rs.753 crore of which around Rs.400+ crore are finished goods. Increase in inventories was Rs.118 crore of which FG inventories was Rs.92 crore (in a PBT of Rs.453 crore). Long term trend in this should be watched.

Addition to Gross Block was just Rs.26 crore and Capital WIP is Rs.4 crore. So essentially there was no major capex during the year. However, in the Q4 concall the company announced purchase of two land parcels and significant expansion even in existing plants in the coming years. The AR however is silent on it and does not make any forward looking statement.

Dividend has increased from Rs.0.55 per share to Rs.0.80 per share, leading to a total outgo of Rs.40 crore Vs. Rs.27 crore last year. Payout is still quite small (PAT of Rs.345 crore) but considering the significant capex that lies ahead, I guess this is okay. I don’t expect the company to hoard cash unnecessarily.

Receivables written off increased from Rs.8.51 crore to Rs.20.54 crore. Aging of trade receivables is given in the Annual Report but “Not Due” and “Due less than 181 Days” is clubbed together. This is too wide a bucket and not of much use.

Purchases from Sumitomo group companies are higher than sales to them, as the company distributes parent’s products in the domestic markets. One hopes to see this trend reverse in future.

Overall as well, the company is a net importer, with forex earned being Rs.435 crore and forex used Rs. 642 crore.

There are no major contingent liabilities or tax litigations which is good. During 2020-21, seven cases were filed against the company in Consumer Forums

R&D expenditure was Rs.12.66 crore which is just 0.48% of the turnover. I guess the company should benefit from the parent company’s R&D, leading to significant savings for SCIL.

Director and KMP remuneration is reasonable. The two key executives are Mr. Chetan Shah (Managing Director) and Mr. Sushil Marfatia (Executive Director ). The total number of employees on the Company’s rolls as on 31st March, 2021 is 1722. There is a recognized employee’s union, 23% of the employees are members of the same. There are no ESOPs. This is rare these days, and something I like. Pay your executives well, but don’t give ESOPs.

The report says currently due to Covid-19 pandemic, farming is facing challenge of manpower shortages, with many migrant workers having left for their native places. It may take a few weeks for normalcy to return. Till then, application of agrochemicals in agriculture may be hampered. In the export market, demand remains robust given the need for food security. In fact, demand for specific agrochemical products has increased as buyers are trying to shift their sourcing away from China. Orders are coming in from key international markets like Brazil, Japan, the U.S. etc., given the cost advantages of India.

The key risks in the business include the industry’s dependence on China for sourcing critical raw material and intermediates. Report also says GM crops present a challenge and threat to the industry in the long run. There are also government policy risks. The Central Government has proposed a ban on twenty seven generic widely used pesticide products. It has also proposed that Glyphosate, a weedicide and an important product for the Company, will be allowed to be used only through ‘pest control operators’. The report points out that the proposal to ban Glyphosate if implemented will not impact exports but will impact domestic sales. It does not specify how much are domestic glyphosate sales.

Overall a good year for the business. A lot more excitement lies ahead, but the report gives no hint of the years to come.

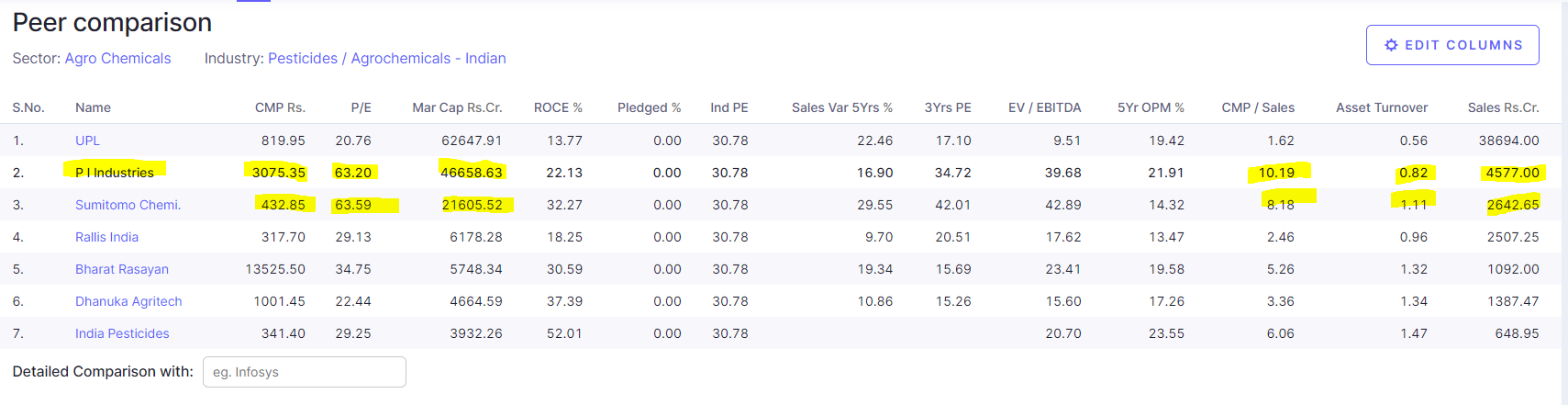

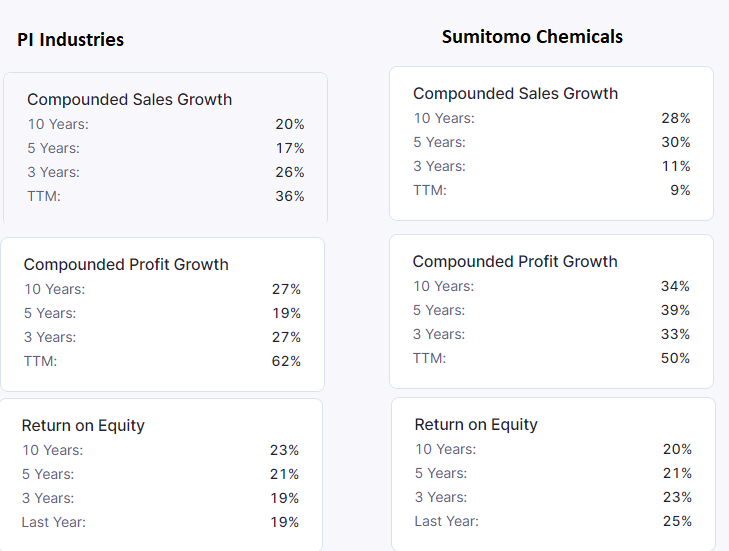

I was trying to compare it with PI (which is innovator kind of company ) valuations wise ( I am looking at price to sales not PE ) PI is still commanding a premium. But valuations should sustain only when there is earnings growth.

Results look very strong, especially given the context. Gross margin expansion, sales growth of 21% YoY and OPM expansion is quite impressive when across the board, the agri space has done poorly. PI domestic revenues were down, most others also came up with subdued results like Dhanuka, Chambal, Coromandel etc. Will wait for the PPT and concall (if they have) to get more details.

June Quarter covers the Rabi season

September Quarter covers the Kharif season

Monsoon this year more or less same as last year, if we assume the revenue growth similar to last year the same season. We are going to see first ever 4 digit sale in a single quarter (i.e., Sep-22 Quarter )

We can Also see there is business coming from other subsidiaries of parent (Refer the link )

Launching more products with the backing of the parent / subsidiaries (especially high margin products )

CDMO (5 Molecules order is received as per the previous quarter con call )

Any in organic acquisitions

New capex on newly acquired land parcel

Strengths

Top class A grade Sumitomo (Japanese ) MNC Management

Debt Free

No ESOPS

No Royalties to the parent

Low free float (75% owned by promoters )

7.7x price to sales

They also mentioned about animal nutrition in the AR.

What can go wrong ?

Change of Management (Still Excel team is managing the show but Japanese are on the board )

Adverse weather conditions (this is one thing is very interesting , with the global presence by the parent; can they build product pipe line { increase the revenue share from exports } where the business can become less cyclical ? this is not impossible with the new way of growing plants in doors - Hydroponic farming , vertical farming etcc )

Please share anti-thesis pointers, it is always important to know why I don’t like than why I like .

Please feel free to correct me if my understanding is not correct.

The key trigger here has to come from Animal Nutrient which is only around 7% now. Otherwise, it is a slow compounder. Buy when there is on blood on streets kind of stock. The traditional pie is a slow growth space ( herbicide and fungicide) and already there are too many players

That is absolutely the right approach! I think apart from the points mentioned above, one risk factor I see is around transfer pricing and related party transactions. Company already has a large amount of imports from the parent. Going ahead, exports to the parent and related entities (e.g. in LATAM etc.) are expected to increase substantially. With lot of imports and exports to related parties, even if the transactions are carried out on an arm’s length basis, proving the same to tax authorities can prove problematic. A lot of contentious litigation happens around these things. Besides genuine disputes, company becomes vulnerable to harassment by unscrupulous officers as well.