Yes thats i am expecting consoldiation/correction for 10-15days then result rally may start in sugar stocks.in 2nd half july momemntum will again pivk up…

I’m eyeing Dhampur for entry during any steep correction. Any other, better pic from the sugar space? Got to increase my exposure to U.P. Based Sugar Mills. Any other worthy contenders to keep in mind?

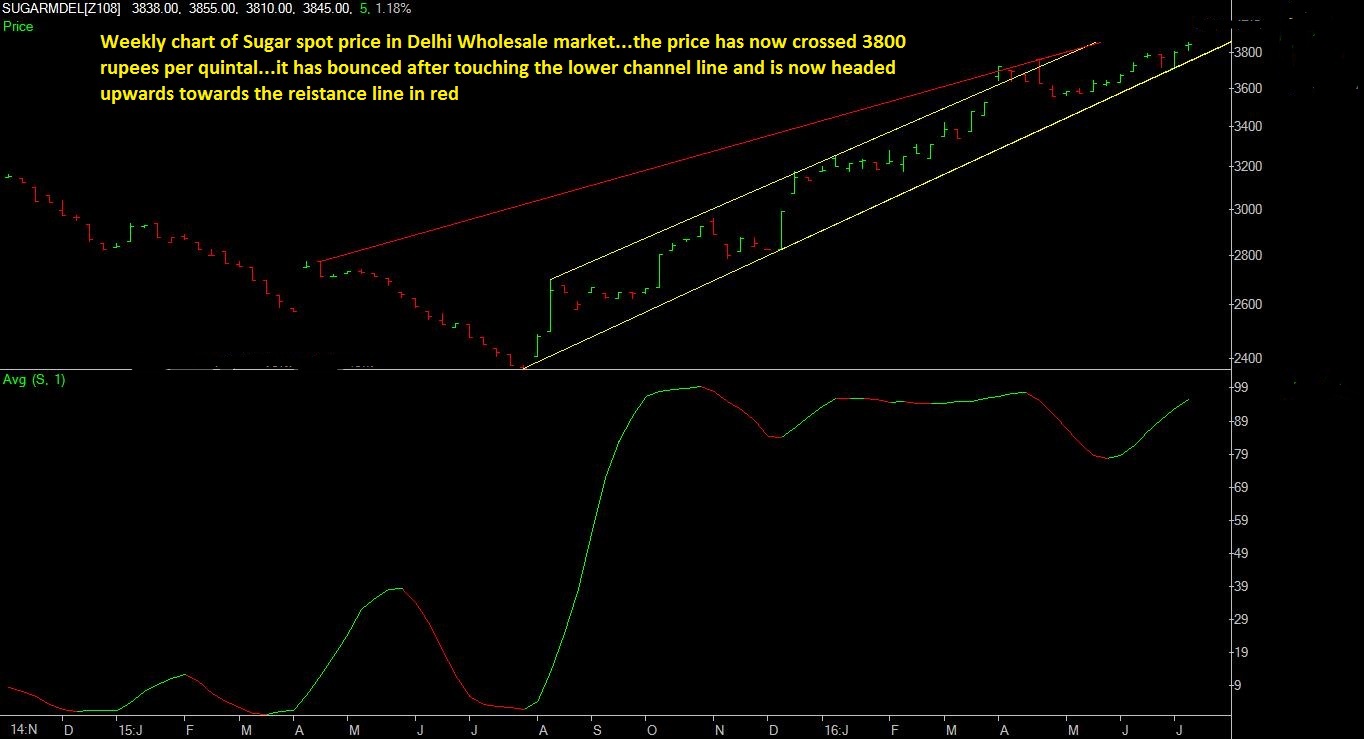

DISC: Holding Balarampur.

Upper Ganges has a board meeting on July 16 to discuss a scheme of arrangement for business restructuring. That should be beneficial for the stock as the arrangement includes 7 other companies and restructuring includes merger / de merger of various businesses. Upper Ganges is a stock to buy on declines. Atleast till July 16.

dear all,

any idea why renuka sugars has remained away from this rally?

inspite of being the largest sugar manufacturer in india, they seemed to be languishing close to their lifetime lows

Mehnazfitma please can you tell as per your technicals if corrections comes in sugar stock what could be the levels to add Dhampur Sugars. I wanted to more in big quantities ? And wat are your targets in dhampur till July 2017 plz

There seems to be some confusion about my qualifications…i am not a technical analyst. I am an investor who is trying to time my long term purchase using technical analysis.

I will hold on to the sugar stocks till April / May 20017 ( atleast)…i will continue to remain invested till i get very strong exit signals on ling term charts.

Insofar as Dhampur is concerned, i dont know how low it will fall…but i am more concerned with, when Dhampur will turnaround after the fall…if possible, i will post the charts when a turnaround does happen…

Fundamentally, Dhampur may sell 11 crore kgs of sugar in Q1… that translates to roughly around 55-65 crores rupees of profit. That itself will act as a support in this downfall…i dont see the stock going below 107 … making that as a very good entry point

9 Likes

All fast mover sugar stocks locked in upper circuit today including Oudh, Ugar and Upper Ganges.

Sugar results are no surprise, I doubt stocks will rally in ‘anticipation’ or as a consequence of good results.

If Balrampur is on the verge of a big rally then why is Mr Akash Bhansali continuously selling his holding. He got in last year around Rs 40 and I surprised that he doesn’t intend to hold on for another year by which time we expect Balrampur to be double of these levels at the minimum . Any idea ??

Mr. Bhansali had sold ~50 lakh shares around 15th June as well when the share price was around Rs. 125. Could there be a pattern or are we over-thinking it?

Technically, both Dhampur and Balrampur are showing signs of resumption of the rally in the next week. Maybe we have to look at it from another angle…perhaps it is the selling by the bhashalis that was keeping the price down.

Let us hope that the rally resumes from next week onwards…

3 Likes

hi mehnazfatima. ok got the reason for balrampur coz of selling by Mr Bhansalis but wat is the reason dhampur not rallying ? and mehnaz i read your analysis and targets for dhampur of 250 levels. dont you think it too conservative. I feel dhampur can easily cross target of 1000 plus in one year. here is my explanation for it , in Q4 15 results dhampur posted a profit of 145 crores. from tht 100 crores was by selling power, 30 crores from sugar and remaining from ethanol. now this time we have to consider the huge inventory gains and profits on new sugar tht will be sold from october onwards. so if u take for full year 300 crores profit from power, 400 crore profits from sugar and ethanol. total profit comes to 700 crores. total equity of 7 crores. so it makes EPS of 100. if you take conservative PE of 10 ( which is very conservative in mad bul run) price target comes to 1000. All your veiws welcome on this calculation. ( I have considered Operating profits so PAT will be lower so targets can be 1000 (±100 ruppees).

1 Like

Billionaire: almost all the mills are shut down by mid April …so they wont be generating any cogen after that…thus nost of the revenue from cogen is realized in Q4 and only a small percentage in Q1…in Q2 and Q3 there is no revenue from cogen.

Same is the case with ethanol…almost all of which is produced in the crushing season.

Thats the reason that i calculate that the revenue from ethanol and cogen, which will be around 125 crores will take care of interest and depreciation. While the profit from sugar sale around 200-225 crores will be the bottomline…

2 Likes

In the same way what do you think will be the profits of Balrampur for this qtr and full year.

Is Mr Tulsians prediction of about 130 cr EBIT for this qtr right. Also he said that as per his information the sales of Balrampur for this qtr were 19 lakh bags of Sugar.

The yearly profit of Balrmpur Chini is expected to be in the region of 550-600 crores…but that calculation is on basis of sugar realisation @ 34 rupees per kg but the domestic sugar price is in an uptrend so the figure of 550 crores may be taken just as a base figure with an upward bias…other seasoned boarders have estimated the earnings of Balrampur to be in the region of around 800 crores

1 Like

but mehnaz you are just considering the profit of 200-225 which is from inventory gains. what about the new sugar tht will be crushed from october. we need to consider that also right ? What are your profit estimates from the new crushed sugar.

Time has come for sugar stocks rally hold tight…be with some solid biggies like dhampur balrampur…along with some small cap sugar shares also…i am holding ugar dhampur and rana sugars…!!

Election in UP early 2017 there are chances that cane price to farmer will be increased which could hurt the earnings of sugar companies, has anyone considered what will be the impact on cos, if MSP is increased by 5 to 10%?