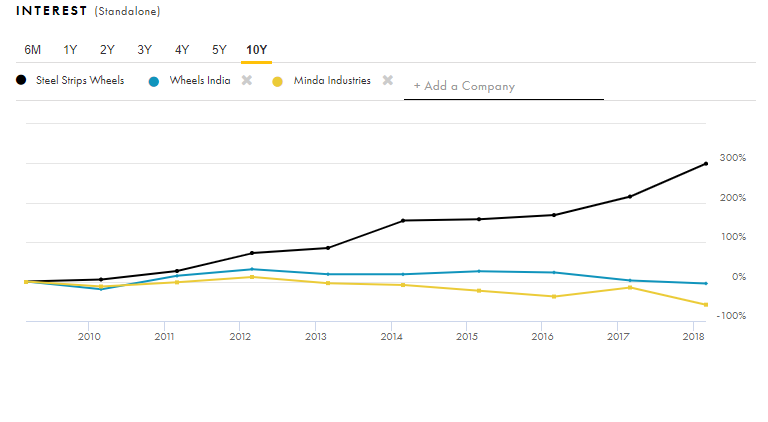

The recent orders are for the trucks segment exports which are having high margin products (2nd highest) 1st being the alloy wheels, their tractor and trucks segments monthly sales looks good in the recent bse updates and their plants are running at full capacity.

I have few concerns with sswl

There are few or no updates with the alloy wheel segments sales which are highest margin products.

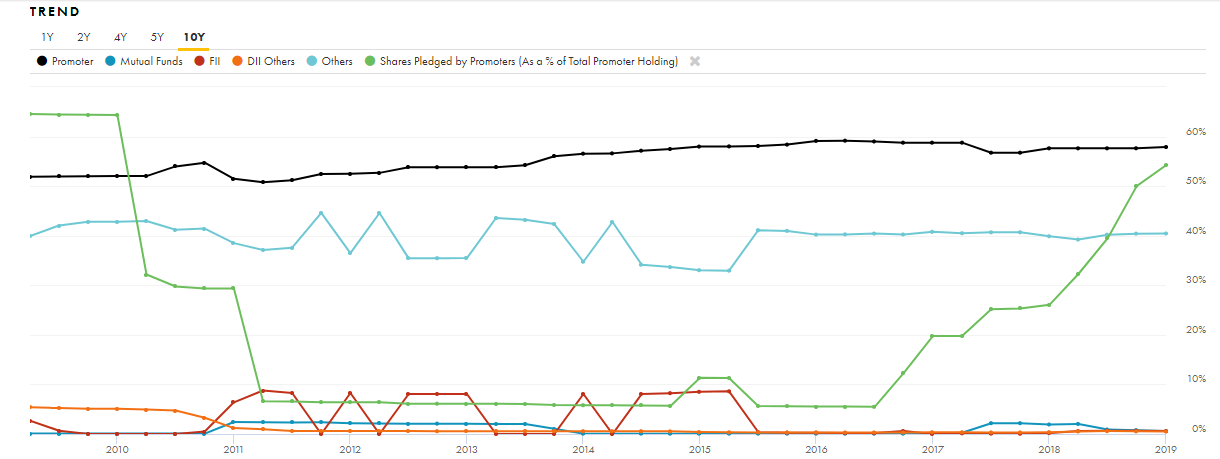

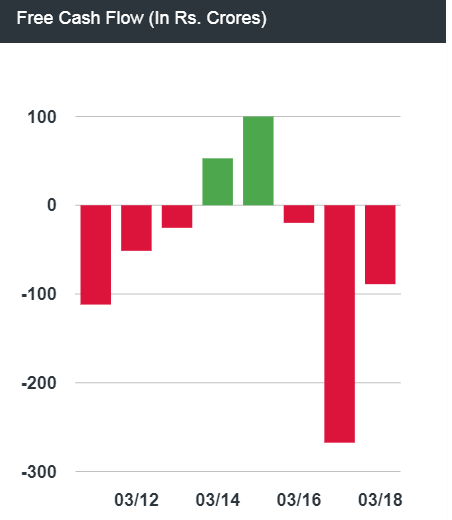

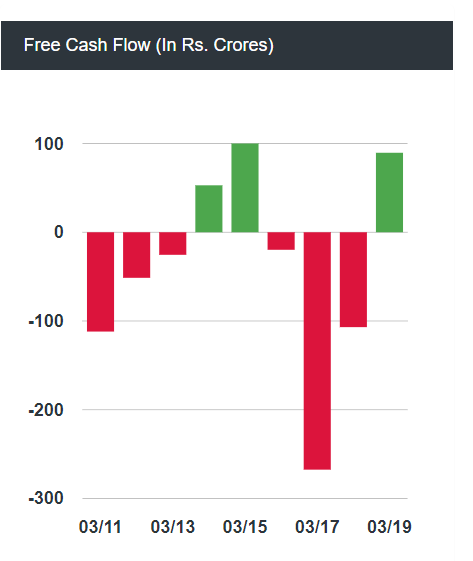

Debt is high and that is hurting the bottom line margins and their debt reduction will be 2 to 3 years long ,if they intend to do and also I have seen recent pledging shares which means more debt.

SSWL achieved January 2019 total wheel rim sales of 13.40 Lacs Vs10.60 Lacs in January 2018 representing a groMh of 26% YoY.

SSWL has achieved gross turnover of Rs 200.00 Crs in January 2019 Vs 156.26 Crs in January 20’18, there by recording a groMh of 28% and achieved Net turnover of Rs.16396 Crs in January 2019 Vs Rs.126.69 crs in January 2018, recording a growth of29%.

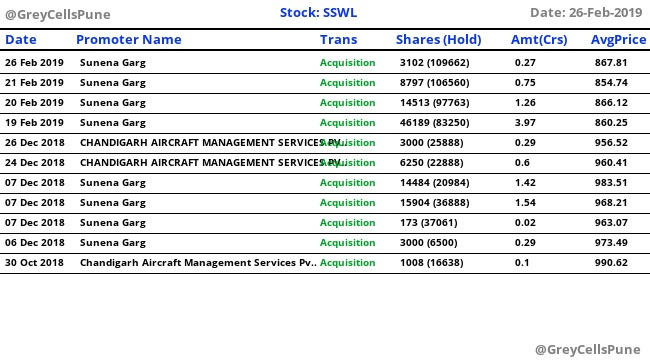

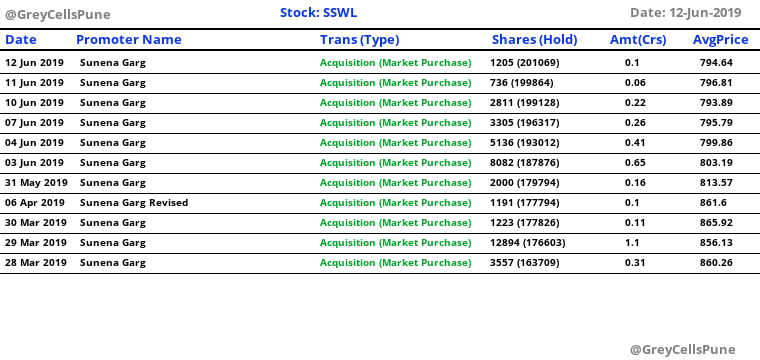

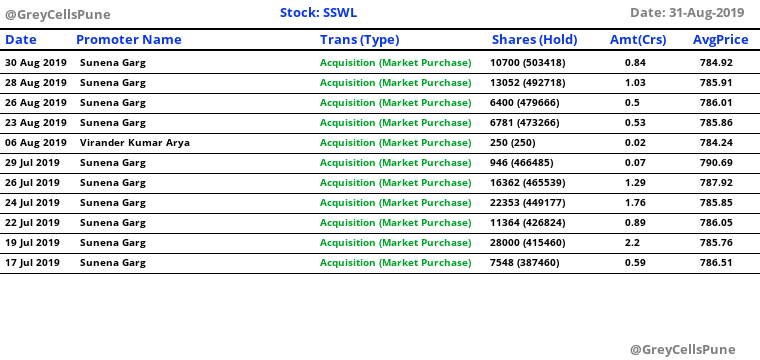

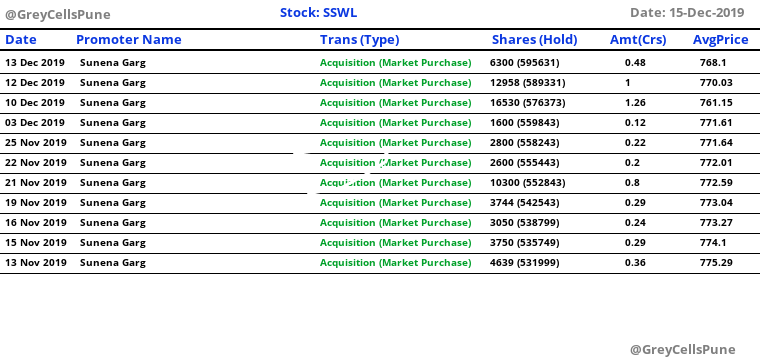

She had 750000 warrant issued in her name at 1140 last april. Not sure she is going to convert them after correction. maybe buying from market will be better for her. though warrant money could help in reducing debt, acquisition from market reduces float.

but too much playing around with shares by promoter- pledging, warrants, buying from markets etc.

Debt interest is 100 % pat…this is not just 1 year…this is from last 10 yrs…almost…can any company cant’t do it from last 10 yrs…to reduce the debt…how can we agree with management …they will do 8t for next 5 yrs…

SSWL has achieved gross turnover of Rs 197.22 Crs in April 2019 vs 211.79 Crs in April

2018, there by recording a de-growth of 7% and achieved Net turnover of Rs.161.O7 Crs

in April 2019 vs Rs.158.81 crs in April 2018, recording a growth of 1%.

Segment wise Breakup of growth

Segment April Growth (YoY)

Passenger Car -5%

Exports +67%

Tractor +3%

Truck -23%

2 & 3 Wheeler’s -21%

Overall -7%

Alloy wheel segment sales were at 27284 wheels in April 2019. with 2 more programs ramping up in Q1, we expect these volumes to add value addition to the financial performance and we expect to attain 600/o capacity utilization by Q3 of FY 19-20.

How do you see the company in current market condition? Market cap is ~750 cr & LT + ST debt of 900 cr. Its an oligopoly market. SSW has completed major expansion and now expected to increase free cash flow and reduce debt. If auto sector picks up then company can be a beneficiary. How do you see it?

Disclosure - initiated tracking position. Views are biased.

I echo …export expected to grow 35% fy21 and if any increase in domestic auto sales…will be a good trigger…only issue is …is managment really interested to bring down debt…no plans noticed on this …no statement any where on debt reduction plans…

Alloy is running more than 50% …so again…only managment plans to reduce the debt is question…all other triggers are in near future…to increase.topline and bottom line.

Disc: I have position, my views may be biased . Do your own research.