I think as a housing finance co, the NIMs are too high and non sustainable. The banks and Even housing finance companies have NIMs around 4% max. They must be Catering to lower strata of customers who are not eligible for home loan from bank or big NBFC. But this also brings in the possibility of NPAs.

16% of NP taken away as salary by MD indicates they may not remain fair towards minority shareholders.

A company where customers perceive risks will command low PE.

Indeed, their target customers are from the lower strata. In general my experience has been that they are not a big source of NPA expansions due to 2 reasons:

- Compared to the kind of draconian interest rates charged by the informal credit system (even > 50% per annum), the interest charged by formal sector banks/HFCs/NBFCs seem reasonable to them and they are able to keep up with payments (Here is one example of IDFC first bank CEO talking to one such lower strata customer).

- The ticket size here is quite low and hence the loan book is quite granular. This also makes NPAs a slightly less worrisome problem.

For comparison’s sakes, have a look at the NIM for Ujjivan Small finance bank. Agreed that NIMs of 12% are not sustainable in the long run, but it does look like financial institutions lending to small customers do have larger NIMs in general so it does seem plausible (does not seem to indicate fraud to me).

My opinion is that micro finance can not be compared with housing loan finance. Microfinance gets developed in a decade with a strong local force in huge nos. and it has a joint liability group. Microfinance is extended for establishing a day today earning and therefore any incident does not make it a complete NPA ( unless govt intervenes and creates new regulations like AP did in case of SKS).The debtor comes back to normal business post incident and starts paying again. So in my limited understanding , both are not comparable.

1 Like

Agree that micro finance and housing finance cannot be compared like apple to apple, but SRG Housing is preliminary into housing loans, so it shall be compared to NBFC as in general.

Results are out

Audio con call recording

Notes from the conference call:

Covid effects

- SRG Housing has given moratorium option to its customers. The customer base of the company is dominated by workers in essential services which have not been affected too much. Also, rural areas are doing relatively better and this is reflected in the relatively good loan repayments. 88% of the customers pay online. 30% of the customers have availed the moratorium.

- People have realised the importance of having their own home during Covid-19. Therefore there is likely to be higher demand for home loans in the future.

General

- The company paid salaries of all the employees on time—the high interest margin of the company (NIM) is important to successfully tackle the outlier events such as Covid. The company wants to maintain its NIM and therefore does not take loan from banks at high interest rates.

- Rating of the company is BBB, which can improve only after the loan book exceeds Rs 1000cr. GNPA is likely to improve, not worsen.

- Market size: Banks fund the Income Tax payers, who constitute 3-4% of the population. The market size is huge since all the others will get funds from NBFCs like SRG Housing Finance.

Future

- Loan book is Rs 260cr, much lower than Rs 350cr target for FY20. This is primarily due to lack of funding from the banks at the desired interest rates. However, the company will be able to complete this target in the current financial year FY21 since the liquidity problem has been solved. The company has also got funds of a total of Rs 75cr from NSB, SBI, and Union Bank in this quarter.

- The company is in expansion mode. It will be appropriate to talk about the details in the conference call after the next quarter.

Disclosure: Not invested.

1 Like

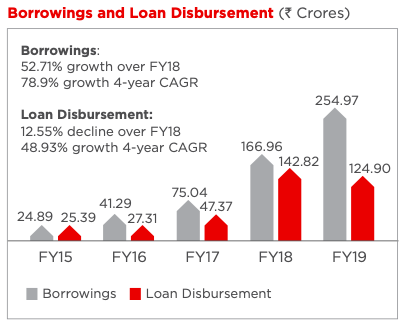

Why has it disbursed less amount of loan than its borrowing last year. It has been consistent before that but I couldn’t find a reason for their less number of loan disbursements that year compared to their borrowings. Any insights?

From the FY19 Annual Report:

Has the crisis impacted the

demand for housing loans? How

do we see the industry growing in

the next few years?Demand has never been an issue for the housing

finance industry; it continues to remain healthy

even today. The problem is that of the banks

getting more cautious to safeguard themselves and

thus refusing to lend. This paucity of funds rendered

many players unable to do business as they began

reserving cashflows for future repayments.

For us, the state elections in our target markets

followed by central elections led to slowdown. We

expect the demand return to normalcy during FY20

…

(emphasis added)

…

We have not disbursed any developer

loan during FY19 following our practice of smaller

ticket loans to retail individual units.

The above could be the reasons for lower disbursement in FY19.

The narrative about a rosy future and problems getting over in the FY19 Annual Report is the same as the narrative I felt in this week’s conference call. It is not a good sign if the company gives a rosy picture but misses its targets again and again. For FY19 (FY20) it set a target of Rs 325cr (Rs 425cr) loan book, but achieved around Rs 275 cr (Rs 270cr).

True @kalidasa. The biggest litmus test for me on this company will be to see if they can come close to 1000 cr loanbook vision for 2022 even after all the things that are going down in housing finance and NBFC slowdown. And if they can have their borrowing and disbursement in tandem to their historical performance by then. Also I don’t understand how state elections and central elections have led to a slowdown. While I am in favor of their low ticket size coupled with higher NIM, I am very sceptical about the other firms that the promoter has floated. Do you have any idea of the long term interest rates they may be borrowing at from sources other than banks? And what kind of time period are we looking for those kind of sources? @hitesh2710 sir, @ayushmit sir any insights on this one?

Disc - Invested a minutiae amount. Market valued it at 70cr then while its loanbook stands at 250cr.

1 Like

- In India, people don’t fund political parties out of their honest money. Funds are parked by political parties in real estate, which are sucked out of the system to finance poll campaigns – and the market faces a serious liquidity crunch during elections. Developers are more interested in clearing inventory than in starting new projects during this period.

- Buyers adopt a wait-and-watch approach in anticipation of election results (e.g., “stable” or “unstable”). The new government may bring new schemes, offers and policies which may or may not be conducive for investments. Another aspect of the elections’ impact on property market can be seen when infrastructure projects started by a previous government are shelved or stalled by the incoming party.

- Rural distress after demonetisation and GST could also have played a part in the slowdown.

Source: https://www.proptiger.com/guide/post/how-elections-impact-real-estate-markets

Source: https://housing.com/news/general-elections-indian-real-estate-adopts-a-wait-and-watch-approach/

4 Likes

Is anyone tracking this company? Numbers looks too good to be true. They have almost Nil write-off over the last decade. RoEs during this period has been around 20-25%. Growth has been subdued but is now picking up due to branch expansion.

But I am still not sure about the corporate governance part, because:

a) They had Delliote as their auditor in 2018-20, but now switched to a regional auditor

b) Many related party transactions (Promotor takes 3-4cr salary on 17-18cr PAT)

c) Promotor group owns the office premises in Udaipur, and the company pays ~2cr as rent. (in comparison rents for all 60 branches will be 3-4cr)

d) Promotor family has another business: SRG Securities (Listed) SRG Insurance; Though there are no related party transactions between them.

The thing that worries me more is, that the promotor is taking away ~5-6cr from the business (in Salary & Rent) out ~18cr PAT (20-25%).

Disclosure: Tracking positions (~1% of portfolio)

2 Likes

Earnings Conference Call: Q2 & H1FY24