Presentation

Can someone throw light on how rupee realization (USD) of Rs.70 is achieved?

Hi

I believe, you must be referring to “Forward Cover Realization” of Rs. 70 in FY18-Q1 for INR/USD on Pg 33 of the PPT.

In my limited understanding, it does not mean that they have realized INR 70 for every US$ of revenues during this Q. This just says that for the past hedges (i.e. forward cover), the average realization is Rs. 70 for this Q (which is entirely possible).

As per the company’ policy they cover 70% of 12 month rolling receivables - which as of FY18Q1 end stands between Rs. 67 - 70 (i.e. reflecting the INR depriciation). Ofcourse the forward cover for INR still goes on premia

Further the above can be seen in the light of the following comments (to rule out the possibility of any hanky-panky stuff) :

Company specifically mentioned that the margins has impacted in IITS due to INR moving from Rs. 64 from 68 on YoY and has also given a cautionary stance of further erosion in margins, if INR goes below 64. All this is captured under “forex income” under line item “Other Income” of the P&L.

Yep, i know the explanation is a bit confusing but hope it helps

Sonata has delivered an ROE of 35% in past three years and is trading at a 1 year forward PE of 10 and dividend yield of 6%

Earnings yield of 10% whereas GOI 10 year paper gives a post tax return of 4.5%

Not a typical services led IT company, growth is more from IP led verticals.

Classic undervaluation from Mr. market or value trap?

Decent Bet @ CMP , better placed than its peers as it has a defined niche market. How ever headwinds of Trump and World business environment is increasing business barriers and hence will impact margins in overseas market. They have a decent domestic business though with low margins which should help them stand the turbulence ahead. Markets do not like uncertainties and that is reflecting in current price. I would not go gung ho but will like to own a piece of it and add on corrections.

Hi,

It looks like that, Sonata is moving ahead in Platform based solutions quite well. IP- based revenue has grown by about 14% in FY17, and it may grow better over a period of next 4-6 quarters. Recent margin contraction may keep stock price under pressure for some time. We need to keep a watch on margins over next 2 quarters to see if they would start going up after few quarters since their investments in Sales force may get completed by that time.

With good dividend yield of > 5%, this is relatively better stock in small cap IT pack at the moment, when some IT services companies will face headwinds to grow, Sonata on low base can grow at over 20% in sales.

Disc: Invested.

concall updates

- adding more employees at back end for strengthening capability

- Mr .Vikas is added all customer facing global operations

- It services a good show , despite wage hike ? probably due to better utilization, not a clear answer given on this

- 11 cr other income is basically 10 cr from IT services and 1 cr from Domestic.

- 7cr out 11 cr is forex earning. However the management said these are real earnings . Not so clear about this?

- margins in IT service dependent on dollar , if dollar goes up margins follow.

- aim to have 60 more than 5 mn dollar clients by 2022.

- increased competition in retail or pricing pressure? - no such pricing pressure. we face competition but not from traditional Indian IT companies .

9.'Demand firm ’ used for account planning , strategising. - ability to win customers not a question ( added 10 new clients this quarter). - need to ensure 30-35 % stick with us atleast.

- embracing automation in our company through the platform of ’ Design Thinking’ . trained 300 ppl , plan to train all employees. its a 2 day program.

- converting customers into the long term account is the key.

13.converting a client into a bigger, account is about snatching a competitor’s share , transforming the clients business model to persuade him to use more of their IT services in his business and hope for the client to become bigger .

i might have missed some points , or written some incorrectly due to wrong understanidng. Please correct in that case and add your points .

Thanks

Disc- Invested

Good to see some additions in this forum recently after Q2 results.

Some more observations from Q2 results are :

The revenues from in-house developed intellectual property (i.e. IP-led revenues) increased to 15% of IT services revenue.

The company added 10 new clients in the quarter, 6 in the US and 4 in Asia Pacific.

Investments in domestic business are almost complete, and they have senior talent recruited in last few quarters to grow the business.

It seems that, Mr. Market has noticed improvements in OPM and re-rated the stock and the patience of holding it so far, seems to be paying off.

Need to see how they continue this improvement, and International Business growth in next 2-3 quarters. Dividend payout is helping investors in current tough IT scenario.

Some observations from Q3 results are:

In 9 months of FY18, Profit growth is about 14% which looks good.

The contribution of IP-led revenue to the total IT services revenue in the quarter was up from about 13% to 15.4% on a YoY basis. Digital revenues are around 32% of Total revenues.

Addition of 20 new clients in the FY18 seems in line with Management vision and strategy.

Overall, the patience of holding it through out 2016 and 2017 seems to be paying some benefits now.

Mind tree turning around, along with some improvements in Persistent and Sonata, has proved that, bottom up investing strategy is always better even though sector might be going through tough times. Eventually Good business will generate good returns.

Disc: Invested for over 2 years.

Sonata software AR 18 notes

• Creating a digital ecosystem platform called platformation

• According to a report by Couchbase, 87% of business leaders are concerned that their revenues would drop if they couldn’t uniquely improve their customer experience

• We are well positioned as a strategic partner of choice in the digital transformation journey of our customers and “redefining digital transformation – through PlatformationTM”.

• We continue to be recognized by the likes of Microsoft, SAP and Oracle as a valued strategic partner in this journey.

• Sales = 2435.94 cr ( 3 % yoy growth)

• EBITDA = 276.34 cr(16 % yoy growth)

• PAT = 192.53 cr (23 % yoy growth)

• RoCE = 30% ; ROE = 31%

• Finalized our new 32,000 SqFt. facility in Hyderabad as a part of our expansion plans

• Added 32 new customers for various products and solutions, including the addition of new logos across geographies and competencies

• International IT services (IITS)- 28 % PAT growth

• Domestic Products and Services (DPS). – 6 % PAT growth

• Company continued to invest in differentiated IP and platforms across industry verticals of Travel, Retail, Distribution and software solutions.

• International IT services contributed 38% of total revenues and 81% of PAT while Domestic products and services contributed to 62% of the total revenues and 19% of PAT.

• International IT total revenue – 928.5 cr. (13 % yoy growth).

• Your Company has achieved good results consistently because of its focus on serving and growing its existing customers, new customer additions of 32 throughout the Financial Year, and maintaining resource utilization at levels in excess of 85% over the Financial Year under review.

• Strong balance sheet with 509 cr of net cash

• Promoter holding stands at 30.95 % ( same as last year)

• Among top ten shareholders HDFC small cap fund is a major change , with current holding 3.53 % of company( zero last year)

• Managerial remuneration = 5.3 cr .( half of max as per ceiling act )

• Employee headcount – 3476 ( 3 % growth compared to last year)

• Receivable days – 57 (78 last year)

• Dividend- 10.5 per share ( 2.7 % dividend yield)

•

Hi,

It is good to see that, they have achieved PAT growth of > 20% with 3% headcount growth y-o-y.

Receivable days have reduced in tough conditions of FY2017-18.

If International sales can continue to grow at the current rate and contribute more, the business may improve further.

Good dividend yield adds stability to the stock, in general.

We need to see whether ROE improvement will continue further or it has reached a point of saturation.

Disc: Invested.

Came across this latest news … thought to share

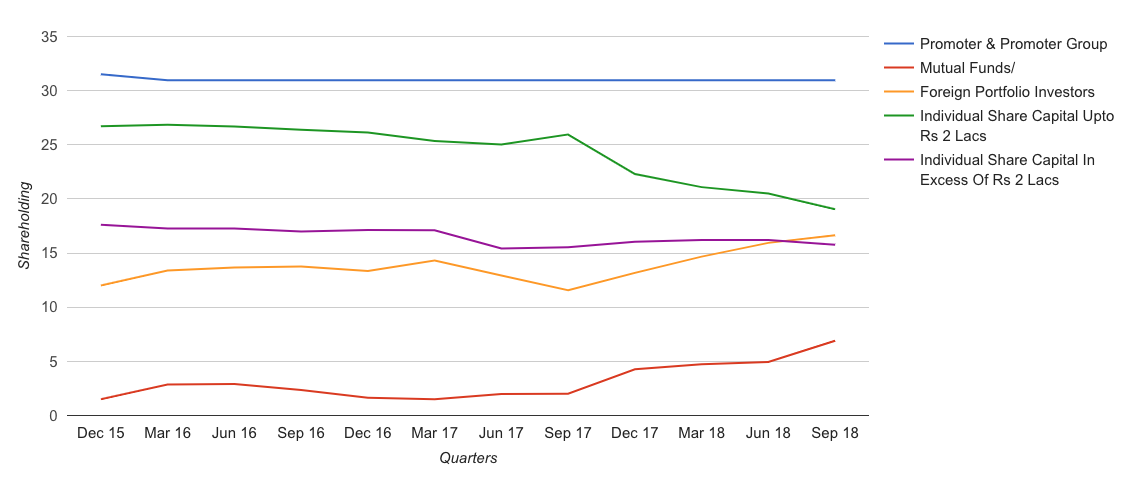

Looks like retail holding has gone down from 27% to 19% in the last 12 quarters. In the same period Mutual Funds and FPI have increased stake from 1.5% to 6.91% and 12% to 17% respectively. Maybe that’s why the activity here has reduced? ![]()

More details on SHP here, if you are interested - https://phreakonomics.in/shareholding/index/SONATSOFTW

The dividend yield of 3.76% and RoE of 30% or thereabouts for the last 4 years is quite attractive. Perhaps about 10-15% expensive based on historical median P/E but if the coming quarter is good and with a dividend around the corner, not a bad time to build a position.

Disc: Investing/Tracking

Sonata Software Ltd

Highlights Of Q1FY19 and H1FY19 Results

Financials

- Revenue grew by 8 % to 593 Cr over last year same quarter

- PAT grew by 37 % to 62.2 Cr over last year same quarter

- ROC stands at 35% and RONW at 36%.

-

Segmental Performance

- IT Services Segment

- Revenue stood at 275.3 Cr which has grown by 7 % QOQ and 17 % on YOY basis.

- This contribute about 46 % of consolidated revenues.

- Revenue in dollar term stood at 39.1 million which is sequential growth of 3.3%. In INR revenue growth of 7% and USD growth in constant currency of 4%.

- Digital component revenue stood at 35 %.

- IP led revenues currently stand at 18 % of current revenues so that grew from 16.3 % last quarter.

- EBITDA stood at 26.7 % sequential grew by 10 %.

- Company added 10-11 new clients which are from North America, Europe and Asia.

- Domestic Product and Services

- PAT stood at 11 Cr grew by 6 % QOQ and 31 % YOY.

- ROC and RONW both stood at 25-26 %.

- IT Services Segment

Key Highlights

- On international service business company grew by 3 % on dollar terms and 4 % on constant currency. Company have seen growth in some of large existing clients and also added some new clients last quarter. Europe has been relatively growing faster than the rest of the other geographies.

- Company has been inducted into what Microsoft calls its Inner Circle members for dynamic focus which has been both organic and inorganic in the dynamic space has now brought company into one of the Inner Circle members which is about 30-40 partners worldwide. So company will leverage that alliance for accessing new clients.

Q&A

- What led the revenue subdued in infra management business from last couple of quarters is there any impact from digital disruption , how are things shaping up on that front ?

- At a high level it is an industry trend, there is a shift from on-prem to cloud. Company large part of revenue is from cloud rather than from on-prem . So that shift will continue to take place in the industry. It is an inevitable shift which is going to be happening and how that finally falls out in terms of what are the service components of this shift. For newer players it is a big opportunity.

- Will the subdued side will continue on the IMS side ?

- It is a function of the movement to the cloud and most of clients of company are seeing embarked on it. So as they do more of it , company will see a higher percentage going forward. At a high level infrastructure is not a leading service for company.

- How is the progress in the analyst meet that company had earlier this year ? How is progress at the moment in terms of client interest, be it current existing clients and the new clients and any interesting activities is there on this front that could lead to record improved revenues growth going forward also ?

- There is lot of interest and actions is coming from both side. A lot of good has been with existing clients and marginally with completely new clients with Platformation as a leading service. Company have seen a lot more traction in terms of conducting of workshops with the top management teams. Even company alliance partners want to work with company to engage in their digital transformation initiatives. So that they also have a fairly unique value proposition when they talk about digital transformation. So company is seeing lot of interest.

- Why company T&M is high compare to others ?

- This is nature of business company do not have any preference. It is client fixed price and T&M. It is a kind of value proposition. Value comes from what service company deliver , pricing and T&M are the secondary factors. Company focus is still to be very heavily differentiated on the service that company offer and what value company brings to customers . Focus will be on margins whether it is a T&M or Fixed price.

- What are the IT services margin for the quarter after adjusting FOREX gains and other income ?

- On EBITDA basis it is 26.7 %. After Other income and FOREX it is 22.4%. Company is at 22.5-23 % excluding FOREX and other income.

- What amount of cash company generated in first half of this year ?

- Company have about 360 Cr cash available. That is after dividend that company has paid.

- Cash flow from operation will be about 130 Cr.

- What led travel vertical revenue grew strongly ?

- A lot of it has been led by growth in the large clients from some interesting new clients in that space. It is a mix of both. About 2-3 clients who are looking extremely promising in that vertical in terms of growth and these are fairly big names they all are in Europe and some are in Asia. It has been driven by both the growth in the large client and some very interesting large new clients that company has acquired in Europe .

- What led to decline the others component sharply ?

- Company focus is on key verticals. Others as the percentage will decrease but that is because company focus is on the 3, 4 verticals.

- There is good growth in IP-led revenue since last 6-7 quarters . So, considering the current run rate, the IP led portfolio revenue is around 28 million, So what scope company can see in that portfolio as company have 6 IIPs, so can it be 50 to 60 million portfolio like in the next 2 to 3 years?

- Company get client from its IP and company do services for them. It is not licenses of IP and that will be less than 5%. So that will be company strategy which has been the 3-point strategy which is Platformation-led, IP-led and alliance-led. So IP is a very strong differentiator for company to go and get new clients. Company expect this number to be 50-60 million in 2-3 years.

- Which are the top IPs that company have ?

- Most of the IPs which are doing well all dynamic-led IPs which is the Brick & Click, the Kartopia and the modern distribution, Rezopia from the channel perspective and Halosys. The one which has still not got very strong traction in the market is the rapid DevOps, CloudOps platform. So that is still in the phase of getting some traction. So otherwise each of them obviously serve a different purpose in the client’s value footprint . so that continuous to be as differentiation growth in clients and with company alliance partners work with clients because in the market because of the IP company have in the industry which are they are interesting in.

- Kindly share IBIS, Halosys turnover and EBITDA for the quarter and Rezopia?

- Halosys and Rezopia are not operating entities anymore although they exist as companies, the business gets done through Sonata 100%.

- In IBIS company had a turnover of $ 2.2-2.3 million and EBITDA was about 18 %.

- What is the other segment of company vertical ?

- Healthcare companies , Insurance Companies and some financial services company.

- How significant will be the relationship with Microsoft ?

- It is very significant. Company is 1 % of the partner globally. So out of 30-40 company is one. So it is one out of 2 probably from India . Other is an acquisition which an Indian company made. So, that is why company is very prestigious and it give access to market access to the leadership of Microsoft. This is selected based on customer adds, IP company have ability to deliver value, successful delivery of projects, that is all metrics which they use before they choose these partners. So it is very prestigious. As company had invested long way as a result seeing good attraction. Microsoft is doing extremely well. They have had the first $1 billion last quarter for Dynamics, first time ever. So they are growing at 50% to 60% in the Dynamic business so it is delivered.

- How is the business panning out in Europe region ?

- Yes company have grown relatively better in numbers, 25% growth in Europe on the first half is the correct number. Company has acquired new clients also. Company is operating in UK, Nordics and Switzerland .

- How is the pipeline looking for particularly IP-led revenue? How is the pipeline for this for next second half?

- Pipeline is very good and it has never been as healthy as of now.

- What were the company other income and FOREX gain for this quarter?

- Overall EBITDA is about 26.7%and stripping it off with FOREX and other income is 22.4%. So roughly about 2.3%is FOREX and 2.1% is other income. That brings a drop from 26.7% to 22.4%.

- On margin front where are the head winds and tailwinds in the IT services ?

- Overall company is growing. There is a small change in onsite-offshore mix. The headwinds came in from the cross currency effects and also headwind is a part of normal operations but in the hindsight company take care of it. There is some investment that company had made in the management overseas. so these were a little bit of cost upside and positive was obviously the FOREX as utilization increase.

- In BPS terms , How it moved from margin to margin from Q-o-Q basis?

- In last 3 quarters , EBITDA without other income and without FOREX has actually moved from 18% in Q2 FY18 to 21.1%, 20.9%, 23.5% and roughly about 22.4%this time. So on overall basis EBITDA in percentage terms was 39.4 %.

- Does company hedge more of its revenues ?

- Cover is in range of 69-70 %.

great set of results

PAT at 64 cr ; 30 % yoy growth

international it services is going strong. it has shown a revnue growth of 18 % yoy while the ebitda growth has been 34 % yoy in this division. this has been due to increase in margins to 30 % in this segment.

domestic business has also given decent numbers with an ebitda growth of 10 %.

Disc - Invested

Great results. The only thing we must bear in mind, is to keep the future growth projections at ~15% at best, as about 10% PAT growth is aided by rupee depreciation.

Disc: Invested

Regards

SJ

great set of results

revenue

international services grow by 18 % yoy from 257 cr to 304 cr.

domestic product grow 31 % yoy from 437 cr to 574 cr.

consolidated revenue growth at 27 % yoy.

EBITDA growth at 106 cr vs 83 cr last year. ( 28 % yoy)

PAT growth at 16 % yoy - from 57.6 cr to 67.1 cr. ( 16 % yoy ), on account of higher finance cost and depreciation.

So here we have a company available at 13 P/E , cheaper than the industry average ; at an attractive 4 % dividend yield, net cash of 400 cr on the Balance sheet , showing great growth consistently in both its business divisions. Management commentary is very optimistic about the future growth prospects., great return ratios - upward of 30 %.

Disc- Invested

Good set of Q2 numbers)Link

Revenues grew by 19%, PAT grew by 16%. Interim dividend of 5.75 per share declared.

Story continues as expected.

Disclosure: Invested

any specific reason for decline in revenue (yoy)…