Things definitely weren’t as bad as the market reaction.

1 Like

Cash flow is very less compared to Operating profit because more than 50% of profit it stuck in Inventory and receivable. Is this something worrisome ?

4 Likes

Got approval for Karnataka.

Waiting for clarity on IT raid, and trend should resume.

3 Likes

Wondering why the RAID has been done in those states where there were election. No clarity on if anything found or not.

1 Like

Sometimes, no news can be good news. What are you expecting to hear from company or the media? That nothing significant was found?

Company would have needed to inform exchange, and there would be news in paper that oh 100 crores black money recovered etc. to create hype, in case of any major findings.

Don’t be worried of your investments, set up alerts on screener, and take decision accordingly. Let’s not speculate anything.

2 Likes

6 Likes

what are the reasons for the low PE multiple? Radico with flat growth now trades at nearly 100x TTM earnings.

I’d say that this company’s promoter’s are always under the radar of the government.

2 Likes

Good Results posted - ‘Som Distilleries and Breweries Limited

4 Likes

Management Target : 2000 Cr Top line in next 2 Years.

4 Likes

It can’t possibly be because of a dividend. For 10k shares, even a 5 rupee dividend is 50k - that’s peanuts for Mr. J K.

I believe its market signaling. They’re getting a far lower PE than both brewery comps as well as IMFL players, largely because it seems people don’t trust the management.

I would strongly recommend people read this. Growth aspirations aside, the management and corporate structure raises many red flags.

Not saying you are right/wrong…just brainstorming…

Let’s assume the management isn’t reliable (I partially agree too) as they have already had a visit to the jail in 2020 but this isn’t something new right? If so, why did the stock rally non-stop from March 22 (Rs.40) to Oct 23 (Rs.390)? Let’s say the IT raid played a speed breaker but in the end, nothing wrong was found. I think the continuous fall in stock prices is due to retail funds moving toward hot sectors like railways, solar, etc… the promoter is buying (let aside the warrant) maybe he sees something that we aren’t seeing.

3 Likes

that was due to preference shares allotment.

Don’t use profanity while expressing your views, even if you believe they are the right words. The intention to warn members is appreciated, but do that without using the bad words.

Sorry, I didn’t mean to be profane. Apologies. You’re right, I could have expressed myself better.

3 Likes

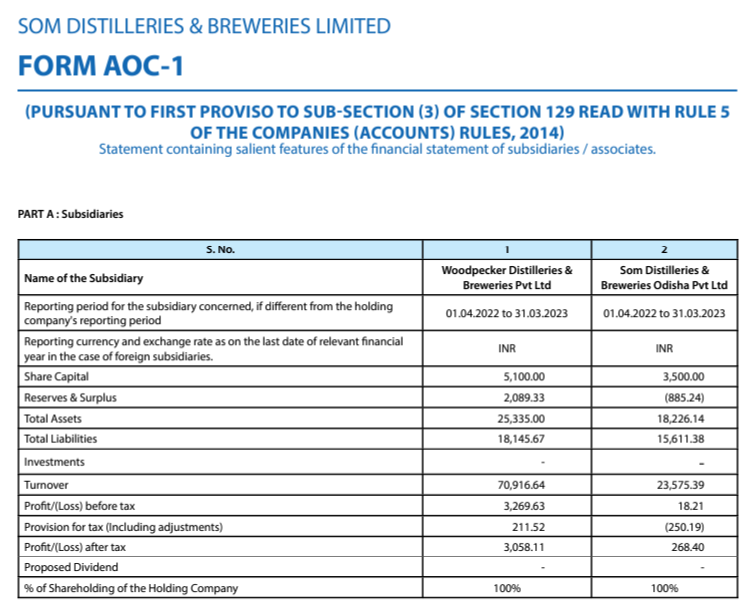

Today, the company has come out with the notification that Woodpecker Distilleries has become subsididary instead of Wholly owned subsidiary. While the Promoters have infused equity in the subsidiary which is a welcome step as the business needs funds to grow at 50-60% rates, I am a bit surprised by the valuations.

The subsidiary did 262 crores of revenue in FY23 (32.50%) and promoters have taken 21% equity in the subsidiary for 30 crores. It means the whole subsidiary is valued at 142 crores i.e. Subsidiary is valued at roughly 0.5x sales.

While I haven’t seen the subsidiaries’ financials separately, I don’t think it is fairly valued at 0.5x sales. The promoters do bring a lot of knowledge in the company and may deserve some discount but it looks like a very steep discount given that currently, the company is valued at 2x sales in the open market.

Also, doesn’t the company need to get this proposal approved from the shareholders? Can someone please throw some more light on this?

3 Likes

I did some further digging and found below information in the FY23 Annual report of the company. Company had posted 60 crores of profit in FY23, 50% of it came from the subsidiary ‘Woodpecker Distilleries & Breweries Pvt Ltd’ (shown below). 21% of this subsidiary has now been taken by the promoter for meagre 30 crores. It means they have valued the subsidiary at PE of less than 5.

If this is not day light stealing then I don’t know what is. As per them, the whole company should be valued at 280 crores and not 2000 crores (current market cap). I still believe that the promoters should get some discount while raising such capital, but this is not looking good. The shareholders have suddenly lost 10% of annual earnings (20% of profit generated by the subsidiary) in return of 1.5% equity value (30 crores for a market cap of 2000 crores).

7 Likes