Going to start supplying beer in Rajasthan as well.

4 Likes

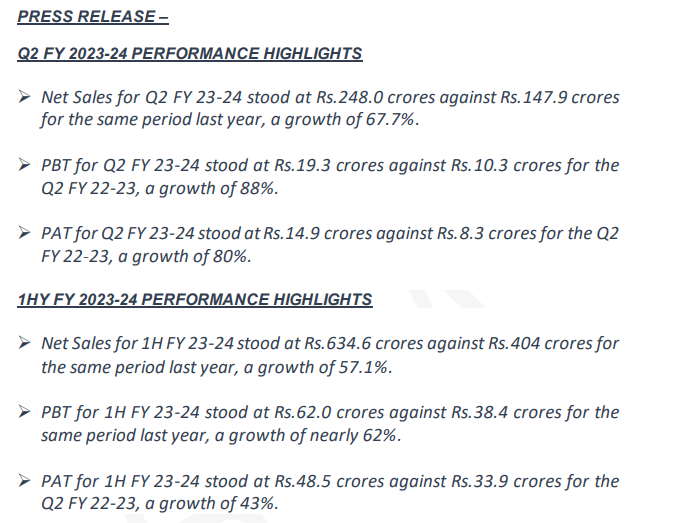

This quarter consolidated net sales of 386cr up 50% YOY and PAT of 33.65cr up 31% on a YOY basis.

3 Likes

Q1FY24

Revenue grew by 73% YoY and 57% QoQ to Rs7,586 mn on robust volume growth.

EBITDA grew by 42% YoY and 72% QoQ to Rs485 mn. EBITDA margin fell by 140 bps YoY while it was up by 57bps QoQ to 6.4%

Net profit grew by 31% YoY and 112% QoQ to Rs337 mn

5 Likes

We are pleased to announce that we have placed the orders for the expansion of the beer facility

at our Hassan plant. The orders have been placed with suppliers based out of Germany and

India. This additional expansion will add another 60 lakh cases per annum from the plant.

Pumping up the total capacity to 1.5 Crore cases/annum which further assists the company to take up contract manufacturing orders.

4 Likes

3 Likes

Promoters increase shareholding as they guide immense growth going ahead, The last con call/presentation was a confidence booster as really positive numbers have started showing up and plants are running at 110% capacity utilization combined with ongoing capacity expansion.

3 Likes

The company informs the stock exchanges that their beer brands have received

permissions for supply to the state of Chhattisgarh. They have also started the initial

dispatches to the state.

6 Likes

The promoter continues to increase his share in the company gradually.

Can anyone help me with the excise duty that a company pay to state govt if they have manufacturing facility in the state vs outside the state ?

i am trying to see how much impact they can make in raj and Chhattisgarh. Also, any news of any acquisition in any state.

Skip to 14th min for the interview with Mr.Jagdish Arora. https://www.youtube.com/watch?v=E5uMIG4TDdg

Mgmt. spoke about aspirational targets of growing 10x in next 6-7 years !! First requirement for growth is aspiration ?

Som is now in 4th place in the overall beer market (behind UB+Heinkein, Budweiser, Calrsberg) even though their geographical presence is limited to only few states. it’s the fastest growing beer brand in last 2-3 years. Wherever they are present, they are no.2 and have gained market share over last few years. They have eyes set on large potential markets like MH, RJ, UP, Telengana, Andhra, TN, which all are 30mn+ cases market.

Capacity : Already using 100% in MP, 110% in Karnataka, Odisha completed capex in July but utilizing >50% (also had tie up with Carlsberg which will take utilization to 100%). Beer as a product is viable mainly with local state production. Possible only via acquisition or greenfield. UP - Planning a greenfield (6th largest country in the world in terms of market size !!)

Debt : Reduced from 250 to 150 cr. QIP coming in this month for 350 cr.

Margins: Raw material - Malt (impacted as it comes from Ukraine), Packaging material was impacted due to HNG (Produced 70% of glass bottles for beer industry) went into NCLT. So price increases taken will stay, raw material pressure will ease, profitability will increase. Plus operating leverage from capacity utilization.

Market Size : 370 Mn cases all India. Som has sold around 15Mn cases in FY23. Total 400 Mn cases market estimate for FY24. Our market share is 12% in the markets Som is present. In 5-6 years this 400 Mn market will increase 700-800 Mn cases. Assuming we can get 20% market share on all India basis in this time, we can be a 10,000 cr. revenue company in 5-6 years.

Disc: Invested and transaction in last month

15 Likes

SDBL -

We are pleased to announce a strategic contract manufacturing arrangement for our brands

in Punjab aimed at bolstering our supply capabilities to the Canteen Stores Department

(CSD) for the Northern region of the country. This partnership marks a significant milestone

in our commitment to provide high-quality products to the armed forces and veterans across

the country.

If company giving such big targets why would they not get money from investor’s in QIP? Is it a big red flag?

Maybe because all institutional investors are currently seeing small caps as overvalued and to be honest they somewhere are but not as bad as they are making it look. Growth lies ahead and numbers are enough evidence. What I feel went wrong is the timing to raise funds and a high floor price, these guys are trying to raise funds when institutional investors plan on selling their existing holdings.

1 Like

As fund raising is cancelled this could impact to future expansion.

1 Like

exactly either that or they’ll have to take debt

any why not rights ? Their last rights which came at 140 was very lucrative. I think by the time allocations came stock was already close to 180-190 and retail got super allocation on top of their eligibility. My initial allocation to the stock was at around 50 with a view to participate in rights which had come at 40. So i would pray for yet another well priced rights. Mgmt. has been looking to raise their holding, a discounted price compared to market price helps them too to raise their holding.

1 Like

Interview after Withdrawing QIP

2 Likes

QonQ is not a good result profit down by 50% which is not good sign - i may be wrong,

Q1 is always heavy for them as beer consumption is highest in that quarter. So the comparison is not valid.

Regards,

Raj