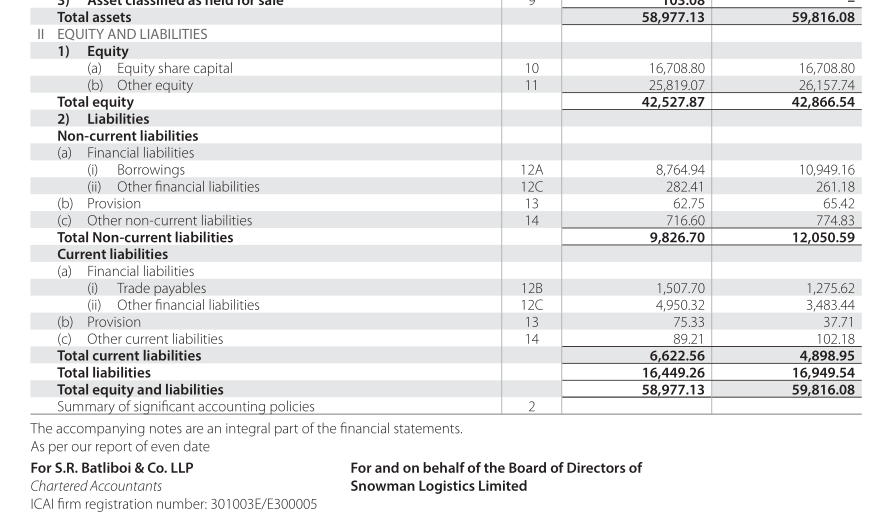

If you want you check whether depreciation is legit, then compare it as a % of fixed assets, as per AR FY18, Depreciation charge was 40 cr, on gross and net FA of 515 cr and 447 cr at the start of FY18. So depreciation as a % of FA comes to about 10% which means FA are being depreciated over 10 years approximately.

If you read the accounting notes further you can what accounting policies w.r.t. D&A they follow.

So, D&A as a % of sales does not reveal much about whether accounting rules are being followed, at best it reveals how current operations are doing and whether the business is capital intensive.

Since, D&A is removed for CFO calculation it may give you the illusion that the company is generating cash, but if you were to calculate FCF which takes into account the maintenance CAPEX you would see why the said +ve CFO is ploughed back into the business with no major effect of Cash, investments, FA, Reserves or debt.

As per Q1 results, the company has increased Transportation services assets by 6 Cr. They were trying to reduce this side of the business for sometime. This area of business was loss making for sometime now and it keeps increasing Q on Q. So, found it interesting that they decided to increase the assets when fuel prices are sky high.

As per AR, they are running at 88% capacity, with 25% warehouses at 100%. This would mean that they have to add capacity to increase sales. So it’s highly likely that they will borrow more money, which will results in higher interest cost and hence lower PAT.

Trade Receivables increased substantially, and now is almost 20 - 25% of Turnover.

Extrapolating Q1 performance to the rest of the year, with 20% growth, gives a forward PE of 100+ even at current market price. Even at the current price, the stock seems expensive.

Hi Ranjit, if you don’t mind, can you briefly explain your rational for investment in snowman? From your post your conclusion is that snowman is still expensive even at current price with more investments needed to grow revenues.

I bought it last year @ Rs 50 average. I was excited about the prospects of GST and Snowman being the largest cold storage co in India. I assumed some form of consolidation/M&A.

I see continuous improvements Q on Q for the last few qtrs. Trying to figure out a good price to average. In my view, If they don’t add any new assets and use the cash to pay down debt, by FY20, the share will have a reasonable PE, just with the reduction in interest costs and depreciation. If they can turn around the transport business, that would be a plus.

Ranjit same here, have been tracking this stock for 3 years now. Its a great sector to be in, and Snowman has market leadership. They kind of restructured the business last year, downsized the transport business (The business is more of add-on than being a core service), took write-offs for past investments, inventories etc. This was all timed during GST.

Snowman has seen consistent improvement in sales and EBITDA, but still struggles at PBT, PAT level. I have remained in the sidelines till date, but actively tracking the stock. My only worry is that, at Quarterly revenue run-rate of Rs 55 CR/ Annual 220 Cr, the current MCap is 3x Revenue, which seems to be a bit high.

Did the shareholders of Gateway distriparks got the shares of snowman logistics earlier when it was listed? Just asking as my friend is having gateway distriparks from last 10 years and gdl being promoter company and he has not received it. He somehow forgot that investment.

Adani Logistics will make a mandatory open offer as per the Substantial Acquisition of Shares and Takeover Guidelines, 2011 for a maximum 26 percent of the public shareholding in the Snowman Logistics.

Can anyone explain how the open offer works? Adani has announce the open offer for 26 % of the public shares, Adani has to buy the whole 26% or its upto them how much they want to?

Go to

Outcome of Board Meeting held on Jan 21, 2020 at INVESTOR RELATION - Snowman

in the link file go to page 4 note 5 :— so the deal is already on the place Adani will not make any open offer

How does this effect the Snow man : It will able to expand further it’s capacity if promotor wish to but the overall control may be change of Batten // or current Unpledged promoter holding: is 40.25 % if adani get than the control will be at par with Promoter …

Regards

disc: in watch list not bought and this is not any recommendation for sell or buy i am not any sebi approved analyst