Sintex textiles able to use the brand of Sintex which is originally a plastics company.

There is some value definitely for Sintex brand, but what price one should attribute to that is a question. On the other way to say book value lower by 1500cr means, zero value attributed to Sintex brand.

Imagine, instead of Sintex brand, if they had to use some new name with the just 2-year-old history of business means, how the market and customers perceive such a company?

@Prash

I am genuinely sorry, but you got it wrong like what I did initially. The 1500 crores is actually on the books of Sintex Plastics.

At the same time I will request the admin @Donald to lock this thread, as there are independent threads available for the two companies that have come into existence after demerger. That is the only way to avoid such confusion. Members can be requested to use those threads.

While many folks knew the shady nature of the promoter. One well known analyst kept recommending it as great value buy who otherwise gives fraud certificate to companies pretty generously.

I have no interest here neither I understand issues fully.

I would not jump to any conclusions just yet. Let’s examine a few facts:

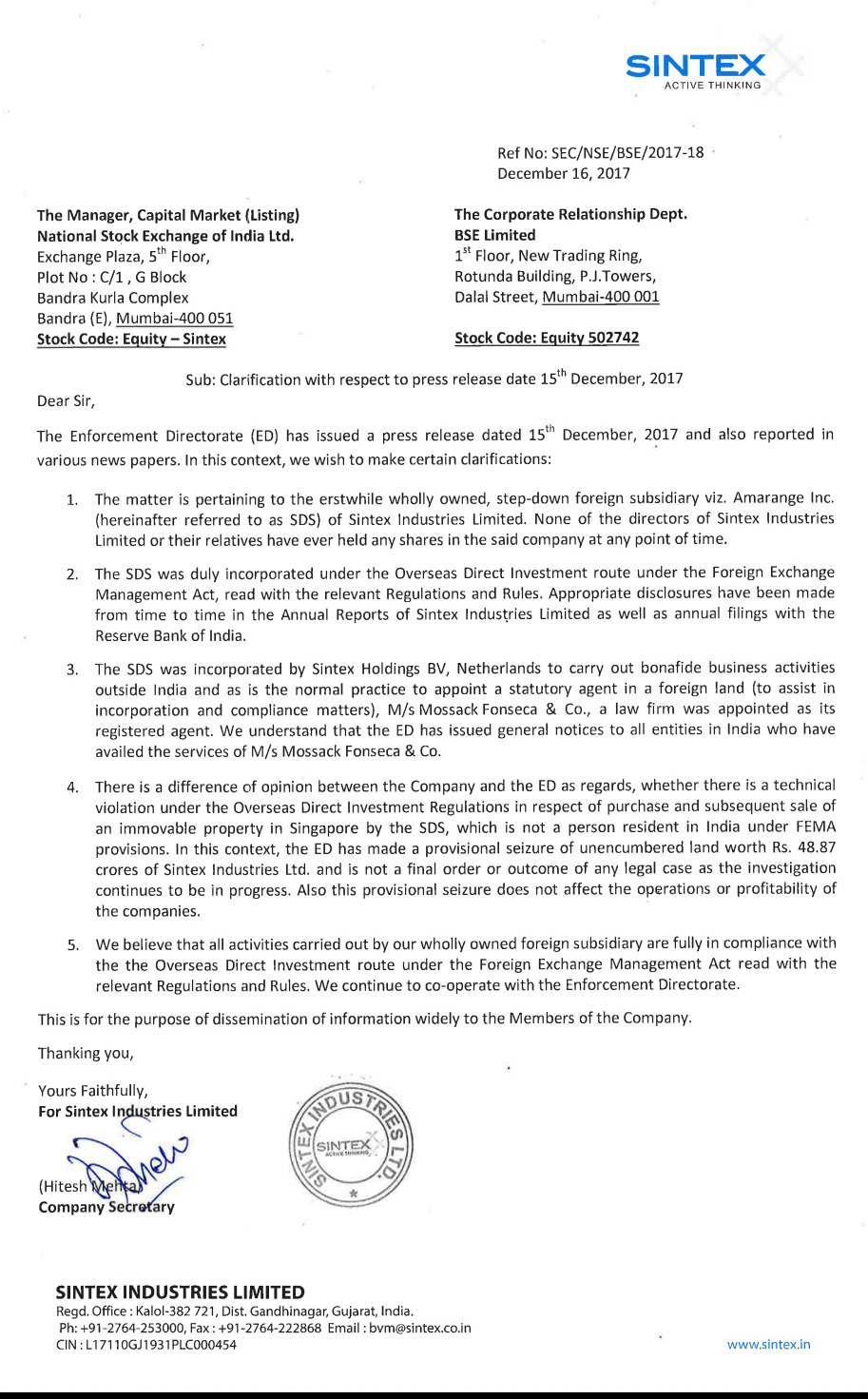

Both the subsidiaries in question - Sintex Holding BV and Amarange Inc. - were transferred from Sintex Industries to Sintex Plastics (SPTL) as part of the demerger scheme. The latest FY2017 ARs of both the Sintex companies clearly show that Sintex Holding BV and Amarange Inc. are now owned by SPTL. If the assets of both these subsidiaries are part of SPTL, so should be the liability arising out of this case (if any). So, the impact on Sintex Industries should be nil in my view (though it doesn’t answer as to why did the ED attach assets of Sintex Industries and not SPTL).

The AR of SPTL states that Sintex Holding BV and Amarange Inc. are Investment Vehicles, and not operating subsidiaries. So, by buying and selling properties, I am not sure if they have violated any norm since they are meant to be investment vehicles. What I do not know is to what are the timeline/guideline around reparation of dividend/profits from such investment back to India. Can any legal/accounting/FEMA expert please throw some light on this?**

This issue came up earlier as well in 2016, and the management (Rahul Patel) said: "We have about 21 plants outside India. We acquired this (Amarange Inc) in 2007. While we acquire international operations, we need to create holding companies. When you acquire a company, you need to hold it outside India and then repatriate the dividends to India. So it is done with RBI permission and guidelines. We also borrow money there and we also send money outside India to fund our acquisition and we also get dividends from those companies into India. It (Amarange Inc) is part of our balance sheets and we also disclose (information about) it in our balance sheets since 2007. We keep on creating and closing these companies as and when the acquisition opportunities arise.”

Overall, let’s wait for the company to present their side. In the meanwhile, if any expert can throw some light on point above, then that would be greatly appreciated.

Regards,

Ankit

Disclosure: Invested in both Sintex Industries and SPTL.

That makes one wonder about the depth of investigation that has been carried out by ED over the last two years.

This is normal for ED to make tall claims which most of the time fail in the courts.

You may be right but attachment order comes only after it is established that wrongdoing has happened or they failed to respond. I don’t understand why ordinary investors should stay put to find out how honest these guys are. Not every textile promoter has been named in these papers. I think you must be aware that primary purpose of entities in Panama was to evade taxes. Leaving aside these alleged tax evasions, can you please point out what makes you think that the promoters will create wealth for investors?

I don’t quite agree. Attachment order is pretty common precautionary measure used by ED and not an establishment of wrongdoing. Kindly don’t mislead. Also attachment means the asset cannot be sold till the attachment is released by itself or due to court intervention. It doesn’t impact day-to-day operations related to the asset. Also the amount involved is pretty small (don’t remember exactly but I think it is around 3-5 M $). So not a big deal considering the size of the company

So ED roams around the street and attaches the property on a random basis as a precautionary measure? I was trying to say that when ED (internally) establishes that prima facie wrongdoing has been done so action has been taken. Obviously they have to prove it and even if they don’t investors have enough ammunition to remain skeptical. Why on earth, a company has to go to Panama to set up a tax dodging operations.

Brother, this is Panama files. No one went to Panama. It is a holding company incorporated in Singapore. FYI. And I don’t want to education on how ED operates. They do attach assets to protect investor’s money. Its almost like a collateral. Anyways, you have entitled to your opinion

There are millions of companies in places like Panama, BVI, Cayman islands. Many of them are owned by Indians or have Indians as Directors. Not all companies are made for money laundering or tax evasion as people generally believe. In many cases it is for genuine purpose like preserving ownership or to legally avoid taxes by taking advantage of tax treaties or for Group structuring.

In this case, avoid commenting on just newspaper report and Company’s clarification as we do not have sufficient details to form any view. It maybe to siphon off money or it may be as a genuine transaction, we have no means to know. If you think this incident affects your conviction then move out or write to company for specific details of the transaction.

This company got sales tax benefits for investments, got low interest rates on debt and still shops for more tax relief through dubious (legal or illegal) means. I rest my case but I have not heard good feedback about promoters. Don’t understand why investors are running around this company which has thoroughly disappointed for a long time and continues to indulge in questionable transactions. If everything is fine, they should have approached ED on proactive basis to clear their name. The stock could still run on "chor bane more " theme though. Sorry, this is my last one on this.

Thanks! Any improvement in the fundamentals expected?

I had read that sintex is getting loans at a very low interest rate (2%) under some textile scheme of the Gujarat government. Should this not be positive for sintex?

The trading arm WOS BVM Overseas - trading yarn at very little or no mark up. My assumption is that sole motive of its existence is to fulfill the obligation to export 2K Cr + of goods to avail duty free import of machinery. Therefore, it’s only worthwhile to look at the turnover of the standalone entity. So compared to Q4 FY18, in Q1 FY19, turnover increase is only ~10%.

As per AR2018, there is still 2K Cr+ of CWIP even though all 600K spindles are live.

They have deferred tax liability of 80 odd Cr which they will have to pay out. One of the reason for lower PAT in Q1. This might continue over the course of the year?

Unabsorbed depreciation of 200Cr + is already on the books. They might have to book it sometime in the future? This will only increase going forward and might keep the PAT low for a long time, even though EBITDA might grow substantially.

There is also this, “Difference between book and tax depreciation” - which is above 560 Cr. I’m assuming this will have some impact on the PAT in the future.

In my view, the only positive here is that they might generate good cash, which they should ideally use to reduce debt quickly. That would help them improve PAT and the share price.

.

.