Update on commencement of operations at our new plant (Unit 5) at D-10, MIDC Lote Parshuram,

Ratnagiri, Maharashtra.

5 Likes

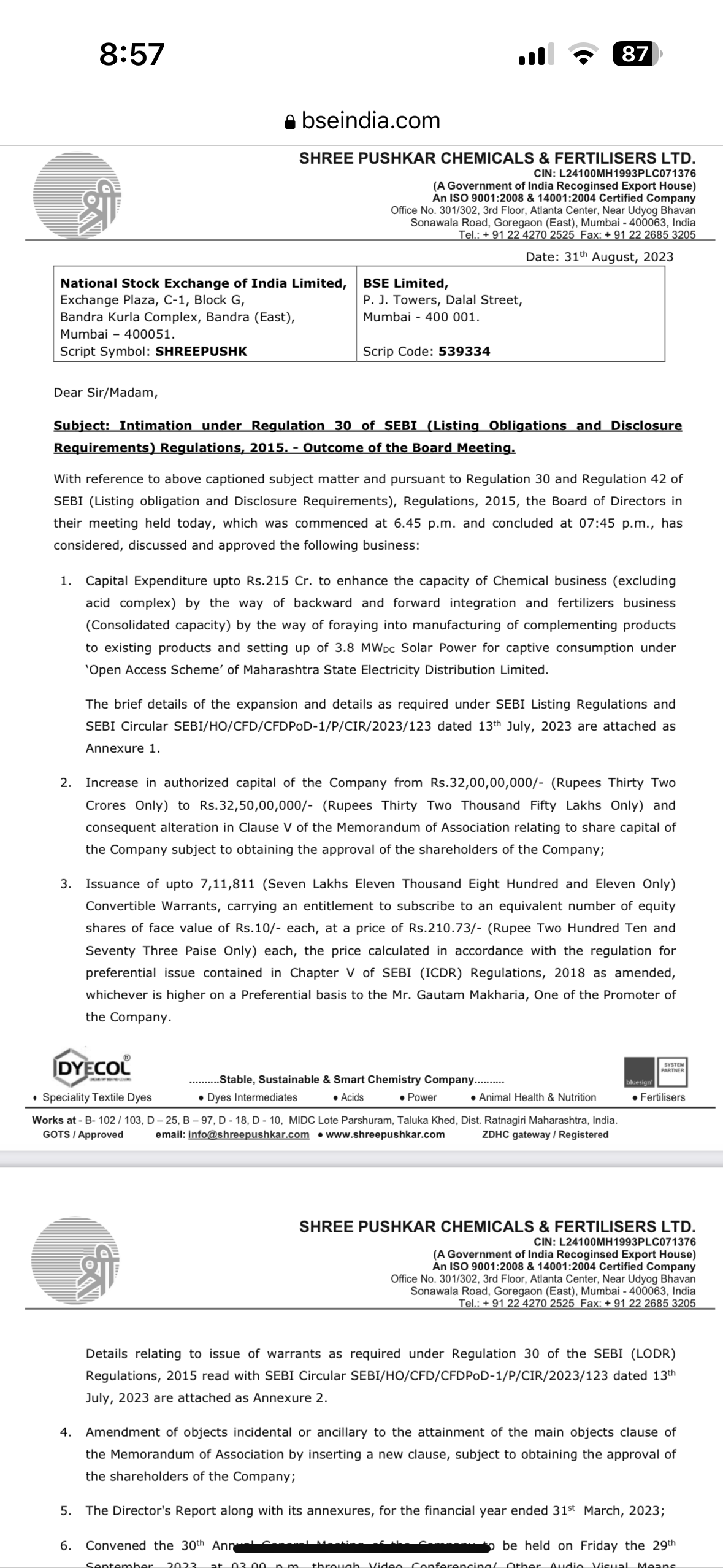

Mr. Punit Makharia has been issued preferential shares @ a rate of INR 190 per share (CMP INR 255). Any reason for such a steep discount?

2 Likes

its conversion of warrants issued earlier in aiug-21 when stock was at same level.

5 Likes

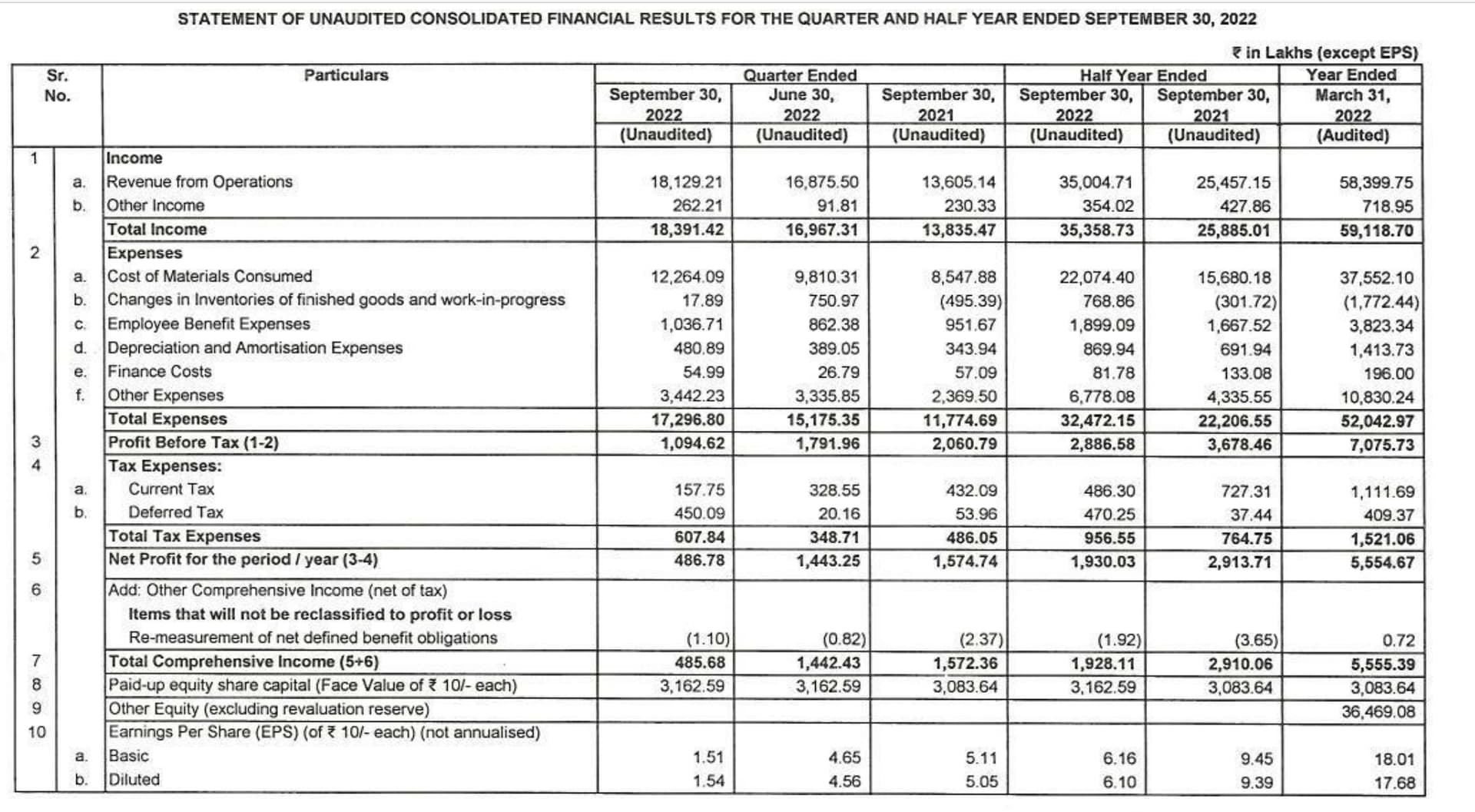

Q2 Results announced. Doesn’t look good. Sales up 32% but PAT down 70% approx.

Anyone tracking this stock closely knows the reason for such a rise in cost and downfall in margins.

Please share your views on Q2 results.

3 Likes

As per the con call the management was pessimistic on the dyes business. The MD was attributing the lacklustre performance to Bangladesh financial issues ( them being biggies in textile ) and Ukraine war. While the subsidiaries Madhva Bharat, Kissan etc has done well in fertiliser business the drag is from dye stuff. He said this can go on for couple of quarters.

2 Likes

If you look at the results and concall there is one time deferd tax.

Management comentry is chemical business will suffer for few more quarters but fertilizer business is intact for atleast 2 quarters.

1 Like

https://www.icra.in/Rationale/ShowRationaleReport?Id=118667

As per the credit report the Dewanganj plant appears to have commenced operations in Q4 FY 23.

3 Likes

Thoughts post Concall Q4FY23

FY24 Outlook: Year of Consolidation

Makaria ji says FY24 rev could be 900cr.

he isnt very optimistic on the bottomline improvement though.

Assuming 10% margins same as this year.

Am expecting PAT of 55-60cr.

Track:

- Improvements in chemical numbers

- Ramping up of Dewanganj plant.

- Ramping up of Unit V which has a potential of 200-250cr. in year. (This year 16.5cr revenue was clocked in Q4 )

Disclosure: Invested from lower levels. No recent transactions.

5 Likes

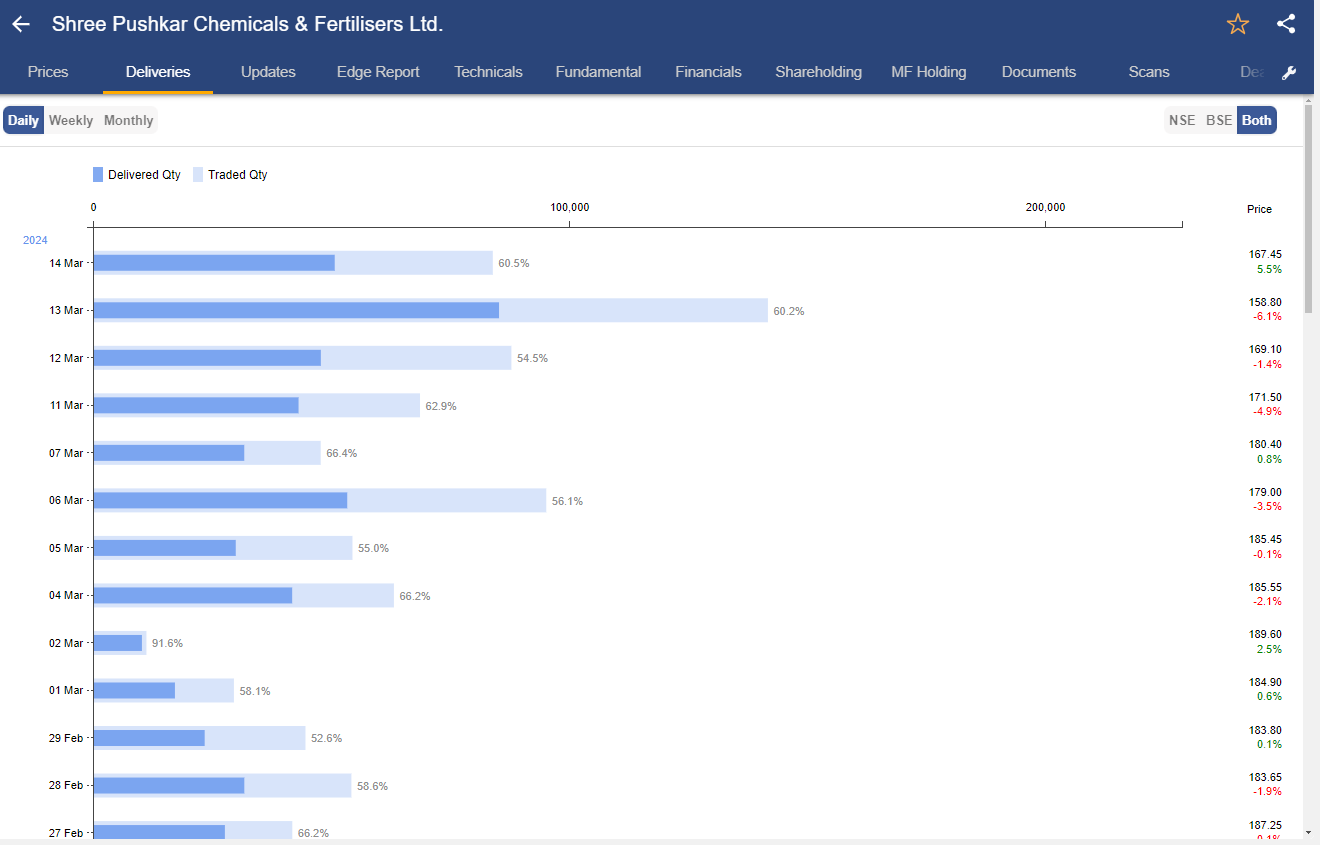

There seems to be accumulation going on in this stock…

-

if one checks monthly deliveries, price range of 220-235 which was previous swing high, we had high volumes with below 50% delivery volumes.

-

Post fall of 35-40% plus, the volumes have dried up and delivery %rages have gone up, averaging 50% plus very month since Nov2022.

-

This according to me is accumulation that is happening in this stock.

-

The bad news about capex delays, covid, machinery breakdown. geopolitics, Rus-Uk war, textile industry not doing well etc… all seem to be factored in the price now…

-

Technically as well stock seems to have bottomed out at Fibo 0.618 levels.

1 Like

What website gives this kind of data or is it a software?

its stockedge app, u can also get delivery data from NSE Website.

If i may ask, Which tool are you using for this information ?

rupeevest website has the details

1 Like