Hi @dd1474 , higher inventory causing dip in bottomline. Your view on this, please.

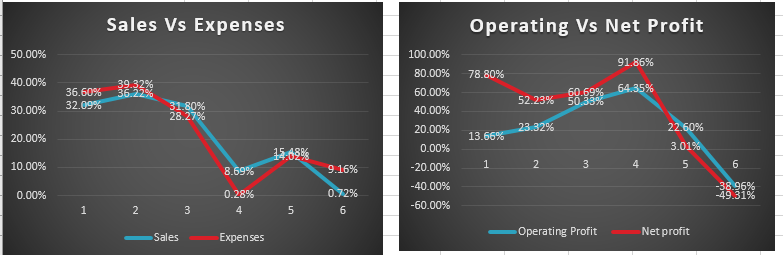

There was concern last time that inventory was building up which is taken care during the Q1FY20, but then there is now concern about margin. while the accumulated inventory is sold out, the company has not gained from operating leverage of higher Sales as seen from drop in margin. Sales growth nominal 1% while Consolidated net profit decline by 49% as compared with Q1FY19.

It is diffcult in small companies when there are no press release from managment to infer from only financials. I would look forward to sales and net profit growth in next 2-3 quarters.

Overall result is poor in my opinion. Having said that, very rarely we come across idea which are secular in growth in topline and bottomline.

Discl: Continue to hold my investment, view may be biased, Investor shall do his/her own due diligence before making any investment.

Annual Report Fy19 notes:

Industry Overview

- The Company’s growth is primarily interlinked with the Electrical, Electronics and Automotive Industries.

- The electronic components segment is expected to see bright days in near future and exports are expected to grow as the government has increased the export incentives for this industry.

- The recent rise in the custom duties on energy meters, electronic products etc. will push up the demand for the components used in these products and thereby will increase the domestic production.

- The emerging high growth areas for domestic manufacturing are automotive components, electric vehicles and smart meters.

Company Overview

- Engaged in the business of manufacturing & sales of Thermostatic Bimetal/Trimetal strips, components, Spring Rolled Stainless Steels, EB welded products with multigauge, Cold Bonded Bimetal Strips and Parts etc.

- The co is specialized in joining of materials through various methods such as Diffussion Bonding/Cladding, Electron Beam welding, Solder Reflow and Resistance Welding etc., and offers precision manufactured components specific to the application requirements and a single vendor to many prestigious OEM’s since 1986 and have successfully met the most stringent of demands set by multiple large global organizations.

- The application of co’s products are mainly in Switchgears, Circuit Breakers and various other Electrical and Electronic devices.

- The co’s products are exported to over 40 Countries around the world.

Principal Business Activities

Geography break-up (seen first time in Fy19 AR)

Future Outlook

- The future outlook is optimistic, despite of the slow-down in the first quarter of FY 2019-20.

- The outlook for co’s business (in long term) is positive based on the following developments in regulatory framework in India:

- Electric Vehicle Market/FAME India Phase-II Programme: In March 2019, the Indian government announced the second phase of FAME–II (Faster Adoption and Manufacturing of Hybrid and Electric vehicles), which envisages setting up of about 2700 charging stations across the country. The government has announced an outlay of 10,000 cr for FAME-II to boost the number of electric vehicles in India. The government will offer the incentives for electric buses, three-wheelers and four-wheelers to be used for commercial purposes. FAME-II will offer incentives to manufacturers, who invest in developing electric vehicles and its components, including lithium-ion batteries and electric motors.

- The co is quite hopeful with the opportunities available and constantly working towards developing the integral components for Smart Meters and Electric Vehicles (both two wheelers and four wheelers) projects in a phased manner. Expecting the aforementioned activities to enhance our revenues/profit in the future.

Recognition or Awards

- Preferred supplier for Siemens, Schneider & Legrand and other leading electrical companies

- Awarded best supplier in the Chennai Plant Supplier meet by Schneider Electric in Mar 2019

- Recognition towards significant contribution made by the co in Electrical Standard Product during the Fy18-19 by L&T Electrical & Automation

- Awarded by Siemens in Sep 2018 as Long Term Business Relationship

- Awarded Supplier Quality Award - 2019 (Gold) by L&T Electrical & Automation

Expansion

- The co has upgraded its quality and process control systems as per the latest IATF16949 standards and received the necessary re-certifications from the IATF16949 Auditors (TÜV).

- The setup of the AEC (Automotive Electronics Council) compliant test facility had incremental upgrades in terms of software and equipment installations to comply with the up-to-date test requirements and to increase the overall capability and capacity of simultaneous research and testing.

- The existing stamping facility is now in its upgradation phase II wherein the remaining mechanical presses are being replaced with new high speed and high accuracy presses. This will provide a significant increase in accuracy, safety and capacity.

- Various manual finishing and inspection processes are being automated. Progress will be done in phase-wise manner as per the planned schedule.

- Co had succeeded in getting 2,324 sq.mt. of land on lease from the Department of Industries adjacent to the existing manufacturing facility. The construction plans got delayed due to various approvals & finalization of drawings/design based on technical requirement of some of the processes. All approvals including drawings/ designs are in place and the construction on this land will commence during Oct 2019 and is expected to be completed by end of Dec 2020.

UNIT-IV

- Construction of factory building is going on and is expected to be completed as per schedule (i.e. construction expected to be completed by Oct 2020).

Remuneration Change

Foreign exchange earnings and Outgo

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/da57085e-14c8-4a61-a41d-d9cc6b68ae2d.pdf

https://dir.indiamart.com/impcat/precision-shunt-resistors.html

competitors of shivalik bimetal.

Annual Report - https://www.bseindia.com/xml-data/corpfiling/AttachHis/da57085e-14c8-4a61-a41d-d9cc6b68ae2d.pdf

Some good names in top ten shareholders

Please share key takeaways from the meeting if anyone attended AGM.

The mega drive to install smart meters in every household is off to a slow start. Of the five million to be offered in the first tender, in 2018, barely a fourth has been supplied by meter companies.

However, EESL, the nodal agency entrusted with the initial tendering, installation and consultancy, says it aims to procure 20 million meters and install two million of these by March 2020.

“The delay in supply initially did put back the process by six months. But, we are back on track. We have a strong pipeline. The next tender that we will float is of 10 million meters. So, supply will not be an issue,” Saurav Kumar, managing director, told Business Standard .

In March, the Union minister for power, R K Singh, announced 100 per cent smart metering in two years. A smart meter has a modem (communication device) and a remote switch by which demand, supply and billing can be monitored and controlled remotely. Data from these is collected in a cloud server. This reduces energy theft, improves billing and bill collection. It also helps power distribution companies (discoms) collect data on demand patterns, for use in planning of supply.

EESL has installed 400,000 smart meters till date, in Uttar Pradesh, Delhi, Haryana, Bihar and Andhra Pradesh. It is in talks with the governments of Rajasthan, Telangana and Karnataka to tender and install these.

Kumar said the areas where meters are operational have already brought benefits for the discoms. For Kesco (Kanpur, UP), NDMC (Delhi) and PVVNL (Meerut, UP), the cumulative net increase in monthly revenue is 15 per cent a month. NDMC saw its revenue shooting up by Rs 507 crore a month.

Supply constraints have slowed the procurement process. The lowest bidder for the first tender in 2018 was state-owned ITI, which has supplied barely 5,000 meters. EESL plans to blacklist it. It has already blacklisted Keonics. The gap in supply is being met by the second lowest bidder, Genus, which has supplied a million meters. The second tender, won by a Chinese company, was scrapped as the supplier didn’t have the necessary quality certificates.

The latest tender this year was won by PT Hexing, which would supply five million meters. The price has come down to Rs 2,200 a meter, from Rs 2,400 in the first tender.

EESL says the installation model is aimed to maximise the revenues of discoms. A discom needs to pay EESL Rs 70-95 (single phase-three phase) a meter and provide access to billing and consumer data. Meter supply, upgradation of system integration, meter management system and billing is done by EESL. It has tied up with telecom service providers and cloud server ORACLE for this.

A telecom company earns Rs 6-8 a meter. For UP and Haryana, it tied up with Vodafone and BSNL. System integration takes Rs 20-25 a unit. All this comes from the per-meter payment EESL receives from the discom.

Meter suppliers have other problems. Many have complained against falling prices, participation of Chinese entities and lack of back-end infrastructure. Several expressed concern that states had been slow in installing these.

Earlier, Business Standard had reported that large players gave a miss to the smart metering tenders in the past, citing irregularities in the bidding document. Government officials contend leading companies have different communication technologies from what states have. However, they are streamlining this, with the same bid document, technology specifications and back-end infrastructure across the country.

“Creating back-end infra takes time. The System Integration which will monitor and collect data for all smart meters has to be standardised across the country. So, we had to reach out to discoms in every state to use similar technology,” said Kumar.

He said a smart meter has multiple benefits. “The system that has been designed will be used for value added services in the future. The same meter can be for pre-paid, for managing peak load, integration of renewable (energy) and time of tariff. It sets the stage for future reforms,” stated Kumar.

First Published: Mon, September 16 2019. 02:12 IST

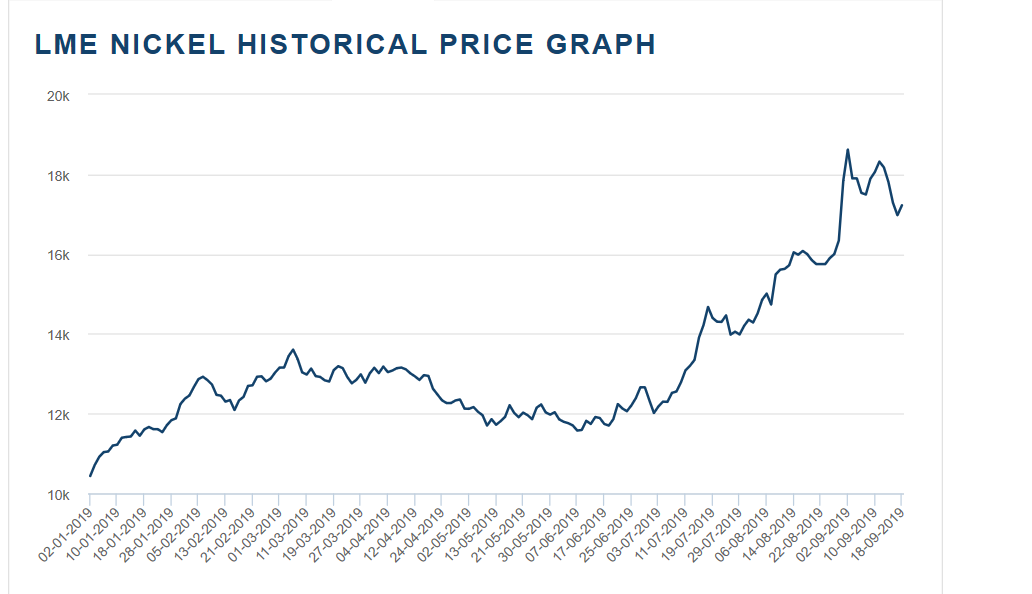

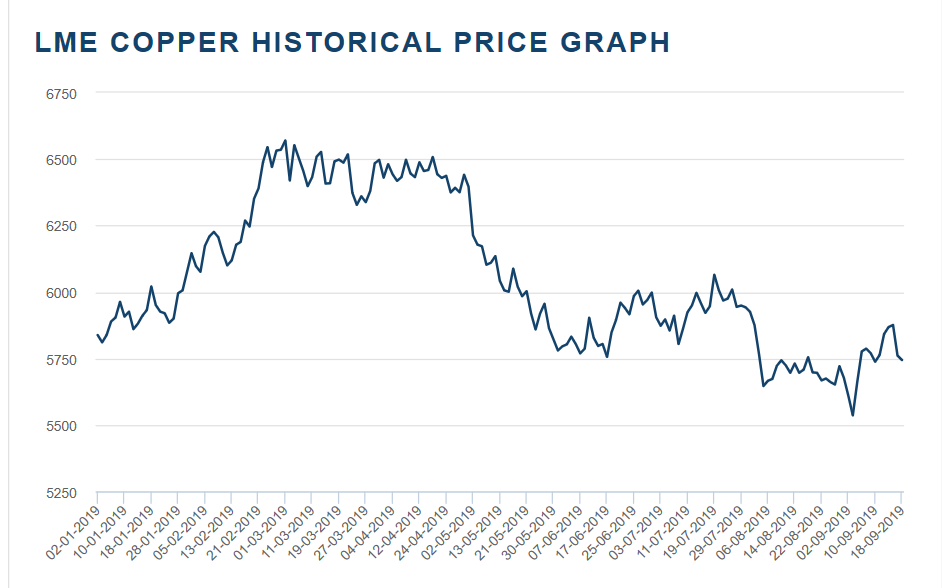

Nickel and Copper for 50% of costs of Shivalik. There was an increase of about 50% in short period of 2 months. Copper on the other hand has come down from highs in March. Of course these can be passed on to customers eventually

Continuing the discussion from Shivalik Bimetal Controls Ltd:

Something seems seriously wrong. The unabated selling has started from 10.40 am on 11th sept just after.the AGM started. There is surely something which some people including the management know and other investors are in the dark. Would appreciate if someone can throw some light

Story seems intact.Temporary headwinds may be there in form of current slowdown in auto smart meters and real estate impacting geyser sale. main promoter Ghumman is a sincere ethical technocrat who has executed well over last few years.2nd gen is good. lets have a long term POV n dont sell at the current cheap valuation. rather from a 2 year POV it seems a steal.

discl-invested from higher level

I have following queries in my mind Could someone clear these

Ques 1 Return on capital invested from last three quarters increased but at the same time capex is reducing .

Ques 2 If the management see the disproportionate revenue streams WHY they are not expanding .?

Ques 3 : There is negative cash flows from Last three years What will be effect of this on future earnings ?

Ques 4 : in quarterly data Q2Q growth in Net Profit exceeding Operating Profit Than Operating profit takes the lead Does it means detoriating picture for the Bottom line ?

in the book V discipline author says

," Balancing market growth and capacity expansion is a dynamic problem. Developing a profitable mix of price, product (or service) quality, design, and availability that make a strong market position is a dynamic problem. Improving quality, lowering total costs, and satisfying customers in a sustainable manner is a dynamic problem".

So How The company’s model is addressing the Dynamics of Growth?

If the Stock is tumbling so there MUST be some reasons

ALso from couple of quarters the % of deprictaion is increased when compared with same quarter last year Depreciation 2.56% 0.89% 2.63% 2.59% 14.17% 28.32% Does that means Promotors are Pocketing more money in the cover of Depreciation ?

expenses are on rise on the other hand the sale is not so robust ? that worries me ANy Investor please solve the query

disc : not invested But valuation seems attractive not Sebi approved Analyst

I had attended the AGM of Shivalik Bimetal Controls Ltd. Some of the points noted during the AGM are given below:

• Current year performance is challenging on account of slowdown in automobile segment and higher inventory stocking by one of our key customers on the shunt side. Markets are challenging due to overall slowdown in economy in India as well as globally. However, over medium to long term we continue to work as per our original plans. We have got orders from European OEM companies whom we were in talks with for years. Supplies to these companies will start from second half of this year.

• Margins of 18-20% came due to certain product mix during FY19. As of now, it looks difficult to sustain such margins in current year. Look at our historical margins as benchmark.

• Bimetals continue to perform well. Last year we entered US markets and that has performed well for us.

• Shunts – new competition will come in. We are optimistic on electric meter side in India as well as exports. We have had breakthrough with one of the largest European electric meter manufacturer. In domestic markets, pricing is a challenge.

• Inventory had increased over the past two years primarily due to finished goods inventory build up at year end for supplies in next quarter. Also, need to keep raw material inventory as largely its imported from Japanese suppliers and lead time is high.

• We will work on better inventory management, automation and reduce labour costs.

• In shunts, ultimately Chinese competition will also come in. However, we will have head start over other competitors due to us being one of the early entrants as well as qualifying with many large customers which takes years to develop.

• Bimetals are commodity but we established relationship with many large customers. It is difficult to get qualification to supply to some of the large and established customers we are supplying to.

• Some of the large contracts we have are for long term of at least 3 – 5 years.

• We have been able to get contracts from 3 mobile phone chip manufacturers which we were in discussions with.

• All the new developments for medium to long term are on track. We are close to commercialisation of lot of our contracts which we had discussed in last AGM. 2020 is expected to be much better year despite slowdown. We have doubled our efforts in exports and do expect better things to report in 2020.

• Our expansion plans are on track in both shunts and bimetals and expected to be completed next year. We can quadruple our capacity in shunts over the medium term.

• We are working on a replacement of solar cell PV replacement product which is being developed by 2 PhDs in USA. We are the only company in the world which has been able to develop its prototype. If its successful commercially, we will have to stop manufacturing everything else and just focus on it given the huge demand!

Many people have been asking for my views. Thought of sharing (personal thoughts):

Thoughts on business:

I have been excited to see the growth delivered by the company over last 3-4 years and this growth has been very exciting as the growth has been coming from a new segment which finds application in new areas like EV Batteries, Smart energy meters etc. I also like that a small company based out of Solan is serving some very high end/marquee global names and is perhaps the only company from India manufacturing these products.

What has gone wrong:

- Q1FY20 was a total surprise on the margins front and that led to the start of the fall.

- At the AGM, the commentary of the company was weak for the near term - given the global slowdown in automotive segment. Infact their key clients were surprised with the slowdown and some inventory rationalization is going on. Which might lead to softer earnings for coming quarters. The company did sound positive for 2020 saying that new clients and programs should start. Broadly they said they are on their plans for medium to longer term.

- Many of the investors were irked with the attitude of the management - that they don’t want to open up too much and denied most of the requests of investors of plant visit, concall etc. These days these points have been paramount for institutional investors to participate as they seek clarity and good governance.

Regards,

Ayush

PS: Above are my personal views and may be biased as my family and fund would be invested. We may change our views, if needed ![]()

Drop in revenue and drop in profits for Shivalik in Q2:

Commenting on results for the third quarter 2019, Dr. Gerald Paul, President and Chief Executive Officer stated, “Vishay’s

financial performance has been negatively impacted by low demand, especially from dist ribution. However, during the third

quarter inventories of Vishay’s products at dist ribution started to come down noticeably. Still high levels of inventories in

the global supply chain should impact our business for another two quarters. We are managing the slowdown by adapting

costs as we have done in the past. On the other hand, our increased machine capacities will enable Vishay to participate in

the next upturn to the full extent.”

This could be one of the reasons for sharp fall in Shivaliks valuations. Vishay is the largest client and its guidance for next 2 quarters is weak.

One of the things that I came across as an alternate to Shunt resistors is hall effect sensors. Just like shunt resistors hall effect sensors are used to measure current and are supposedly more accurate.

Some of the questions that I have for the industry experts here:

a) What are the key difference between Shunt Resistors and Hall Effect sensors and are they interchangeable? Which one is preferred vs the other and why and in what situations?

b) It would be really helpful if we can find out about EV battery design choices in Indian companies like Mahindra and Tata who seem to have some lead on this.

Ofcourse outside of EV also shunt resistors are extensively used.

I dont understand the technology at all and request experts to take this forward.

Hall effect sensors use magnetic element to crate hall effect hence generate voltage across metal. Given the same application shunt resistors shall be much more cost effective than hall effect sensors as we need to measure voltages of multiple cells that make huge battery. I believe shunt resisters shall be cost effective choice over hall effect sensors for battery management systems

Hi Ram, as you are related to this industry, can you educate us more based on the insights that you may be seeing. Key questions are - 1. Is the adoption of shunt increasing rapidly - if yes, why? what edge does Shivalik have to be the only company in India to be producing this? how would they be standing globally? 2. Despite higher cost for hall sensors - are they superior and provide better performance when compared to shunts? If yes, are you seeing a shift happening in the industry or is it a long term monitorable?

Thanks,

Ayush