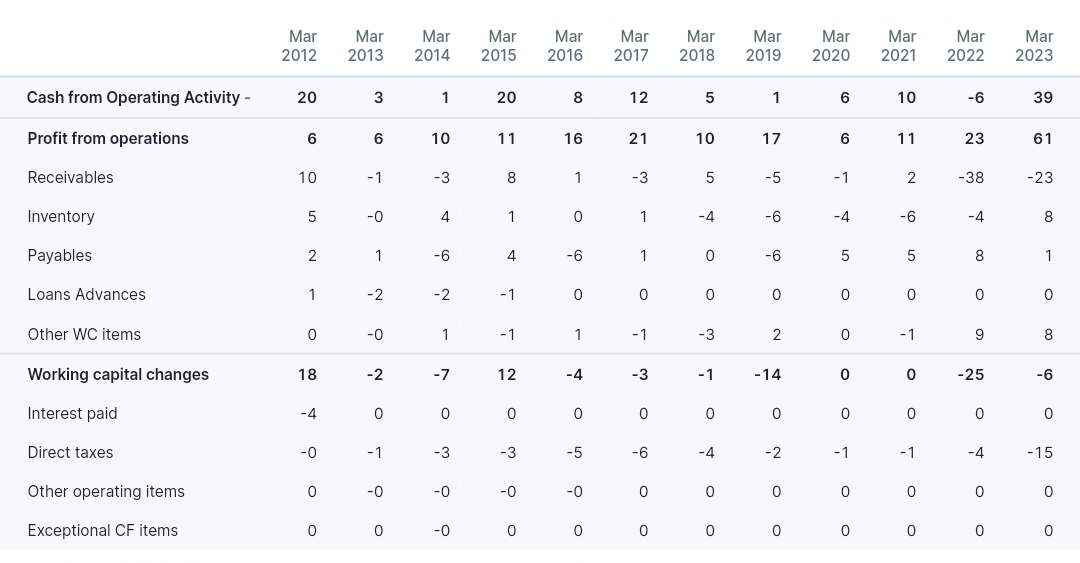

What is the problem with the cash flow cycle? Please specify. Is the number of days for receivables going up or is the company paying out payables earlier than expected? Or may be something else?

So from Zauba import export data, it is evident that a US based company called Custom Magnetic Inc is one of Shilchar’s clients. Custom Magnetic themselves are a transformer manufacturing company and was founded by a certain Mr. Kirti P Shah who used to be one of the top 10 shareholders in Shilchar.

Their website mentions about a Joint venture partner in Baroda (name not mentioned).

Wonder if Custom Magnetic is subletting their US orders to Shilchar. Not that it should matter much, but just an observation…

13 Likes

Sharing some notes from tracking exports for last 1 yr+ at high level

- Real kicker for them is exports of Power n distribution transformers (supported by huge demand supply mismatch), which have way higher KVA ratings (and they supply directly to Energy giants MNCs - something other Transformer players are yet to crack/scale ) ,

- custom magenetics is a long standing client & exports fall under below HS code, less than 1 KVA (more in telecom & electronics transformers) - this is likely very small in overall scheme of things

- per concall of exports - US are arnd 30% while 70% type is in Middle east, most of tools tracks US side shipments

Promoters deserve credit for getting global approvals and having invested in plant during down cycle years here - all of this is culminating in numbers delivery from last many qtrs (6-7).

investors like @sharemarketgen_ , @T11 and other VPers here have identified the trend way early and got on the ride, and kept sharing info/AGM notes right from times when mkt cap < 300-400 cr , totally different thing as to how many actually continue to hold it given solid rise & a legacy narrative to bucket sector in cyclical etc(however length of cycle is something mkt has surprised many) !! Been a solid learning for self as well.

Transformer sector dynamics and promoter commentaries clearly support tailwinds to persist for some time to come, though names seem to be getting in well discovered zone now.

D - invested

23 Likes

My observation is that majority of PAT is going towards additional receivables. In such a scenario the company will be short of funds in the long term. This requires Debt or Equity dilution.

So why is that a problem? Would that not be true of any fast growing business? After a point of time, you will run out of money to finance your working capital cycle or do put up the required capex. Had the working capital cycle worsened by more than 30% or had they written off a lot of receivables, I would have understood. Do you see something like that happening?

3 Likes

Hi. Thank you for sharing this granular insight. How to quantify the exports which are being done for Higher KVA Ratings?

Any business which grows Sales fast, should also have it’s Cash Flow’s growing at similar growth rate. For context in this case CF Growth is 6% whereas PAT growth is 40%. If the company wants to keep growing at 40% the growth it has to be debt funded or through equity dilution which would reduce RoE.

If the working capital situation worsens or there is write-off, the stock will keep on hitting lower circuits till it’s just worth it’s current market assets. But this is worst case scenario and companies avoid this at all costs.

Every Investor has unique perspective. My perspective is sustainability of business with reasonable growth. My style does not rely on 100m dash, rather I focus more on marathon runs.

All the Best.

8 Likes

On the contrary, I think there would be an explosion of demand. There are multiple mega trends powering the growth of the entire power value chain and power equipment manufacturers are in a sweet spot.

Some of these mega trends:

Drivers of growth capex:

- Data Centers

Cloud migration is a huge driver. Plus AI which is like an avalanche gathering snow, will generate tremendous demand for electricity, that too, high voltage and stable electricity without any disruptions.

2. EVs and their increasing use (notwithstanding the current blip)

-

In India massive capex in railways (think new, high speed trains) and electrification of railways

-

Make in India and Atmanirbhar Bharat initiatives leading to a surge in manufacturing

-

Increasing use of renewable sources of energy where there is huge fluctuation in production in geographical and time perspective (solar, wind etc produced only at certain times of the day/year in certain parts of the country) so the peak capacity for a given level of production has to be higher. Also, the power so produced has to be ‘evacuated’ immediately.

Drivers of replacement capex:

The transmission grid and the related equipment both in the US and India (not familiar with the situation in the rest of the world) is ageing and needs massive capex for replacement.

11 Likes

The way Shilchar and TRIL are moving in tandem every day (5% Upper Circuit last few days) and today both at 5% Lower Circuit, without any apparent reason, I am beginning to feel these are operator driven? I know the long term story (at least till the end of the current cycle) is intact but this ‘every day circuit’ business looks a bit suspicious.

6 Likes

last quarter eps was 35. Let’s take 30 going fwd for 2 years. Given the tailwinds in this sector, this is base case.

Mgmt has guided for 900 cr top line in 2 years with new capacities incrementally online from April 2024.

Base case.

30 (eps) * 4 = 120 with existing capacity

60 (eps) * 4 = 240 with new capacity // 2026 end

240 * 30 PE = 7200 (stock price)

2 Likes

I don’t think that a fast growing business will/should run out of working capital. I can name many small companies who are growing fast but are very prudent in managing their cash flow.

It’s important to distinguish between long term capital requirement and day to day operating expenses. It’s OK to raise debt for the first if you are in a fast growth phase and can’t fund that with internal cash. But for the latter a company should be able to consistently generate enough cash, from their operations, to buy raw material, pay their employees, clear their bills and fix broken equipment, at a very minimum, and still have enough for rainy days. If the management can’t do that, then either it’s a reflection of poor quality of management or nature of the industry.

2 Likes

Hi. Please share three such names. I will look at them and learn what are they doing to manage working capital so well, even while growing revenues 50% a year or more.

There are many but from the same space you can look at Voltamp and Techno Electric. Check the trends in working capital and cash conversion cycles. Zero debt, healthy cash flow generation and run by good management. In the capital sector you can look at names such as Triveni Turbine, KEI industries etc. Very healthy balance sheet and working capital management.

Then there are names from highly cash guzzling and low ROCE sectors like construction such as NCC. They do lots of projects for government customers who are known for delaying/withholding payments. Company is focused on strengthening balance sheet through prudent working capital management and it reflects in their continuously declining debt.

7 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/51fddf53-dd3a-43a8-905f-9c35273cf238.pdf

YOY numbers are very good. QOQ there is a dip in revenue, but margin is up. Seems growth was constrained due to capacity - there is no reference to status of expansion plans.

1 Like

Is there an error in screener.in for last year’s EPS?

Good observation. They did first concall last qtr, hope there is one for this qtr also

No. It’s due to the bonus shares

1 Like

So far they have not announced for the call nor have they published an investor presentation

Shilchar reported solid earnings today. EBITDA margins remain rock solid at 30%,head and shoulders above peers. Revenue growth was disappointing however there is a large jump in inventories at 60 cr. for FY24. Company was slated to add around 40% capacity from April 1st. I am quiet sure Q1 will be better than Q4.

As an aside,while people are free to interpret data as they deem fit…recent posts on this thread seem increasingly disconnected from reality. So much so that people are suggesting Shilchar will need to dilute! Here is the current economics of the business:

Capex of 30 cr,addition of ~90% capacity on base of 4000 MVA. Company has done 118 cr revs in Q3 and should be able to do 500 cr on annual basis given current capacity. This number is going up by 90% assuming current realisations. Thus,an addition of roughly 450 cr revenue at a cost of 30 cr. However,this won’t happen in Year 1 itself. Let’s assume 50% utilization in Year 1. One gets addl revenue of 200 cr.

Given that the WC is 86-90 days this implies a capital employed of ~80 cr(50 cr wc+30 capex)

So what incremental margins does the company need to do to make 20% RoCE?

On assumed utilization of 50% the answer will be just 8% ebitda!(16/80)

However,Shilchar is currently making north of 25% margins. Even assuming a margin of 25% one gets RoCE of 60%. This in Year 1 itself at 50% utilization. Q4 exit is at 30% ebitda

At peak,we are talking of an RoCE of 80-90% on incremental capital employed!

I don’t see how such a company will ever need to dilute. On the contrary,markets are paying 50-55x fwd for a company from the same sector that has diluted to repair a broken B/S and has another QIP lined up. Shilchar is most likely trading at 35x fwd unless the whole economics of the business goes for a toss in coming quarters.

Disc.: Invested. Views are biased.

37 Likes

Added to your note, During Q3 con call, Management clearly guided for Revenue in range of 100 - 125 cr. , which they have delivered. They also mentioned at least for foreseeable future (1 yr), margins will be intact which is also true in Q4 results. They have lot of orders in hand, niche segment of transformers and a tail wind sector (renewables), Demand to stay strong for atleast 5 years. Management is walking the walk, looking for good times. Q4 results will flush out weak hands or the ones who entered for sheer momentum and social media following

Disc: Invested from lower levels

2 Likes