This could be for personal reasons - but it is not our concern. The good news would be the removal of pledges and buyout of Carlyle who have a track record of entering and exiting animal health care.

2 Likes

I think it is fantastic for minority shareholders and would not tender at 86 under any circumstances. I understand your concern regarding exit levels as many have been stuck in this stock for years. I have been holding this stock myself for many years with 0 returns. Pls understand this is a distressed sale and the valuation of Sequent is significantly higher that’s the open offer.

2 Likes

This seems like a good long-term play now. With Carlyle group as new promoters, the co’s push towards improved profitability will be accelerated.

Can long term investors in this throw some light on what can be sustainable margins and debt levels in this company?

My understanding is that the new promoters will try to pay down debt first.

Disc :- Not invested. Started Analysing.

3 Likes

I went through the FY20AR of the company. Below are the pointers

- Company operates in 2 segments APIs (35%) and Formulations (65%). Formulations have higher margins that APIs.

- Major geographical segments are Europe (47%), EM (21) , Turkey (18) and LATAM (14%).

- Regulated Markets (68%) vs Non Regulated markets (32%). Regulatory margins are higher however Turkey has the highest margins.

- Margins are high in Injectables (29%) as compared to oral dosage forms and in Turkey, injectables sales is higher.

- Company has manufacturing facility in all the key geographies.

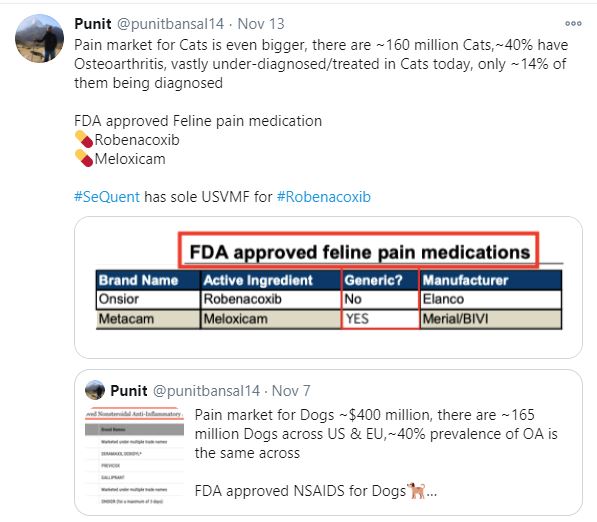

- There are just 4-5 large players in the Vet API/Pharma industry. The company doesn’t supply anything to Companion pets which has the market size of $12.54B however they are top 20 players in Farm animal market with market size of $20B.

- Company has presence in Vet API space in US market however they have filed 14 new products in last 3 years.

- Company is planning to launch a key product in Europe market by this year’s end with potential global market size of $500M.

- US launch is still 18 months away.

- Global players make 30%+ EBITDA margins in this industry and company believes that they can keep increasing the margin by 200 bps Y-o-Y due to new product launches in EU and US.

- Company sees 15% growth in Turkey and EU markets and slight growth in EM despite having significant reduction in Q1 due to payment issues. This growth in EM will include the ZOETIS licensed products.

- Margins Company is clear that the pricing in Animal API and formulations space remains stable and hence there were no one-offs in Q4FY20. Operating leverage will keep playing.

- Company manufactures APIs for top 4 global players and hence they can get more business with increase in wallet share.

It is one of the best AR’s I have read.

Disc. Currently not invested, waiting for better price levels. Historically sales growth with margin expansion has resulted in multibaggars.

26 Likes

Lupin’s Non Executive Vice-Chairman Kamal Sharma joins SeQuent Scientific as Chairman

3 Likes

How do you think Carlyle group will make an exit, as it’s already listed? By getting a new promoter or some other Pe investor? I’m asking this to understand what will happen in future, without any promoter and small stakes by pe investors and institutions.

Lot of options on the table once business gets scaled up in terms of revenues in the US and EBITDA margins get reset (for Carlyle to sell Sequent).

I would think below scenarios are possible and I am ranking them below in order of most likely buyer.

- Larger pharma companies- who want to diversify into animal health space (lot of companies might get interested given niche space)

- New late stage PE investor

- Large international animal health companies like Zoetis (they are already in collaboration with Zeotis and have a multi-year agreement with Zoetis India to market and distribute their ruminant portfolio in India as per recent conf call). Zoetis also interested to expand its India business (https://telanganatoday.com/zoetis-to-expand-india-presence)

- Smaller regional companies with aim to vertically integrate and go international with help of PE (eg. Hester Bio)

- Least likely (as this rarely happens in India) but management buys out Carlyle’s stake.

4 Likes

I am seeing that a lot of people are actually taking Carlyle’s astute leadership and experience in animal health space for granted. I checked their last 3 investments in this space ie. Manna pro products (unlisted company in Spain), Saprogal (unlisted company in Spain) and CP Pokphand (listed company in China/HK) and below are my findings:

1. Manna pro products: Carlyle acquired Manna Pro when it absorbed the portfolio of private equity fund Broad Sky Partners in 2015. (link1) and sold in around Dec 2017 (link2). During this time Manna pro products tripled its EBITDA from $10mn to $30mn as per link2 above. A Debtwire report, citing anonymous sources, said the deal valued the business at about $330 million. (link3)

2. Saprogal: Carlyle acquired Saprogal from ConAgra foods in May 2004 (link4). Saprogal had 2003 sales of over €250 million. In October 2005 Carlyle sold its investment in Saprogal (link5). Carlyle sold Mercapital which paid more than €150m (US$186.6m) for Saprogal (link6). No disclosures around entry valuation and profits.

3. CP Pokphand (CPP): Carlyle bought 11.3% stake in CP Pokphand in July 2010 (link7). CPP’s revenues increased 1.7 times during 2010 to 2013 but net income rose by just 40% in this period (as per public disclosures). I couldn’t find any news on when Carlyle exited CPP.

Disclosure: Not invested. This is not an investment advise. Do your own research before investing.

15 Likes

3 Likes

Sequent Scientific has entered into a definitive agreement with Dr Huseyin Aydin for the acquisition of 40% stake from him in Provet for $17 million.

2 Likes

Sequent acquires 40% stake in Provet.

6 Likes

Sequent entered into a definitive agreement with Mr. Servatius Justinus Cornelius Maria Van Der Heijden for the acquisition of 15% stake from him in Fendigo BV through Alivira Animal Health Limited. After completion of the proposed acquisition, Fendigo BV will become a Wholly Owned Subsidiary of the Company.

Fendigo is a trading and distribution company in animal heath products.

1 Like

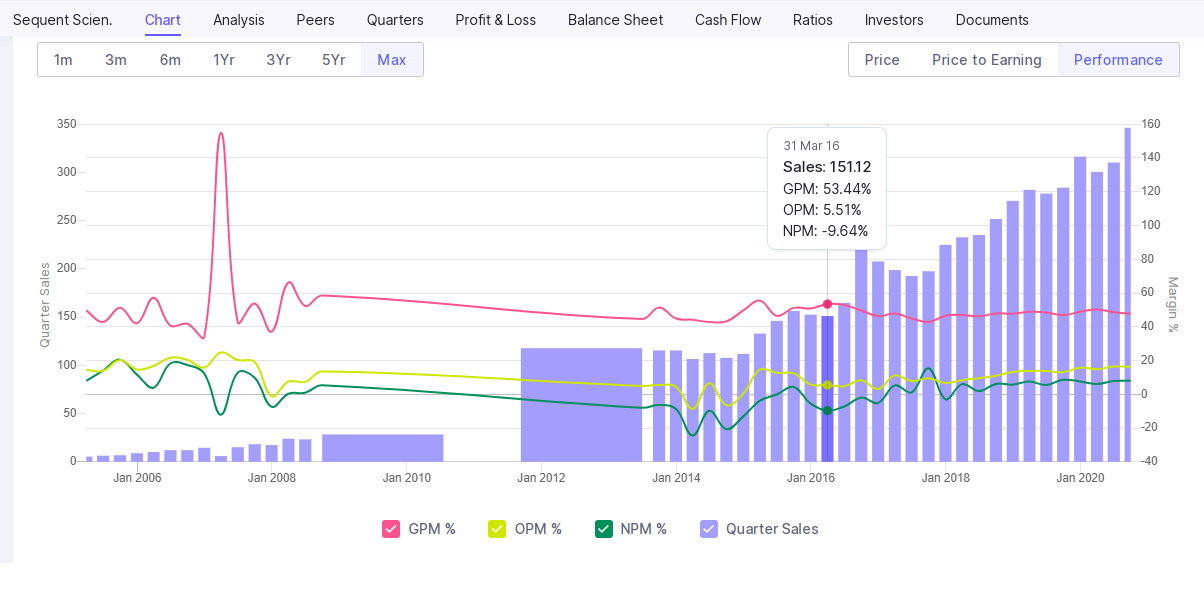

Decent set of results from Sequent

- Revenues up 21.8% yoy

- Ebidta margins up 400bps

- Consolidation of subsidiaries using funds from sale of Strides shares

- debt reduction and good cash flow generation

- CDMO model started with a large AH player

- number of upcoming formulations and api products under development

Here is a research report and con call summary from Sapling capital

https://drive.google.com/file/d/1Cn1MKHk2YQj_viDNMsOQ9GqyIc495vBR/view

6 Likes

Looking at the Q-o-Q performance, company has fairly stable Gross margins. Operating margins have improved from ~7% in Q418 to 16% in Q2 21.

Change in promoter to Carlyle group will further strengthen company’s ability as a global animal healthcare player.

Reduction in debt to boost bottomline going forward. As on Sept 20, company has debt of 261 crore with cash & cash equivalent of 125 crore and investments worth 231 crore.

1 Like

How come you knew it well before hand that promoters will exit the company by selling it to a PE fund ? As I have recently started following the company, I want to know whether promoters had indicated that they plan to sell their holding ? Or was it a good guess? Or by going with promoters history of selling their business? Thank you

2 Likes

Although not directed to me, but if you track Arun Kumar, he is great at scaling up businesses and then selling once they reach a certain scale.

Won’t be surprised if he eventually look to sell some part of solara and Strides too, infact in strides he sold Australian business which was the largest revenue contributor at that time.

Disc : invested in Strides and Sequent.

6 Likes

Sequent Scientific: Co Received The World’S Largest Injectable Tulathromycin Approval Within 11 Months Of Filing In The European Market During Q2FY21

4 Likes

Q2-FY21 Earnings presentation notes

- [Scale]: Emerged as India’s largest and now amongst ‘Top 20’ global animal health companies.

- [EU approvals]: EU approvals received for: World’s largest injectable filing (Tulathromycin) within 11 months of filing 3 products approvals from Spain’s R&D development Commercialisation to drive H2 performance.

- [Revenue granularity]: 65% Sales to regulated markets. 80+ countries with marketing presence.

- [CDMO]: CDMO model initiated with one of the largest AH player – 2 products under execution

- [USVMF filing]: 1 USVMF filing in the quarter, 20 US filings in total

- [Production capacities]: Enhanced production capacity at Mahad, Vizag expansion to be completed in Q4

- [Formulations R&D]: 35 products under development at 4 R&D Centers. Injectables form 38% of the formulations. 10 new USVMF filings in next 3 years.

- [API R&D]: 14 APIs under development at 1 R&D center. 20 US filings and 11 CEP filings.

- [PAT one-off impact]; There was a 1-off impact on PAT (9cr) in Q2-FY21. 5cr of One-time Bonus to employees & Accelerated vesting of ESOPs on change of control. Alivira France operations discontinued due to adverse business environment costing 4cr inr.

- [Debt position]: Due to strong financial position, the net debt to equity (0.38 to 0.2) and net debt to EBITDA ratios (2.8 to 0.67) have improved in the last few years.

- [Delivering on Guidance]: Management has guided for high teen revenue growth and 200 BPS EBITDA margin expansion. Revenue grew by 17% in H1 and margin expanded by 340 BPS.

Q2-FY21 concall notes

- [Management change]: Seamless transition to the new promoter, Carlyle Group Will give the strategic direction as well as resources to drive the company into the next orbit.

- [Sequent 2.0]: Company has consolidated its minority holdings in Turkey and Netherlands, a clear reflection of the confidence in the growth potential of these businesses going forward.

- [Growth goals]: Hired Stonehaven Consulting, a niche animal health consulting firm to help us draw out a blueprint of the journey of the company into the next orbit. Inputs from Stonehaven will transform the outlook and put us on a path that would enable us to being amongst the global top 10 animal health companies in the world.

- [Formulations Growth drivers]: The growth for the quarter was formulations led, with the formulations business growing at 24.7% for the quarter, driven by the geographies of Latin America and Turkey.

- [API growth]: API business grew at 18% during the quarter. We recorded our highest ever revenues of INR 120 crores in this business.

- [FCF & RoCE]: Focus is on cash generation; INR 100 crores of free cash generated in the first half, while our EBITDA-to-cash conversion is 80% plus. At this rate, we expect to become debt-free in next 12 months’ time. The return on capital employed is also now in its early 20s, almost a 3x growth in the last 3 years.

- [Tulathromycin]: This being the largest injectable product in animal health, this would be kind of a game changer in AH industry (in terms of competitiveness), which generally does not see too many launches on day one of patent expiry. As There are 13 approvals for this product in Europe, including ourselves. We have never taken it as a big part of our business plan. It was a learning exercise. Most of us come from human pharma so we are aware of the hyper competition that exists. We had kept very small numbers for ourselves. But yes, it will be a good wakeup call for many of the animal health guys who are not used to seeing such kind of competition.

- [AH industry price erosion & Tulathromycin]: AH does not have the gap in terms of pricing between generics and innovative prices, as you see in human pharma. However, this product might be different, and we will figure out as we go along. We are ready for the day 1 launch. The patent expires in December, and we should be in the market at that point of time.

- [Decision to close France Facility]: COVID environment makes it difficult to do branded generics marketing operations in any country because, it is physical contact intensive, wherein in you go out and retail. With the new shareholders when we got together, one of the calls that was taken was that there was no point in continuing to lose.

- [India Biz]: Clearly, the scale up has occurred on 3 counts. One is the distribution of Zoetis (largest AH company) products that we started in the current quarter. Even our own portfolio has done very well, and we have grown about 32% in the first half as far as our cattle business is concerned, without considering the Zoetis portfolio. And third is the poultry side of business, which suffered in Q1 because of the COVID-related rumors about the poultry business. That has since died down. Therefore, the poultry business is also back on recovery mode in Q2.

- [Industry structure]: As a company we prefer smaller products, and that has been our strategy. That also is the way animal health industry is structured. We don’t foresee any, even a $100 million market product in animal health going off-patent in the next 3 years.

- [Reason for API growth]: There is no price-led growth, but it is a quality of business-led growth, as we move more and more from unregulated markets to the better markets of U.S. and Europe.

- [Stonehaven contribution]: It’s all about shaping the next vision for SeQuent, maybe in next 5 years’ time. And so the real scope of their work is setting up a vision for SeQuent 2.0, which may entail new markets and/or new areas of business. We are currently focused on production animals, should we look at companion animals as well. And as far as our own acquisition strategy for U.S. is concerned, again, that is one area of significant engagement with Stonehaven.

- [US business strategy]: there’s no way we can fast track anything in U.S. We will still be in line for a FY '22 launch as far as our formulation commercialization is concerned. In the U.S. there’s only 1 filing that we have made so far. And we are currently working on a pipeline of 10 products, which will be commercialized in the next 3 to 4 years.

- [Turkey operations]: Revenue growth lower vis-a-vis constant currency due to Turkey lira depreciation. Operations growing very fast (market share gains). Being a local manufacturer is very beneficial.

- [EBITDA to cash flow conversion]: When we look at players like Zoetis and Elanco, they basically convert 75% to 80% EBITDA into cash. Sequent’s 90% EBITDA to cash flow conversion in H1FY21 was one-off. More sustainable number is closer to Zoetis and Elanco’s 75%-80%.

- [CDMO business opportunity]: This is also part of the mandate we are working with Stonehaven. We are only going to focus on veterinary CDMOs and not get into the human space. We are yet to size this opportunity. It’s not a very well-defined industry per se, separately from human pharma. Currently, most of the CDMO work for AH business is undertaken by companies who do both AH and human pharma work. But going forward, there is a need of segregation. And that’s what we are getting feelers from our customers, and that was the reason for this foray.

- [Difference between US and Europe businesses]: While there are 13 approvals in EU (for Tulathromycin) , there is still not a single approval in U.S. Reason is that there are not many U.S. FDA-approved injectable plants in the veterinary space, while there are many in the EU. There is a big difference between the U.S. and EU as far as the injectables are concerned. We don’t foresee significant competition in the U.S., at least for some period of time.

- [Facilities in Europe]: We have 2 facilities in Europe; 1 in Germany, which is injectable; and another 1 in Spain, which is an oral facility.

- [Growth & Margin Guidance]: I think our guidance stays the same that we have been looking at mid-teens revenue growth and a 200 bps margin improvement year-on-year in medium term.

- [Carlyle group’s influence]: We are only looking at broadening our vision, which may entail certain bolder steps. If we were looking at U.S. acquisition, on our own, we could have looked at a $10 million or $20 million transaction. With Carlyle, it allows us to look at a bigger transaction. Will be guided by Stonehaven and/or Carlyle Group on our strategies for China simply because it is the second largest animal health market in the world.

- [Capex]: One is our expansion at Vizag plant, which we are scaling up. The first phase should be completed sometime in early Q4FY21. And the second phase will be completed next year. Between these 2 phases, we will be good enough to deliver our business requirements as we foresee for the next 3 to 4 years. And collective investment will be about $10 million in this. In addition, we are looking at an expansion at Bremer for our injectable footprint that was more to do to cater to the U.S. market. That is 1 project which is running late because of the current situation in Europe. That is something we have deferred by > 6 to 9 months, and it’ll have a total CapEx outlay of about EUR 3 million.

- [Can Sales be 3x in 5 years]: AH is a branded generic industry. And therefore, market share gains are always slow and steady. We cannot throw some money or hire more people and then double our sales and all that. Trying to grow too fast is dangerous in this industry. In a branded generic industry, unless there is a consumption, the material will come back as an expired material. So that’s why we have been guiding to a mid-teens growth and not a very substantive growth. Even growing at that rate, we are growing at double the industry growth rates. The third element, of course, is acquisitions. And that is something which can certainly help us scale faster. And there will be obviously an added area in the next phase of growth, given the Carlyle expertise

- [By when into top 10 companies]: On our own business plan basis, we were targeting to get into top 15 in the next 4 years’ time. Clearly, the gap between our current stage versus top 10 is very, very different. On our own, we had not envisaged that. Stonehaven is 4 to 5 months engagement. February or March is when we will have a better visibility in terms of the way ahead. And that is the time when we’ll be able to give a better answer to your question in terms of whether it is worth even chasing getting into top 10. While scale is good, it is not necessarily the best for the shareholders and which we will be. The good thing is that Carlyle is a shareholder. Their interests are aligned with the rest of the shareholders

- [Formulation Strategy]: Our formulation strategy is not a forward integration strategy with our APIs. Our formulation strategy and API strategy is very independent strategy. We are not seeing API as a cost arbitrage strategy for our formulation business. API is a separate business vertical for us with its own growth engine. Not all our formulations that we are developing for U.S. are based on our APIs.

Disc: Invested and increasing position.

22 Likes