I have some queries about Zerodha demat account, trading account and linked bank account.

What are charges for transfer of money from bank account to zerodha trading account and vice-a-versa?

How reliable is this transfer? Is there a possibility that, money gets debited from bank account and not credited instantly to zerodha account? Are there any follow-ups required?

Is it possible to calculate LTCG and STCG easily using FIFO algorithm if there is any LTCG/STCG applicable for current financial year? Is is automated like other full service brokers?

Is there any upcoming facility / tie up with any bank which can work like 3-in-1 account in zerodha, where we can allocate funds for equity and automatically internally funds are reserved for buying equity, instead of logging into bank account and transferring funds to zerodha trading account every time?

Note - I do not trade in F&O, and buy/hold shares for time period ranging from few months to decade as well but looking to reduce brokerage costs.

I am looking to migrate from full service broker to Zerodha, but there are some concerns, hence looking for more clarity. I generally prefer hassle-free transfers (do not want to spend time on follow ups or calling customer service), ease of use and good quality GUI. (I am willing to forget 3.5% saving account interest for some period in case funds are lying in trading account for few days/weeks).

I checked some discount brokers like Zerodha, Upstox (Mumbai based), and ICICI Direct.

With prepaid plans, you can reduce brokerage from 0.55% to 0.2% (1L prepaid plan) or 0.25% (75K prepaid plan) in ICICI Direct. This is justifiable only if one trade high volumes. With this, F&O trading charges can be reduced to Rs. 20/ or Rs. 30/ only depending on plan, so it is inline with Discount brokers.

Some observations are as below:

You keep earning 3.5% saving account interest as soon as amount is credited in your a/c after selling shares. In discount brokers case, mostly it will remain in trading a/c for some days or if you are planning to buy some other shares) after selling something you may keep it in trading a/c for few days/weeks. This is what some of us do.

There is no hassle of logging into your bank account every time you trade.

There are no transfer charges as in case of discount brokers, where for immediate transfer it is about INR 9 plus taxes, and for NEFT transfer it is free. But still there are some small charges to be paid.

IPO and FPO are not available on Zerodha. Occasionally we may need this. Not sure why this is not available as this is the basic feature for any broker.

So, though we can certainly reduce brokerage drastically from 0.25% to zero, and only need to incur 0.1% STT, SEBI charges, and NSE/BSE Transaction charges, still this comes to about 0.12%.

The saving in brokerage seems to be very high, with some hassle of logging in multiple times in bank account.

Is it worth going for prepaid plans to keep things simple? I am still researching on this from all perspectives.

Also, we can see that, no. of customers have dropped in case of ICICI Direct in last 3 years.

I would like to know if any one has opted for any prepaid plans of any full service broker, to understand its pros and cons.

It seems that, using Discount Broker may not provide us certain facilities like GTC, GTD, IPO, Buy Back Offers so it could be tough to switch to discount brokers for all scenarios. May be discount brokers are more suitable for trading for short term/mid term.

I use SBI Smart now and have used Religare (0.65% brokerage initially and negotiated down to 0.3% over time), Zerodha and HDFC Securities (0.5%). I will recommend SBI over anyone even “free” ones like Zerodha or Upstox.

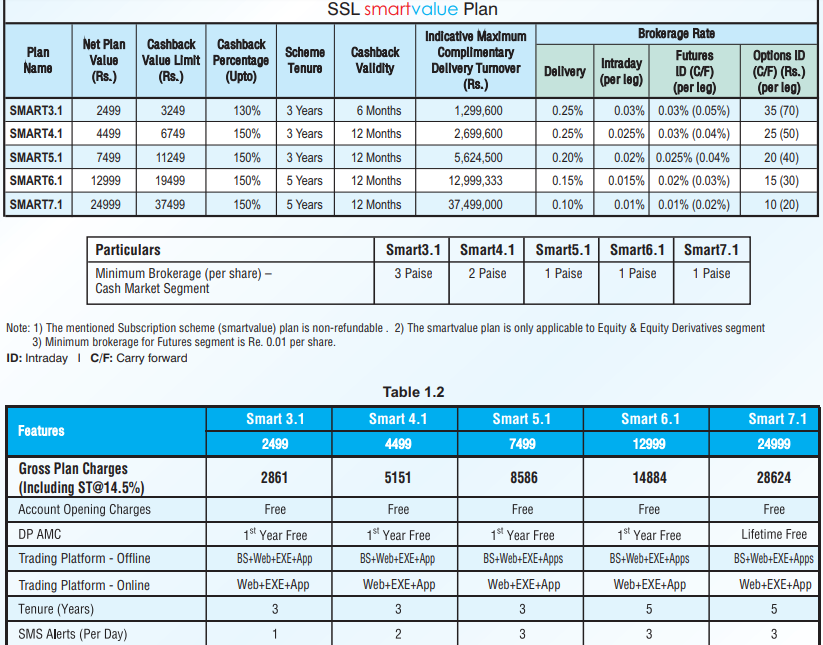

There is a prepaid plan in SBI called “SMART7.1” where brokerage would be 0.1% (all inclusive 0.24% with GST, STT, Stamp Duty and other charges) and lifetime demat AMC free. Moreover whatever brokerage that is incured for one year will be credited back to you upto Rs 25000.

Not sure if they still have this plan around. You should ask for it.

Brokerage is valid for 5 years only but got oral assurance that even after 5 years it will not be the standard brokerage of 0.5% but lesser than that.

Brokerage cashback will be credited to account after one year of paying the plan fee.

Rest T&Cs in the the document mentioned above.

Now if you don’t want to pay Rs 29,500/- (inc. GST) then if the total assets held with SBI is over a certain amount (I think it is Rs 25 lakhs, can be mutual funds, FD/RDs, demat holdings, PPF, etc) then you are eligible for SBI Exclusif (now SBI Wealth), then SBI gives a brokerage of 0.2%.

SBI may not be as good as someone like ICICI Direct (technology wise) but they are good enough and I don’t get any marketing calls or get nudged to trade more.

Why trading with Zerodha/Upstox is not "free"

No margin trading. I’m not advocating the use of leverage but it is a very convenient feature to have. Say, today is election results and you expect market to open gap down. You can place orders with having any money in your trading account and your existing stocks are kept collateral. You will pay them back on T to T+2 days without incurring any charges.

I have used Zerodha in the past and almost during any event where market is expected to be more volatile (say election results, demonetization, budget day, etc.) the server can’t bear the load and you can’t take advantage of any volatility

No features like GTC/VTC, “best” exchange orders(orders getting executed in BSE or NSE whichever was lower/higher), etc.

Funds getting credited on T or T+1 day on selling to you SB account where you earn 3.5%

Disc: I have no interest (financial or otherwise) in SBI, ICICI Direct or Zerodha.

Thanks @drgrudge, for highlighting some facts about SBI Plan. It looks quite good at only 25K pre paid amount.

I will like to have a look at this and other fees as well.

Thanks.

@drgrudge Thank you for sharing this link. This is very good information that you have provided.

@gsapte

I am using zerodha for the last 1.5 years and I have faced following issues.

Money transfer IMPS from app is chargeable and sometimes take 30 minutes for your money to get credited in account.

After selling shares, you have to wait for 3 working days to credit your money back into your account.

Not all buy backs are available on zerodha. like last month JB chemicals buyback was also not avaialble on zerodha and I had to call and email them for applying in the buyback.

the profit and loss statement for tax is also not proper. But they had just now upgraded their system. Maybe the system is improved as I have not checked till now.

The above information is based on my personal experience.

Recently Zerodha has also changed it’s policy, now all the shares bought from Zerodha has to be kept in Zerodha demat account only. Earlier people could keep their shares in any demat account like HDFC/ICICI.

What is the opinion of fellow boarders in relation to this change? Should we move back to HDFC/ICICI/Kotak and will it be prudent to keep all shares in Zerodha Demat?

I think that is an industry wide phenomenon; not an isolated one. Even SBI/HDFC/ICICI too do not permit linking their trading accounts to other demat accounts, as per my knowledge. So, much should not be read into it.

Trust in Zerodha is a subjective question, not an objective one as it depends on an investor’s perception. I am also using Zerodha for last two years, along with SBI for last one decade and HDFC for last five years, I have not faced any issues that would lead me to question the integrity of Zerodha. But it’s also true that I do not have enough information to vouch for the integrity of Zerodha or lack thereof. It all depends on how an investor perceives a broking firm and what would allow one to sleep better at night is best for himself/herself.

I have used ICICIDirect for many years & I find their web interface simple & easy to use. I don’t day trade. I always do delivery based stuff.

Recently, I opened an account with Kotak Securities & I have been using it for a couple of months & I find it rather difficult to understand.

For e.g. with ICICIDirect - if I chose “Cash Buy”, it would not allow me to place an order without first transferring enough money to cover the order. In Kotak, there seems to no distinction between Cash Buy & Margin Buy while placing the order, so I have gotten into the habit of place orders & then allocating money for it at the end of the day.

So my questions

Do they have some charges for this - i.e. as long as I allocate money on the same day or before delivery, I won’t be charged any penalty or fees for this, right?

At the end of the day, is there a way to figure out how much I owe them so that I can cover it. They have a margin report but it’s so confusing & half a page long that I can’t make head nor tail of it.

What happens if I don’t cover before delivery - will they intimate me before hand so that I can cover it?

Can someone who is familiar with the Kotak Securities interface answer?

There is no interest charged by Kotak for margin buy for two days after which interest will be charged at 18-24% per annum on a daily basis. Disabling margin trading will not help because the system still allows you to buy shares the only difference is without margin trading facility your positions will be liquidated after 60 days if you don’t transfer the due amount

You will have to transfer shares from Zerodha demat to your other demat using Delivery Instruction Slip. More details here. Zerodha will charge you 0.03% per ISIN. Not exactly a discounted service though.

Hi,

In CDSL website MyEasi system the freze option for dmat account is not working. With the freze option we can keep restrictions to the shares in our dmat account. so that broker canot sell shares without our permission orwithout our order.Even if we can buy the same company shares they will deposited into our account.In case we want sell shares of a company we have unfreeze the shares .

Please help how to use this facility.Please find the attchment.

I have one query I am assuming some of you would have done the same already.

Background: I want to open a Demat in the name of a minor (my child).

Queries:

I was told by HDFC bank that I can open a demat in the name of my child but that demat will not have a trading account associated with it. The same was written on Zerodha. I have raised a ticket to them. Is it so?

Assuming there is no trading account associated with the minor’s demat account then how do I credit/debit shares. Is it via instruction slips?

In case of instruction slips what is the usual cost? Is it what Yogesh has mentioned in the post above.

Can I have a demat for the child in HDFC and use Zerodha to credit the minor’s demat? I am assuming inter/intra depository will be allowed?

If I decide to open the demat of the child in Zerodha vs HDFC what would be the demerits/demrits of Zerodha?

I currently hold stocks for my child in my name and want to transfer the same to the child. Also it helps in having some time to think before taking an impulsive decision of buying/selling though a little costly.

You can only open a demat account and not trading account for minors.

You may gift shares by DIS (Delivery Instruction Slip) or applying in the primary market/IPOs.

Depends on the broker and whether it is CDSL/NSDL. Incoming is free out outgoing is chargeable.

No. Your trading account can’t be mapped to a minor demat account. Anyway Zerodha now requires that you have a demat+trading account with them.

It actually doesn’t matter where you open your Demat account as the charges would be almost the same everywhere since you’ll have to pay the annual AMC charges only. You should be concerned about where you are having a trading+demat account since you will pay the price (brokerage, taxes, fees, DIS related charges).

I have noticed differences in Demat AMC between different DPs. Ex. Hdfc charges 800+ while ILFS and zerodha charge less than 400.

You can buy the shares from your trading account and transfer them to your child’s demat later on at a nominal cost of around 25 rs per scrip. This can be done online as well if you register for this facility at either of the depositories.

You can transfer the shares from any demat to any demat. No problemo.