One more equity raise on the cards in the 13th Nov Board meeting.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/346fec55-df8a-48ed-a850-5dc74c39ac97.pdf

One more equity raise on the cards in the 13th Nov Board meeting.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/346fec55-df8a-48ed-a850-5dc74c39ac97.pdf

So after painful 3 quarters, Satin has reported profits

AUM now stands at 4490 cr. Mgmt has guided 5500 cr for FY18. Post QIP Book value at 189. Price/Book at 1.6.

Results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/2974df48-eda5-4156-ba42-258dc4af0ce7.pdf

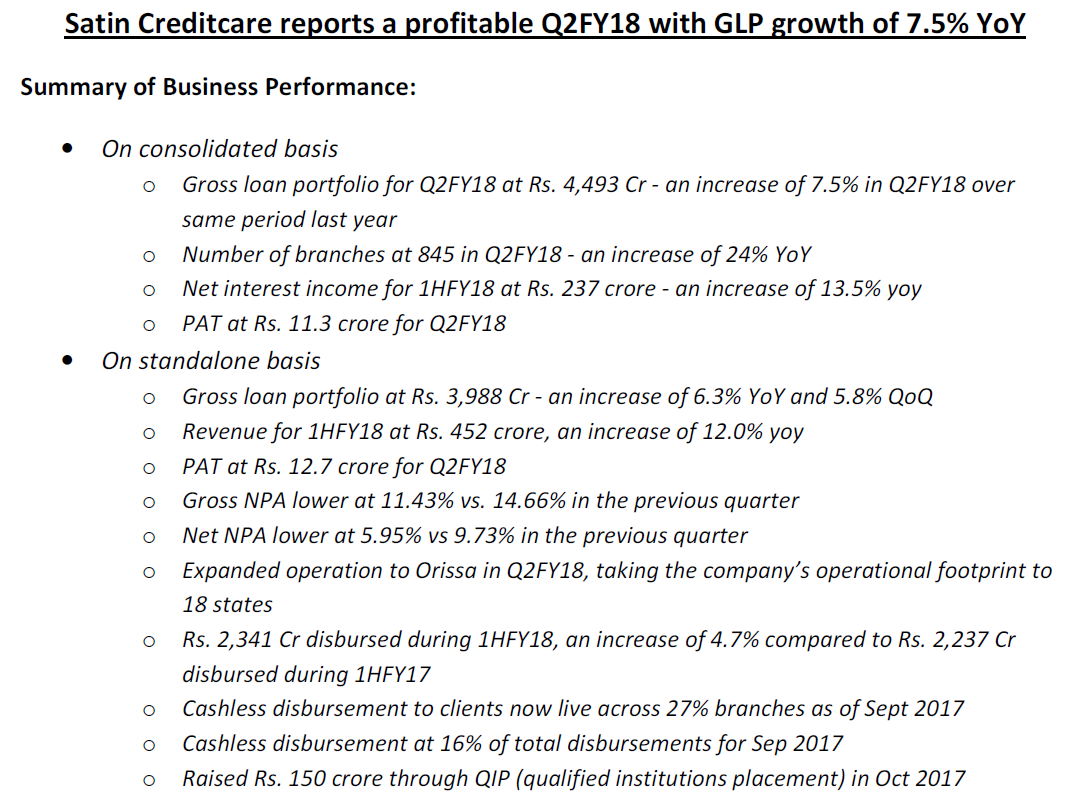

Press release: http://www.bseindia.com/xml-data/corpfiling/AttachLive/11bcd7eb-d0ea-4aec-a999-435180690389.pdf

Investor Presentation: http://www.bseindia.com/xml-data/corpfiling/AttachLive/d06d5c2d-9294-40ec-a20a-5b63ee693cd9.pdf

To put numbers in perspective, satin P/BV is 1.6, compared to ~5.5 for BFIL. Satin’s Mcap/GLP is 0.3x, compared to 1.29 for BFIL.

How P/BV is 1.6? Can you please explain? Thanks.

A GNPA and NNPA of 11.5% / 5.5% is still very bad numbers. This means about Rs550 Crores is still non performing and Rs275crs have not been provided for. That’s very high.

Agree with you if you just look at the GNPA and NNPA nos. Collections are seeing a lag effect and thats the main reason in my opinion. Most collections which happen now are perhaps being accounted as dues of previous’ months. Nov16 collection efficiency now stands at 96% from 65% in Nov16. Correct me if I am wrong.

While we can go in to accounting methods and argue whether the amounts are recoverable, it’s easier to make comparison with peers. With aggressive provisioning, Bharat Financial and Ujjivan have already brought the NNPA to pre-demonetization levels of 1%. Whereas Equitas still have high NNPA.

This just shows if Satin had followed the path of Ujjivan and BFIL, the net profit figure for the quarter will be much different (probably another quarter with a loss of more than Rs 50 crores ). In this regard, I think the results are bad and Satin is not yet out of demonetization pain.

Hi Akhil, BV as on 30th Sep is 189 rs. per share.

I attended the Q2 earnings call. Did not get chance to ask questions though (Only brokerage house folks got the opportunity to ask questions  ). Some notes

). Some notes

1- Targeting AUM of 5500 crores by 31st March 2018, and on course to achieve it.

2- GNPA on the book is about 470 crores, and for about 200 crores provisions are not made. However in the last quarter the GNPAs were brought down by about 95 crores. The management expects that they can recover more money from the leftover 200 crores. However this also means that there would be provisions made in the next two quarters as well. The amount of provisions would be a function of recovery made in the days to come.

3-H P Singh replied to a question about why not provide provisioning for all the NPAs and writeoff the bad loans.And if and when the money comes back then write back. His answer was that once you writeoff the loan then despite your best intent the actual effort that you put to recover would not be as much as it would be if you have not taken it out from the books.

4- To meet the AUM target the disbursement speed would be higher in the left over time than it’s been so far in the current fiscal.

5-Awaiting housing finance license to start operations.

6- AUM CAGR for MFI would be maintained at similar level as the current year in the coming years. However no concrete guidance was provided for AUM for fiscal 2018-19.

7- Assam and Orissa were the new geographies expanded in the last two quarters.

8- Will not hesitate to dilute equity to spur growth.

9- Would try to bring down the credit cost under 1% in the next year.

10- No issues in getting debt from institutions and it would not be a problem even with housing finance arm operational.

There is fair possibility that I may have misheard something. Please correct me. This is definitely not the comprehensive set of points discussed in the call. I have strong ownership bias.

Cheers,

Krishna

Satin has informed to the Exchange that the National Housing Bank has granted ‘certificate of registration (U/s 29 of the National Housing Bank Act, 1987) to commence business of a Housing Finance (Registration No-11.0161.17)’ on November 14, 2017 to Satin Housing Finance Limited which is a wholly owned Subsidiary of Satin Creditcare Network Limited.

What will be the impact of this license?

Satin raising Rs. 205 Cr from IndusInd, Promoters & existing PE funds (NMI and Kora Capital) at Rs. 335 per share.

Q3 Results

Presentation:

Satin reported its Q3 2017-18 results on 14th Feb. They also had the earnings call on the same day. Here are some quick extracts from the results and earnings call

1- Consolidated topline was 262.7 crores compared to 218.5 crores in same quarter last year registering growth of 20% yoy. PAT was 21.64 crores compared 16.91 crores. Please note that last year third quarter was demonetization quarter.

2- The gross consolidated AUM as of 31st Dec 2017 stood at 4881 crores. They are on track to meet the AUM of 5500 crores by 31st March 2018.

3- Gross NPA on consolidated AUM was 394.8 crores or 9.17%. Net NPA was 148.8 crores or 3.67%. Thus provisioning coverage ratio stood at 62.31%.For all zero collection clients full provision has been made. PAR1, PAR30 and PAR90 have seen consistent and meaningful drop over the last two quarters.

4- There was recovery of 61 crores bad loans during Q3-2018. However recovery from here on would be difficult but management is not giving up on it. There was no guidance on the money that can be further recovered, but looking at the past it would not be very optimistic to assume that at least another 50 crores should come back over the next two quarter( please note that this is my assumption and management was tight lipped on that).

5- Collection efficiency stood at 98% for the loans disbursed after 1st Jan 2017 (post demonetization era). The zero collection clients have decreased to 62K as on 31st Dec from 81K as on 30th Sep. This number has further decreased by another 4-5K in the last 45 days. Indicating that some more recovery of loans is happening.

6- Cashless disbursement stood at 26% in the quarter and it would hit 50% by 30th June.

7- There were two question related to social/economical unrest. Impact of loan waiver in Rajasthan and disturbance in a specific part of MP over the last few days. Management clarified that loan waivers do not have impact (in fact the collections increase as called out by management in the past). The unrest in a focused area of MP is factual but not overly worrisome.

8- There were questions asked on why collection efficiency is lower than other MFI (read Ujjivan, BFI and Arman) players. H. P. Singh clarified that they own the business in the states where there was maximum impact and they are coming out of the woods. Give couple of quarters and things would be ok. They have been offsetting old loans when they recover money from a client because unlike other players they did not write off all the bad loans. Because of this there collection efficiency may optically look slightly lower than others.

9- Five years from now then would like to have one third business coming from MSME and other segments, and two third coming from MFI. In housing their focus would be to provide loan to underserved segments where competition is less. One interesting point made by management was that while funneling loan clients for Reliance they have acquired ground knowledge and know what they want to do.

10- NIM to remain stable around 10%. The AUM growth should be 35-40% over the next year. More concrete guidance to come at the end of next quarter.

11- There is no intention of any further equity dilution at least over the next one year.

12- Answering a question Mr. H. P. Singh mentioned that he would aim to bring the credit cost under 1% in the next year.

13- Book value per share at the end of 31st Dec 2017 stood at 213.84. The CMP discounts it by 2.13 times. Not apple to apple comparison, but Ujjivan’s CMP discounts BV by 2.56 times and BFI by 5 times.

There is fair possibility that I would have misheard/misread something. Please correct me. This is definitely not the comprehensive set of points discussed in the call. I have strong ownership bias. This is not a buy or sell call. Please apply your judgment before any transactions.

Cheers,

Krishna

I still think sector as a whole has a long way to go. Satin has been the worst performer in this sector. Huge equity dilution and still 10% GNPA is quiet bad. Arman and Ujjivan are faring much better.

As they say, best time to invest in a sector when everyone has given up on it. This is a growth+rebound story.

Status: invested in satin, Ujjivan and arman.

If one is averse to equity dilution, he should stay away from lending business. Growth will always come with dilution of equity. Satin has raised equity for aum upto 10000 cr, so they are good to go for next 6-8 quarters. Arman will do same by Q1 of next year.

Not ‘only’ related to Satin but in general to MFI and banking sector, Bandhan Bank seemed to have received the nod from SEBI for their IPO. They plan to raise 2500 odd crores from this IPO. More details can be found here https://www.moneycontrol.com/news/business/ipo/bandhan-bank-gets-sebi-nod-for-rs-2500-cr-ipo-2521673.html

In the middle of all headwinds for the MFI sector this IPO should augur well at least from market sentiment perspective for companies like Ujjivan, Equitas, Arman and Satin.

Cheers,

Krishna

Its been observed that the company is almost paying 85% of operating profit as Interest since a decade. Whats the logic behind retaining such huge interest burden? Even if it plans to bring it down by 50% or so by not going aggressive on the expansion it can double\triple its bottom line without doing anything. Why it isn’t treading that path? I am not asking it to curtail the expansion plan, all i am asking is modest its aggressive plan of growing by 30-40% on top line for couple of years. Once the debt comes down drastically(there by increasing its credit profile and there in reducing your COF which will further help in expansion), it can always hang on to 30-40% CAGR on bottom line as well as top line. Why not tread this path? When the current norm is not working, why not think about out of the box thinking and achieve what we want achieve?