The amount raised in rights issue was very small compared to annual profits of the company.

There was no actual need of the rights issue for such a small amount in the first place.

Any CA can confirm I guess or correct me if I am wrong.

The amount raised in rights issue was very small compared to annual profits of the company.

There was no actual need of the rights issue for such a small amount in the first place.

Any CA can confirm I guess or correct me if I am wrong.

While it may sound bit harsh, but if you find the company is not fit into your investment parameter, for whatever reason, just ignore. If you have something negative and want to check, it is perfectly fine. Now talking about intent of management, the managment past conduct has been reasonably clean. Please read the thread from beginning about treatment of management to shareholder/ employee and with state. They use to provide fixed price ration to their workforce in past which was charged to P&L. Considering the past long history of fair treatment to various stakeholder, now to raise concern about managment conduct and decision, I think we need some solid reasons for being watchful. This is my opinion and may be wrong. While we all shall be watchful and careful, but we also need to take calculated risk on management in stock market. Every management would have some negative points. We need to take collective viewpoint based on our requirement and risk assessment. In case we find, the conduct of management doubtful, we shall ignore and focus on other 2999 listed companies.

To be specific about your query, I do not have answer about why right issue were raised. However, based on my past working, at least in my understanding, the managment is unlikely to do right issue at price of Rs 10 and increase stake by 1%. They could easily do private placement throughtwarrant and other various ways (like merging group companies/ hiving off assets) which are more simpler way to increase their stake by larger percentage than just 1%.

I think we should not bring emotions in investing.

There is young and new management of sandur- so, previous track record is immaterial.

this is a discussion forum, and I have full rights to ask questions.

If you don’t have an answer, typing a very long paragraph will not help.

Value of 1% stake acquired by management at Rs. 10 = 40 crores.

Amount raised by rights issue = 18 crore.

Basically, the company got 18 crores cash, while the management got shares worth 40 crores at throwaway prices.

(1% of 4000 crores is 40 crores)

Also, the 18 crores raised from rights issue was very small amount vs total annual profits and there was no real reason to do rights issue.

And, still you want to believe management is honest?

I rest my case

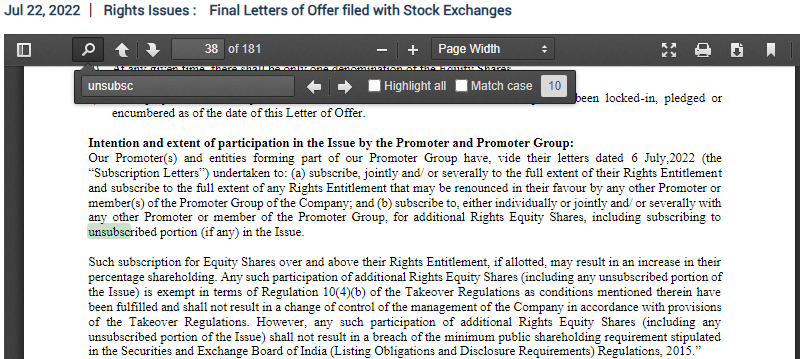

The 1% stake acquired by management after minority shareholder failed to subscribed their porttion of right issue of Rs 10 per share. So, it is not that management allotted themselves shares at Rs 10 and not given opportunity to other shareholder. In fact, right issue offer document categorically has disclosure that in case right issue remained unsubscribed by the other shareholder

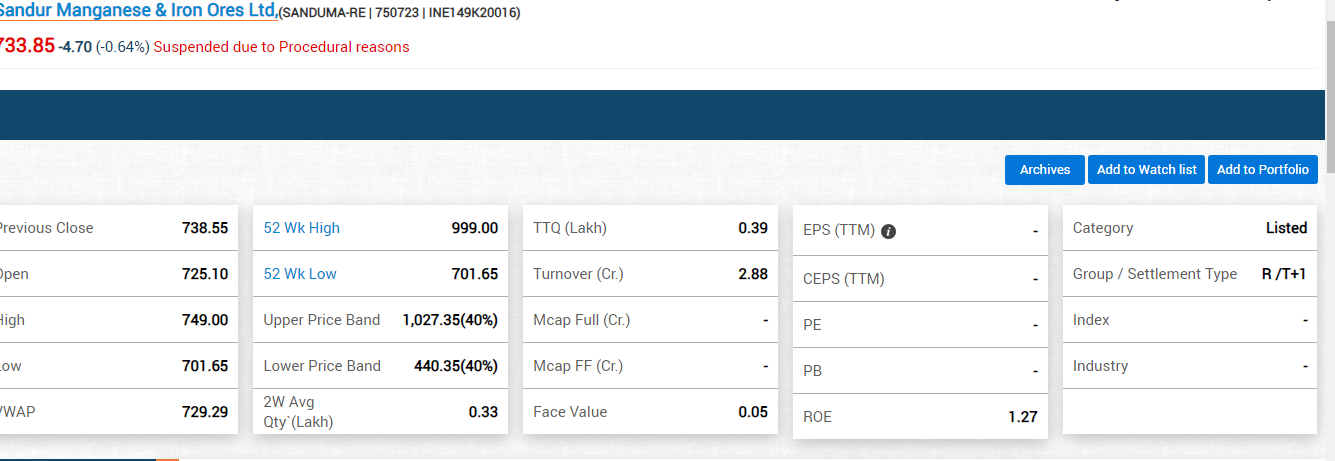

In case minority shareholder have no cash to subscribe, still s/he could have sold his/her entitlement in secondary market and get his/her share of benefit of rights at lower price. Enclosed BSE trading screen for Sandur Right entitlement.

I believe this are sufficient disclosure and hence consider managmeent clean in my understanding. Further, shareholder also got option to subscrite in right at same term and also encash their entitlement in secondary market (in case having on interest to subscribe to right). If they are not watchful, at least, management shall not be blamed for their inaction in my view.

Finally, We shall agree now to close discussion on this point and continue hold diverse view about management, which is fine in my view.

sure, this will be my last message here.

The management and even most astute investors know- that quite a few retail shareholders are sleeping shareholders- they don’t apply to rights issue etc due to lack of time or lack of knowledge.

The management knew this- and did the rights issue- knowing that some of the shareholders will not apply to rights issue.

18 crore raised was very small amount vs total annual profit of the company, and hence no real reason to do rights.

There was no logic to have right issue. An active investor also had to keep a track of the dates when rights would be available for application and it becomes difficult to track. For retail shareholders who do not track market, it is impossible and in my opinion it was not a prudent decision by company to have a right issue.

Fund raising doesnt seem to be the intent here.

There is no point in defending management here.

I am invested in Sandur (in small capacity) but cannot justify this action of the management.

I have seen mutiple companies which increase equity base by way of bonus/split to improve trading. On specific reason could be to get listed on NSE also, which is more liquid than BSE. Now, it is possible that same can also be achieved by bonus issue. However, the companies which are very old (like Sandur which registered in 1954), the bonus shareholder would also get in hand of inactive/deceased shareholders and hence may not result in improve liquidity. That could explain Right at such terms (2 share of 1 share held at price of Rs 10 per share). I am personally director in company which is registered in 19th century and faced that issue. So at times, what appear as unfair treatment to minority shareholder, may not be necessary be the case. I may be wrong in my assessment, but just wanted to present another perspective.

Last but not least, the shareholder who are not following up their investment need to really careful. After seven years of non-receipt of dividend, shares would get transferred to IEPF and as per new SEBI act, shareholders who have not provided KYC details to companies/RTA by 30 September, their shareholding would be frozen. More details are enclosed in case anyone interested. https://www.sebi.gov.in/legal/circulars/mar-2023/common-and-simplified-norms-for-processing-investor-s-service-requests-by-rtas-and-norms-for-furnishing-pan-kyc-details-and-nomination_69105.html

Bonus/split is the right way to go for liquidity.

Every company does bonus/split for liquidity.

There are 8000 listed companies- I haven’t seen other companies doing such rights issue to increase liquidity. so, that’s a totally absurd reason.

your reasoning of not going for a bonus by sandur is very awkward and doesn’t make sense.

Also, suddenly, you have changed your answer on the reasoning of rights isssue.

We know that management got 1% extra shares worth 40 cr at throwaway prices.

also, iron ore mine lease will expire in 10 yrs.

the profits of iron ore mining will anyway suddenly vanish 10 yrs from now.

There are many other companies- GPIL, sarda energy- which are also excellent companies in same space.

I don’t see why sandur deserves such a favorable treatment after such a rights issue by the management.

Heritage Foods is also another which has done such Rights issue in recent past.

There are also cases where promoters are drawing high salary when compared to Net Profit.

Both above activities are wrong from management quality point of view. As Ayush Mittal Sir say, If they are taking high salaries, at least they are taking upfront. Atleast they are not siphoning of the money.

Such Right issue are also similar case. Atleast they are doing upfront.

As Investor we have to Live with it and be super Cautious by investing such companies. Such cases if are happening very often then its a Big red flag.

I would like to add my two cents here, I got 50 shares extra than rights entitlement at 10 rs, so I do not have any problems with management, but business I cant be sure, holding 50% of my initial investment

Board recommends Bonus Issue in the ratio 5:1

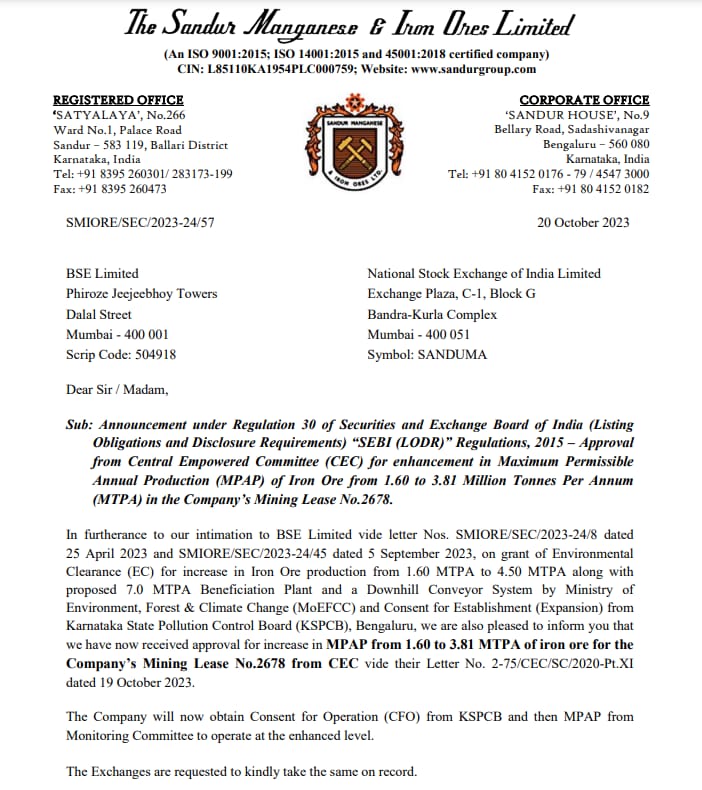

Might be the reason -

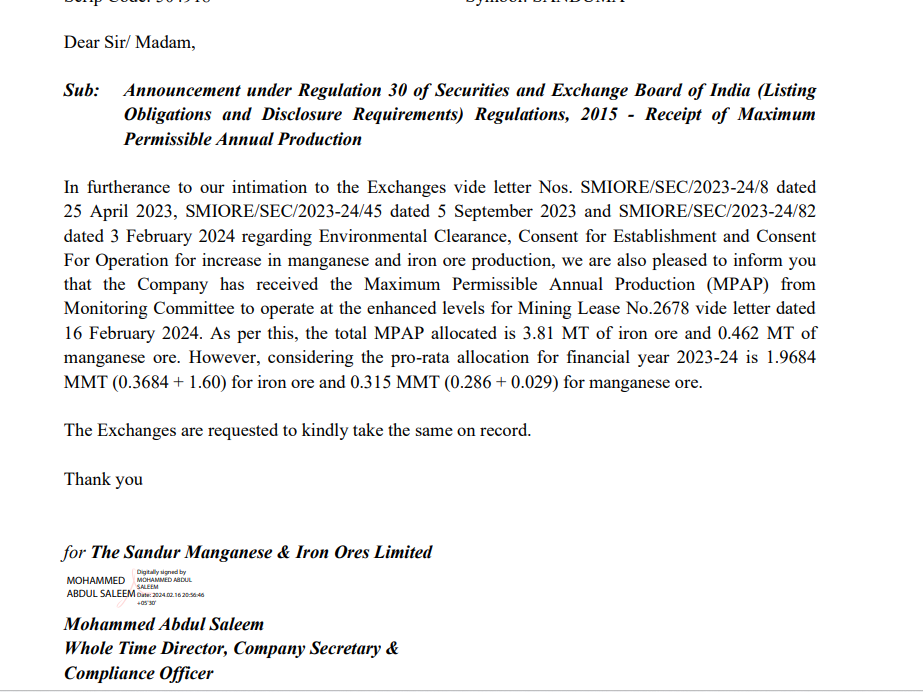

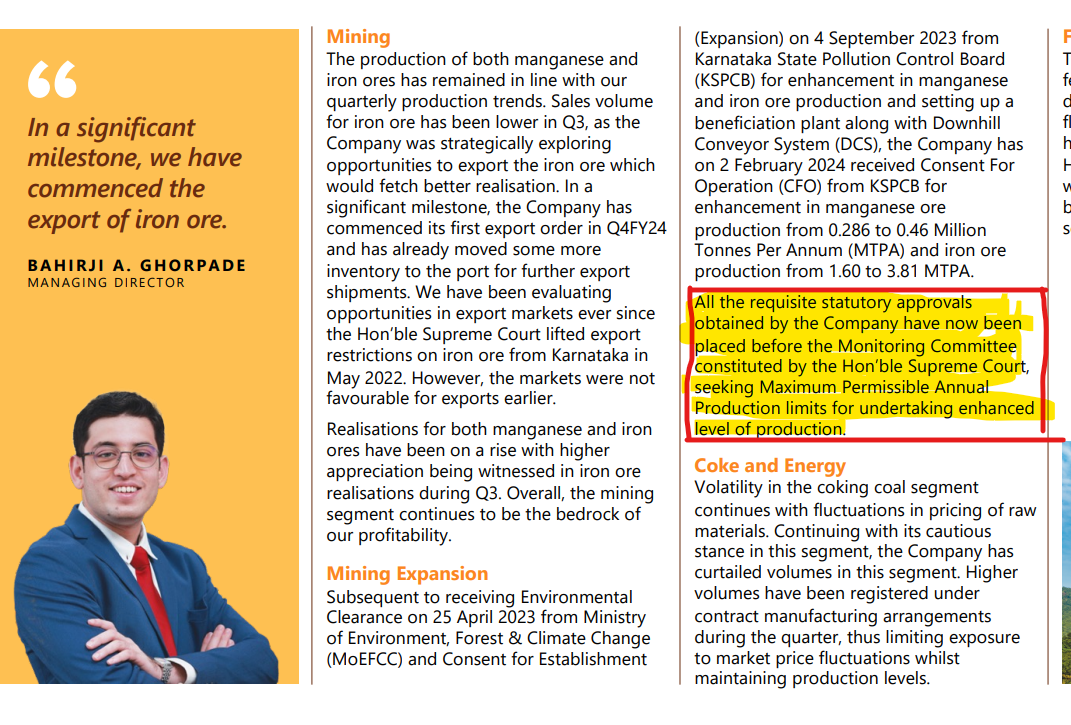

The company has received the Maximum Permissible Annual Production to operate from monitoring committee which the management has told in Q3FY24

(Attached both)

Hi Rohit,

I track the stock- not too sure on why it tanked, probably the price had run up quite a lot in a short period.

They should do a PAT of 800-1200cr for the full year in FY 25 ( depending on the iron ore prices) so the current price does look very attractive.

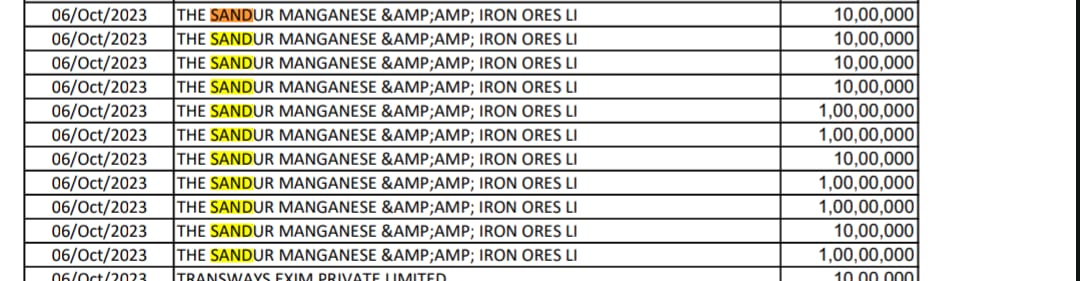

Was going through the electoral bonds list released today and this showed up.

Very interesting that this came two weeks later.

Disc: Don’t own. Shared because I found it interesting. P.S. I know that this is how business runs in this country unfortunately.

Hi @baniyainvestor,

Could you share your numbers here?

Your numbers look too ambitious considering the expected FY24 numbers.

Acquisition: Sandur acquired Arjas Steel private ltd

07b53897-1fdc-4fbb-84af-0b4fa5b54d57.pdf (314.9 KB)

From what I’ve read so far looks like a good move… Here is the hypothesis

Arjas has a capacity of 3L tons ( including Modern steel plant in Mandi gobindgarh ~4L tons)

a) Profitability perspective: Per a CRISIL report they did a PAT of 200cr on a topline of 1500 cr in 2021…Assuming normalization of the steel cycle on the company disclosed topline of 2800cr they should be doing 200-300 cr of PAT.

b)Valuation based on capacity: VSSL a close competitor has a capacity of 1.75 L tons and a mcap of ~2000 cr so by that logic also the price seems fair

Future expansion: Based on news articles Arjas is planning an expansion at both existing plants to take new capacity to 5.5 L ( which should translate into a topline of 5500cr in 1-2 years)

However all of the above is conjectural and very outside in. Will wait for the management to share more details.

Disc: Invested and super biased

Hi All,

Sharing the video of Arjas steel plant…it looks quite good. Though its a 5 year old video…but good enough to get a sense of the asset that Sandur is acquiring.

Regards,

Yogansh Jeswani

Disclosure: Invested for self & clients

Hi

This acquisition looks like a very good move by the management due to obvious integration benefits. With ming expansion and stabilizing realizations, company should do well on margin and bottom-line basis. However, management previously guided their interest in expanding into pig iron and DI pipes. Any idea on that?