Enterprise Value is 12,100 Cr. (includes Debt and any other liabilities). Also, NINL includes a captive iron ore mine and huge tracts of land (then can build 5x capacity) which needs to be adjusted to get a correct figure.

But still basis this also - SAIL is atleast 4x under priced.

3 Likes

The debt reduction of 3350 crs is more than the entire Depreciation+PAT= 1048+1529= 2577 crs. Seems like both the CAPEX and the excess debt reduction were funded by payment of receivables.

Any idea why there was a spike in the Employee expenses. Didn’t they provision for the increase in the employee expenses in one of the past quarters at once?

2 Likes

Does anyone know where I can find the Q3 FY22 Concall? It is not there on trendlyne YouTube.

I dont understand why SAIL is falling even at a PE of 2.88 ?? What am i missing?

4 Likes

All metal stocks are down due to lockdown in China, Lockdown in china would result in subdued demand. to be honest the metal stocks movement is totaly irrational, most sensitive sector to any global news

1 Like

Given the news that Russia will provide India with commodities at discounted prices, and that since Europe has imposed heavy sanctions on imports from Russia, if the coking coal supply comes from Russia to India, and Europe cannot import from Russia, won’t we have a situation of lowering of input costs for domestic steel companies but steel prices remaining elevated in Europe and the world? As the steel companies have already taken a price hike, due to sufficient coking coal inventory, the margin pressure won’t come until June(got this from interview of Tata Steel boss). And we also have some news of lockdowns in china, further reducing the supply.

So as a result if coking coal is imported from Russia, won’t the Steel companies will be benefitted from this fiasco? A great export opportunity to Europe is up for grabs don’t you think?

7 Likes

The daisy chain thinking of yours is impressive!  upvoted! I agree with the overall idea that steel prices and profits should remain high not quite all the reasons behind it.

upvoted! I agree with the overall idea that steel prices and profits should remain high not quite all the reasons behind it.

If you look at cost structure of SAIL vs private players, you will notice that SAIL is less efficient then other players. One of the contributors to this high cost is Employee Salary (being govt company, it is obvious it will not be as efficient on this part). There was also some discussion/pending action on salary hikes etc… This and some other factors are likely to weigh heavy on margins of SAIL for next few quarters…my guess is (and I could be wrong), this is one of the key reasons for stock price under pressure.

SAIL management did a meeting with Omkara Capital some time back. Video of the same is available on YouTube. You can check it out for inputs on employee cost and other cost parameters

3 Likes

But that has always been the case right? That’s what the psu tag means. The reason sail looks interesting is because of the debt reduction. The gross debt remaining is just 19000 crores. This is around the same levels as it was in 2010…when the stock price was 280 and the company had even less capacity with no modernisation. Even then the company now trades at a price around 30 rupees below book value and a price to sales value of well below 0.5. Once the debt further reduces won’t these ratios normalise? At least that’s what I think.

The current debt to equity ratio is 0.42 vs Tata Steel’s above 1.

The operating profit margin of both companies is the same (consolidated). So there no such problem of incompetency.

The undervaluation is what bugs me, debt free PSU companies such as NMDC and NALCO trade well above book value and price to sales, as does Tata steel. So the market already has differentiated Sail and Tata Steel.

Isn’t it time for sail to shine again? I may definitely be wrong and would love to get other views on the topic.

8 Likes

Very valid points. Must admit I am out of my depth to answer questions you have raised.

Just one small input on the point of debt reduction. Long back when I had read Basant Maheshwari’s book (The Thoughtful Investor), he had written that market rarely gives extra premium for improvement in profit due to debt reduction.

I think your questions deserve more research or inputs from more experienced folks in this area. I clearly don’t have much to add.

1 Like

3 Likes

Hey everyone,

I was going through the recent developments in steel space.No doubt, the export duty hike looks very disappointing from an investor perspective but the valuations , combined with the overall debt reduction in various companies doesnt look typical of a sign of a top in the sector.

Also, in case of SAIL I was looking at the EV vis a vis the replacement cost of steel plant and assuming ~6K Cr. for 1MT steel capacity, 21.4MT steel existing capacity, the EV should come to about 1.28L Cr compared to about ~44K Cr currently. That looks like a good bargain to me but just wanted to understand from some of the more knowledgeable industry person on the forum to understand if the ballpark 6K Cr /MT looks correct.

I have gone through some of the articles from Mr. Rakesh arora for the same and understand that there might be short term pain left due to the news flow. But, from long term perspective (~3Y) the investment seems good to me.

Happy to hear thoughts/opinions on the same.

Disclosure- Was already invested in the stock, Avg price ~95. Looking to add more.

3 Likes

I think the SAIL management has done well by taking advantage of a boom in the steel prices in 2021 and 2022, by reducing the debt. Rs. 38,557 crores of debt has been paid back in the last 2 years as seen in their balance sheet of Mar 2021 and Mar 2022 (Source: screener.in)

Therefore even though steel prices have cooled off a bit, I believe that SAIL will continue to do well.

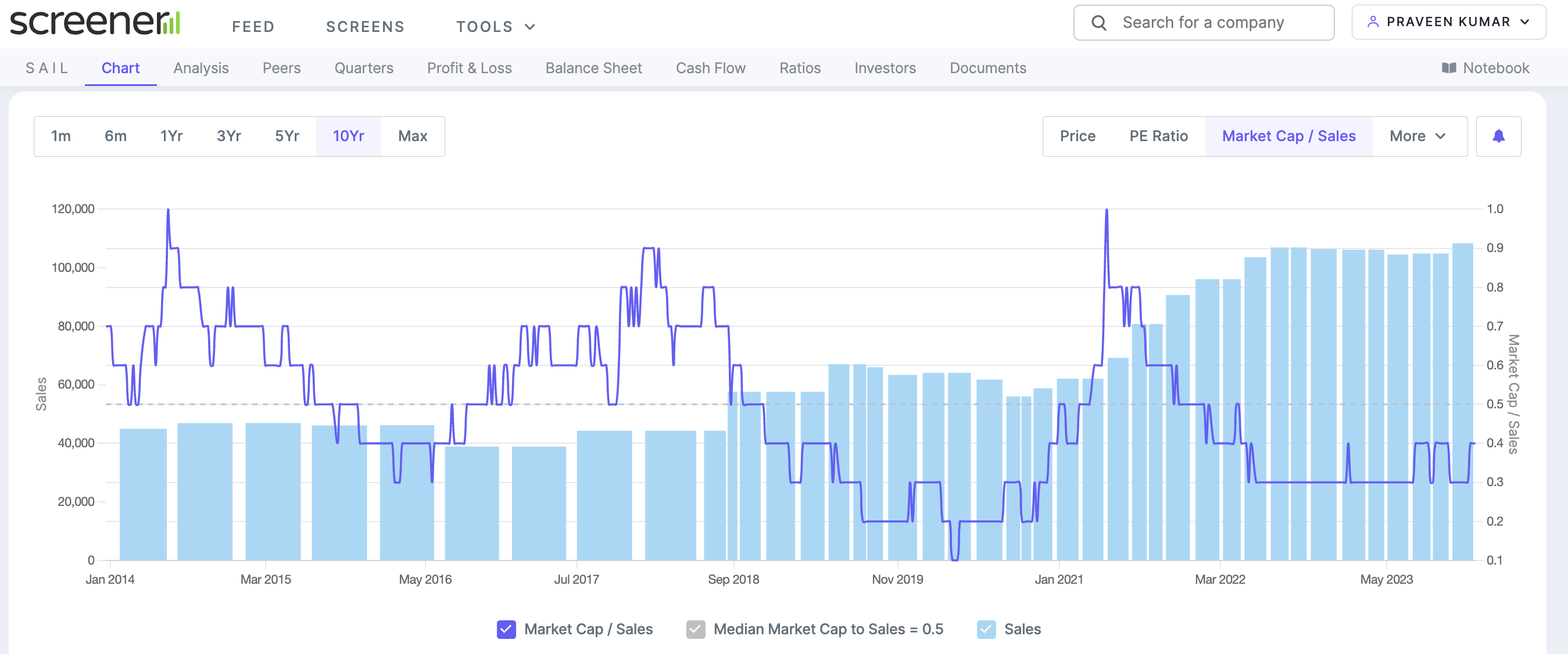

Their current market cap to sales ratio of 0.3 is much below their historic value of 0.5. Plus their dividend yield at current prices is ~12%, which offers good margin of safety. While their price to book ratio of 0.6 is in line with long term averages, this has to be looked in context that these are fairly depreciated assets because SAIL has not undergone any major capex in the recent years.

From the management commentary, SAIL seems to be inclined towards investing incremental capital in modernisation and value added steel instead of merely adding more volumes (Disc: SAIL / NMDC / JSW Steel / MECON are clients of my business).

Peter Lynch’s theory of exiting commodity businesses at low P/E multiples (SAIL current PE is 2.5) might not be applicable in this because this theory hinges on increase in supplies as a key reason to avoid investing in low PE commodity stocks. Whereas, there hasn’t any huge increase in domestic supply despite the booming steel prices in the last 2 years.

Thanks to all the ESG activists and perennial problem of land acquisition, setting up a greenfield steel plant is a huge challenge. For example, NMDC Nagarnar Integrated Steel Plant in Chhattisgarh is under construction since over 10 years and yet not fully functional. Another initiative by Andhra Pradesh Government - Kadapa Steel Project is also languishing only on paper for the same reasons of land and environment clearance (and therefore no interest from investors). Please read YSR STEEL CORPORATION LIMITED to know more.

Most of the capex in this sector has gone into acquiring existing steel assets (Essar Steel, Bhushan Steel, Bhushan Power & Steel, Asian Colour Coated Ispat and the most recent Neelanchal Steel). Meaning, the market has only got consolidated, making the existing players much more powerful.

After the IBC process, the steel market has consolidated heavily in 4-5 players. If you see product wise consolidation is just within 2-3 players (Example: JSW Steel controls over 50% market share in galvanised steel, SAIL-JSPL control the railway steel market, etc.).

Add to that, the government’s rule of ‘Make in India’ and contractual preference to use domestic iron & steel for all government infrastructure projects means the domestic players are relatively insulated from steel imports. The policy document can be read here:

https://steel.gov.in/policies/policy-providing-preference-domestically-manufactured-iron-and-steel-product-govt

A lot of people think that steel is a pure commodity business. That is far from true. Manufacturing capacities are designed for specific purposes: Cold Rolled Steel, Hot Rolled Steel, Wire Rods & Bar Mills, Structural Steel, Blooms, etc.

You cannot change the plant design in a short period. For example, there is no ways that a rolling mill making steel sheets is going to manufacture structural steel just because the product demand has shifted to another product.

I feel that the fall in prices of steel players is overdone. Factors at play:

- Massive debt reduction

- Major consolidation of capacities (especially product wise)

- Make in India push by GoI

- Intelligent capital allocation by existing player by buying out weaker players, investing in modernisation instead of over-investing in greenfield capacity addition

Disc: Invested in SAIL, Tata Steel, NMDC

20 Likes

- Margins are likely to increase in Q3 FY23. Imported Coking Coal cost declined which will be realized in Q3 FY23. More drop in coal consumption cost is likely.

- Q4 FY23 might see some increase in costs leading to reduced margins.

- Debt Guidance: Plan to reduce Debt levels by Rs. 25000-26000 crores by March’23 which is still more than FY22 debt levels of Rs. 13800 crores.

- Capex Guidance: In H2 FY23 capex will be 6000 crores which will be spent on coke ovens, casters and other small projects.

- FY23 production guidance is 17-17.5 MT and sales guidance is 16 to 16.5 MT. For FY24, the saleable steel production target is 18.5MT.

- Employee cost to remain flat.

1 Like

This straight away increases the quarterly EBIT by 15 crores. Additional benefit on interest and depreciation.

Insignificant, though just goes on to show the intent of the government.

2 Likes

Dear VPers

Eventhough I don’t have any clue on how the margins of Steel companies would play out and how the overall cycle plays out, Price wise SAIL is moving up (weekly chart below).

I see the same trend for JSW steel and Tata steel which are at 52 week highs

I have some expectations on the cycle turn around and peak going by previous cycles. From the P/S chart below one can see that the peak P/S is 0.9-1.0 and the Peak to Peak takes 3-3.5 years.

So, If we expect the cycle to peak after 4 years from previous peak (May 25) the return expectations would be good. But that may not be possible until China economy (construction) comes back strongly. So, I assume that the cycle peaks only in 2 years from now.

My assumptions (expectations ) as follows

Sales = 1.2 lakhs and P/S= 0.85 implies the Market cap would be around 1 lakh which would be more 2.2x from current market cap

Disc: Have small exposure. Bought in last 30 days and may buy more

Praveen

1 Like