Input costs continue to put pressure on margins. Encouraging to see the stellar yoy growth in topline (29%) indicating that the the co seems to have found some new pocket of growth. Yoy Gross Margins are at 40% v.s 44% and operating margins are at 8% v/s 13%. The robust growth in revenue indicates that the co is doing well in capturing market share. The good growth in gross profits (18%) is also indicative of the business being executed well strengthening the co franchise despite the rise in input costs. Lets see how the market reacts to these results tomorrow to get further cues.

Best

Bheeshma

Anyone attend AGM? Please share notes.

VIP tried to smoothen this quarter GM margin impact by using a mix of old (high price) and new (lower price) inventory. Yes you read it right; please read the concall transcript. Surprised nobody is talking about it.

Will be curious to understand what Safari did.

Safari FY19 AGM Notes

I asked more or less same set of questions that I asked for VIP. Following is summary.

Mr. Jatia is very comprehensive & to the point in answering most of the questions.

Mr. Jatia Speech

- There is thrust to grow the polycarbonate bags & backpacks.

- eCommerce & hypermarkets are the fastest growing channels & the company will be focused on these channels.

- There will be another expansion at Halol in Q3/Q4 FY20.

- The company has filed application with NSE for listing & it might be done over next 30 days.

Competition

- The company’s aspiration is to become #1, it might take 10-20 years. He said he gets kick out of trying to compete with world’s no. 1 luggage company & India’s no. 1 luggage company.

- He agreed that VIP, Samsonite are much bigger players but he said Safari is also 45 year old brand which never got damaged.

- One of the weakness of the company is it has no EBOs compared to other two players.

- He claimed that the competition has been intense in last 12-15 months & currently competition has priced products below the Safari rates.

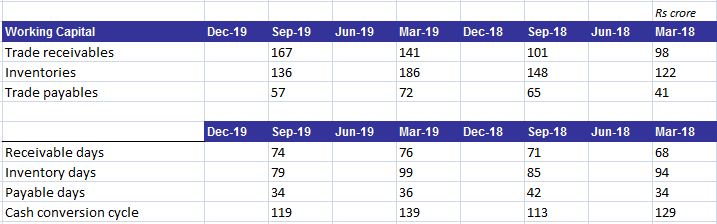

Working Capital

- Mr. Jatia candidly accepted that negative OCF has been a problem ever since he took over the company. He feels that there will be improvement in WC when Sept balance sheet comes out. The March quarter WC looks elevated because CSD did not make any payments, adjusting for that receivable days have not seen much deterioration.

- The improvement in WC would be due to increased India manufacturing + sourcing. In FY19, sourcing from India is ~30%, he is hoping to take it to 40% in FY20.

- He also candidly admitted that they have not been able to negotiate any major reduction from Chinese suppliers despite US-China trade war causing soft demand for Chinese players.

Capex

- The company will be doing capex of 35-40Cr for warehousing, racking etc, in the second half of the year.

Products

- He said that people have tried doing specific products targeted at wedding & it has not worked. It’s a difficult thing to crack.

- The company has 1800 SKUs.

- The distributors are exclusive to Safari but end dealers, retail touch points are same. The penetration with dealers is more or less similar but extraction is less.

Brand

- The brand philosophy is to make it younger.

- He candidly admitted that he does not understand digital.

- On brand spends, he said the order has to be Products -> Distribution -> Brands & can not be any other order. They will keep investing in above order, there is no magic formula to it.

Others

- The company’s rating might improve in coming days as they are working with CRISIL. it might help in reducing cost of borrowing further.

- The company had taken enabling resolution for QIP of 100Cr & would go for it when stock market improves. Currently nothing concrete is on the table.

Disc - token position to attend AGM, not a buy or sell recommendation. Please do your own due diligence. Not a SEBI registered analyst.

EBO is acronym for exclusive brand outlet

by Angel broking

Link to the report:

Why have u taken tailwala plastic and co hold co for samsonite… they are completely two different companies…

Tainwala chemicals plastics holds a major chunk of shares in Samsonite, thats why its taken and samsonite growth is played via tainwala chemicals

Appreciate your work on this.

I did a small exercise today related to that in Bangalore.

In my sample, I have visited about 3-4 unorganized stores.

And among branded stores, have visited VIP and Samsonite.

All in the area of Marathahalli flyover in Bangalore.

Unorganized Luggage vs Organized Luggage:

In Soft Luggage, the price differential is way too high. That is about 100%+ kind of differential. However, the quality difference is also way too high. If you go to better quality ones in unorganized, the price differential is still at 50%.

In Duffel Bags as well, it is high but about 50% differential. A bit better compared to soft luggage. But again, I can see steep difference in quality here. Better quality bags from unorganized have price differential of not more than 30%.

Talking of hard luggage, I couldn’t find much hard luggage products with the unorganized people. I’m not sure of the reason. Will probably find out if I stop by that place next time.

Both VIP / Skybags & Samsonite / AT have great products in all the three segments.

Unorganized Backpacks vs Organized Luggage:

Backpacks was relatively interesting as the price differential is quite low at about 20%. Like I could find some Skybags starting at 1200 or 1300 while also see some unorganized players trying to sell bags with random brand at 1200. (Both prices after discount / negotiation.) Of course, there are backpacks selling at 600 / 700. But their quality is very poor in comparison to Skybags. And at the same time, Skybags can cost you upto 3000 too if the value-add of that bag is higher.

So to summarize,

Soft Luggage: 50%-100%

Duffel Bags: 20%-50%

Hard Luggage: -

Backpacks: 10%-100%

Please note that my sample might be biased. And there is a possibility of human error among my notes.

Discl: I own a bit of VIP. Might consider adding more. Please do your own due diligence. Not a buy / sell recommendation.

Good analysis

Results are a mixed bag. Cash flow has improved however expense ratio has increased leading to flat earnings pretax. The tax cut has benefited the co . Top line has improved by 31% yoy. Gross margins have also improved to 44% from 42% yoy. The employee exp at 12% of topline remain stable indicating that the co continues its plan to increasing reach and volumes over margins. This also indicates the competitive intensity in my view. There was also an increase in finance costs indicating some pressure on channel liquidity which contributed to the decrease in pretax margins. That said, working capital mgt has emerged as the differentiator in luggage cos. The co has done well in managing it’s requirements on that front but the nature of the industry prevents it from being another VIP at least as of now.

Technically, while there was an uptick in the stock price post results it failed to break any recent intermediate highs corroborating the results. The stock price has been drifting downwards for a while now.

Best

Bheeshma

P.S : no holdings

Bulk deal on BSE:

| 22/11/2019 | 523025 | SAFARIND | ASHISH KACHOLIA | B | 218,000 | 550.00 |

|---|---|---|---|---|---|---|

| 22/11/2019 | 523025 | SAFARIND | SAIF INDIA VI FII HOLDINGS LIMITED | B | 578,992 | 540.00 |

| 22/11/2019 | 523025 | SAFARIND | TANO INDIA PRIVATE EQUITY FUND II | S | 1,070,000 | 544.07 |

At the cost of sounding like a broken record, while safari is helmed by an able mgt the working capital position of all luggage players in the industry has deteriorated. No player including VIP is able to generate sufficient cash and WC borrowings have increased quite a lot in both VIP and Safari. Safari will need to take a capital infusion in the near future. Safari continues to be on my watchlist with a good growth in topline however I feel that along with topline growth one must also look at balance sheet quality to deduce the quality of earnings and on that front Safari at this point does not seem to be placed well. We have seen this happen in Mirza where the WC intensity in the entire industry increased suddenly due to stiff competition leading to a margin erosion.

Quite surprised at the fall in revenue growth - from a ~30% avg growth in H1 down to 14 in Q3, while margins have gone up by quite a bit.

Similar trend seems to have played out for VIP as well, where sales growth is now down to 0% (though it was already slow in H1 at ~6%) while margins have jumped quite a bit.

Seems like both players have negotiated well with Chinese suppliers recently - can’t think of any other reason given that they could not have hiked prices in this environment and a mix change could not have impacted margins so much for both (please suggest if any alternate theory likely).

In this scenario, given sales have fallen so much I don’t see how both players would be able to maintain margins at this level. I’m guessing last quarter with the festive season would have been better for business and no signs of any short term uptick in the economy or consumption, would put further pressure on sales.

Add to this potential supply disruption in China in the near term, on the back of coronavirus impact, could put further pressure on supplies and increase costs for both players. Maybe more of an impact for Safari than VIP given the relatively higher dependence.

Additionally, equity dilution could also be on the horizon to fund growth. Valuations are also not really cheap currently at these levels.

Struggling to see a brighter side to this story currently.

Request others to add their thoughts.

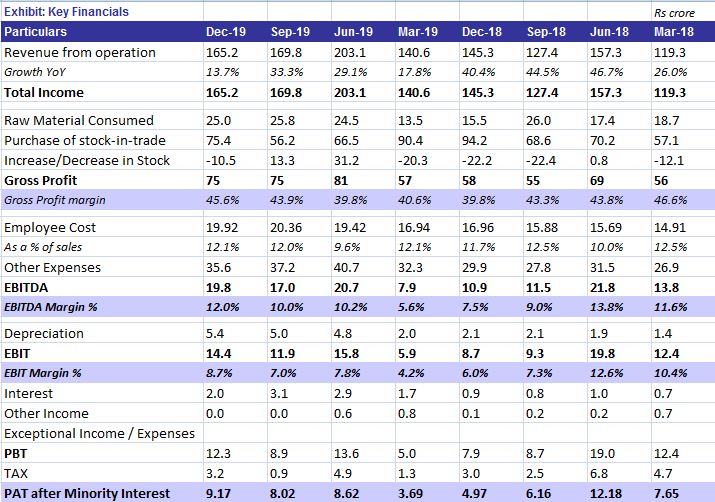

Q3FY20 Result analysis:

- Safari has reported 14% revenue growth, whereas industry leader VIP has reported flat revenue growth

VIP quarterly revenue

-

Depreciation cost has increased as Safari has adopted Ind AS 116 “Leases”

-

Gross margin has improved to 45.6% vs 39.8% YoY

-

EBITDA margin at 12% vs 7.5% YoY

-

Contribution of traded goods was 54.4% during the quarter; company may face some supply side issue due to coronavirus outbreak in China

Both VIP and Safari which had good run-up due to upside PE Re-rating backed by PMS/FII will correct significantly and might lend at real valuation due to -

(1) VIP and Safari both has more than 50% contribution in top and bottom line is from Chinese imported goods. Due to freezing of supply chain and higher price from Chinese manufacturer, these company will suffer

(2) Panic due to CORONA. Travel industries business is going to wiped out in current year. Even though corona will come under controlled, fear among people will postpone their travel next year.

I was just wondering,

In case of SAFARI, I see operating cash flow has not generated as per the sale and also receivable has increase drastically. Still Safari is in boom for buyer(except current month).

I can see, they are drastically increasing market share with low margin, also looking for tie up valued brand to sale in India.

Can someone put some light what is the future path/plan of safari so it got evaluated?

Hi, did anyone attend the AGM. If yes, please share notes. Thanks.

Key Takeaway’s from AGM

The company reported positive operating cash flow during FY20 and was expecting to continue the same in FY21 also, had covid not happened. However, owing to the pandemic, FY21 could see negative cash flows

The company plans to fund future growth from internal accruals and will not need debt or equity dilution to grow going forward

The company would increase sourcing of soft luggage from India

No plans to enter ladies handbags or premium luggage segment

Volumes have shown some MOM improvement after a complete washout in April and May 2020 due to Covid

Retail stores stand at just 40-50 stores and no major impact on the same. Also, the company does not expect that its customer touch points will be impacted due to Covid

No salary to CMD for FY21 and no salary cuts for other employees

Disc: Invested