Closely monitoring portfolio every now and then and frequent churning had not been fruitful for me. Instead all time and effort must go into understanding the business and risks in each story. Hence resorted to minimal action on portfolio front as inaction and patience pays more here.

You can find my updated portfolio and views on the stocks held in my blog. Will update that annually.

Cant agree more and such a approach has served me very well till now (even in my modest beginning)! But I find it interesting in terms of Capital allocation within ones portfolio. For an amateur investor who is gaining experience the next biggest challenge would be to handle capital allocation.

I do think, understanding the business and risks is important. But once you have done that, i find it more thrilling to answer the question of why there is difference in P/E between PI, Kaveri and Dhanuka. And there you learn much more about each individual business and the risks associated to it. Simply asking: Why does Mr. Market treat these businesses differently?

I did already find your blog, which was an absolute pleasure to read! Now, coming to Hawkins - After going through your thread and of the company, I have found that you been some one who was always bullish on Hawkins! I do see the reasons of a fundamentally strong business, but as the (recent) discussion was missing on the relevant thread i wanted to ask: With no significant improvement between FY13 and TTM yearly figures and with all operational issues resolved, what short term triggers do you further see in the story unfolding? And hence what makes it attractive at current valuations?

True, the quality of business will surely be a key differentiator in Capital allocation decisions too.

Hawkins have had supply side issues over the last few years, FY14 is the first year after all supply side issues have been resolved and company is working on fast pace to introduce induction cookers and cooktops and host of other devices.

Led by a change in top management, with infusion of young blood, company will chase growth as opposed to restoring supply which was the focus area earlier. Hence, if the going gets right shareholders will be rewarded handsomely.

As seen from the recent TTK numbers, large base was a headwind for them while the same base being lower (almost stagnant profits from FY10-13) will act as a tailwind for Hawkins. However, given the poor macro situation sales of new devices might take some time to pick up and also expansion into newer channels/higher ad spends etc might dent the bottom line for a few quarter.

So I am expecting a steady build up and superior return from the next 2-3 years nothing immediate from the next 2-3 quarters.

Your blog has projections for Hawkins for fy14. Are you more or less sticking with those numbers?

fy14 eps at 80-90 does not seem difficult ( inspite of poor macros). IN that case next 2 qtrs should be promising?

Thanks

Rudra,

Cant agree more and such a approach has served me very well till now (even in my modest beginning)! But I find it interesting in terms of Capital allocation within ones portfolio. For an amateur investor who is gaining experience the next biggest challenge would be to handle capital allocation.

I do think, understanding the business and risks is important. But once you have done that, i find it more thrilling to answer the question of why there is difference in P/E between PI, Kaveri and Dhanuka. And there you learn much more about each individual business and the risks associated to it. Simply asking: Why does Mr. Market treat these businesses differently?

I did already find your blog, which was an absolute pleasure to read! Now, coming to Hawkins - After going through your thread and of the company, I have found that you been some one who was always bullish on Hawkins! I do see the reasons of a fundamentally strong business, but as the (recent) discussion was missing on the relevant thread i wanted to ask: With no significant improvement between FY13 and TTM yearly figures and with all operational issues resolved, what short term triggers do you further see in the story unfolding? And hence what makes it attractive at current valuations?

Supreme’s standalone results are decent, however the consolidated numbers are pulled down due to loss in Supreme Petrochem.Company also monetized additional 0.26 lac sq ft from Supreme Chambers as discussed in the AGM.

However, given the recent huge run up, I believe there are better opportunities at this point and one might start nibbling at Supreme from lower levels.

A) Even in cloning do not blindly venture beyond your circle of competency. There might be discussions on various stocks promising stupendous returns, but without thorough understanding of the sector and risks it is better to stay out.

“…There are also competence differences. **I may not unnderstand some things they invest in because they just donât fit within my parameters. **For example, if you look at their 13F filing, recently they bought a company called Davita. They own $1 billion worth of Davita stock. Davita basically runs dialysis centres. They are the second largest kidney dialysis provider in the world. **It is a very specialized business â I donât understand a lot of dynamics about that. They clearly have a moat but it is unlikely we will invest in them. **The commonality would be that I would be looking to buy things well below what they are worth. I donât understand it but probably Davita is trading well below what it is worth…”

B) Accept a lost investment in the right context and move ahead. It is critical to treat each losses as incremental learning and more to make sure the mistakes are not repeated rather than focusing on loss.

"…Actually, my funds were down from peak to bottom 65% or so. But my wife mentioned to me that she didnât realise the funds were down that much because throughout that period, she saw no change in my behaviour pattern or my sleep pattern or anything like that. You have to keep things in context. There is a famous quote: if wealth is lost, nothing is lost. If health is lost, something is lost and if character is lost, everything is lost.

The other important thing is I am not bouncing up and down with stock prices. I donât even know what the markets or my stock did today. All of that is just irrelevant…"

Kaveri seeds: I think seeds companies are well placed. Agri sector itself is well placed especially if Narendra Modi comes into power. Nuziveedu Seeds is also planning to come up this year.

Hawkins Cooker: I Think a 4-bagger is waiting in Hawkins. The market should pick up. I planned to buy it but I am waiting for sales to pick up.

Unichem labs and Dishman: In pharma the ones I prefer are Lupin and Sun that’s it. But there are some good business models in Health care delivery that are coming up.

Amara raja: They are having ambitious plans. 10000 cr revenue by 2020 i think. Its a good stock and allocation is also good.

Gruh Finance: This is my all-time favourite. I am never tired of talking about this one. I believe that it is a standard 30% return stock.

One thing i can suggest here Please do not be in bad businesses just for the sake of 20% higher returns. Or because of Low PE ratios. At the end, it is the discipline to stay with good businesses that keeps our money intact.

Hi Rudra.Nirmal Bang has come out with a very comprehensive investment case for ARBL(target price of 426) Its available on Researchbytes.com.Since both of us share pretty much similar feelings about ARBL,I thought you would like to read it.

I have mentioned my inhibitions on the management, regarding the excessive management compensation and political nexus. I have discussed the reasons of opting out from this great business on my blog in details. Hence the stock is out of my radar.

Hi Rudra - just wondering is it possible to get an update on your portfolio as it would be a great learning to see how it evolved over the years. Thanks as always.

Looking at this thread after a long time, would look forward to use this more to reflect my thoughts and gather more perspectives from the esteemed boarders on the forum

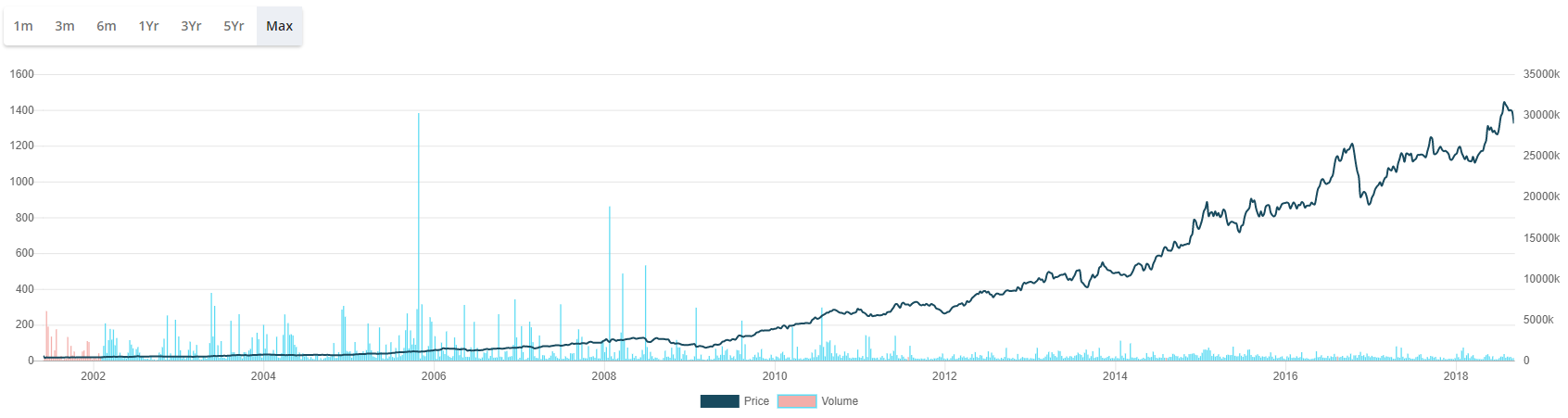

This was a point that came out multiple times from Saurabh, in his recent interview, where he refers to his Coffee Can portfolio (last 10 years, 10% revenue growth, 15% RoC) - don’t touch your compounders. Page has been a 30x in the last 10years and Asian Paints is up 1500x since its IPO in 1983, so despite that inherent froth in terms of valuations, one should hold on.

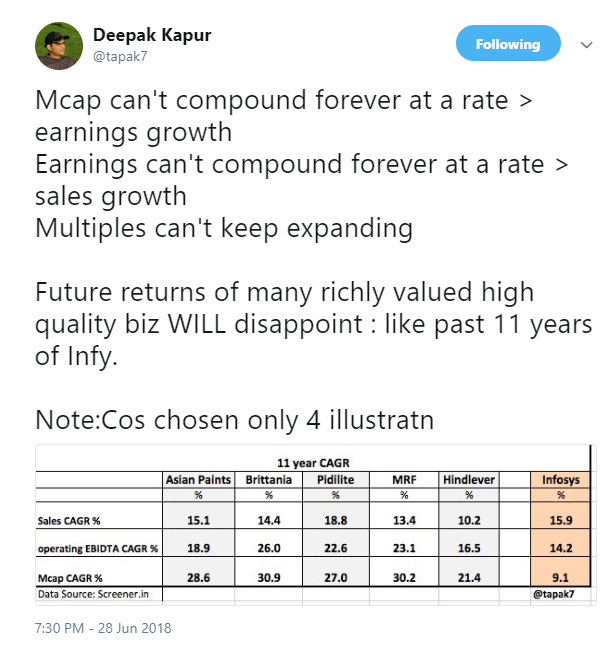

Of course this is beyond any meaningful perspective for Value investors to even remain invested, forget buying into these at this juncture. A very pertinent thought brought out by Deepak in this tweet

I believe a few things that stand out for these companies are as follows :

They have nurtured and strengthened a strong moat very carefully which makes it next to impossible for a challenger to dethrone them from their pole position in the short to medium term (Asian Paints in paints, Pidilite in Adhesives, Page in apparels etc.)

These companies have a very low technology obsolescence risk associated with them - (and why I think Infosys is not the best counter example here) - Margin of safety comes from business endurance here and not from price action

These are ideal candidates for patient and large pool of capital (pension funds for e.g.) where

a) sufficiently long investment horizon 10years+ or more

b) not losing money over long term is paramount

c) hurdle rates might be lower and

d) there is no relative performance benchmarking but only absolute wealth creation as the objective

So in cases, where these criteria are met, these might well be ideal investment candidates, while we keep looking at them with skepticism.

A very nice document on Relative valuations, discussing different perspectives of absolute valuation (DCF and others) with the relative ones (P/E, EV/EBITDA). Some very useful pointers and empirically working with the framework with 1500 top firms in the US for the last 40 years!..so valuable.