Do you mean Repro exporting printed books of Indian Authors ?. Repro has an agreement with INGRAM where it can sell books from its Indian authors worldwide using INGRAM. Also I do not have any details on the opportunity size here (my view is that it may not be much).

Yes (at least for now the focus seem to be only for India). INGRAM has similar tie ups for other countries (read last investor conf call transcript which has some details). I’m not sure if this model can be expanded to other countries (we need to probe the management to check if there is scope to setup Books on Demand for countries where INGRAM do not yet have any tie ups). But I believe, if this model works out, there’ll be significant opportunity in India for years to come.

Currently , I believe it has negligible share to revenue ,however, earlier too mgmt has given view on this question that they see this option also as a market though I don’t remember them giving a market size estimate .Coming to other question on going beyond India, the whole essence of this model is 0 inventory and quicker delivery ,so, I feel a local player would be more suitable to replicate the model rather than Repro going in another country n doing this set up. Globally, there r 8 such partners and each of them are limited to that country itself. So, country wise there r opportunities available for future but my instinct is that those opportunities would be fulfilled by local partners in case there is no one filling that gap right now

The promoters could have been in media and give huge growth forecasts.But they have not done so and this is a good positive from management side. They are doubling the capacity and they are doing so because they see demand growth.

I am keeping some track of repro books on demand on amazon and if you see the product listing under seller information , the number of pages has increased from 250 to 341. (Sorry i didnt take screen shots).So the number of book titles is surely increasing.Currently as i see they have 494352 books on amazon. Further i checked the pricing for some best selling books . There are multiple sellers and repro india is the cheapest in most cases. Also its an amazon full filled seller.

A majority of the books is available for free on amazon kindle , this can be a problem for repro , but i believe book lovers prefer hard copies over soft copies. I did my own little survey with the book worms i know.

The next result will be very crucial wherein we will come to know how books on demand is growing further. Hoping for the best

Hi all,

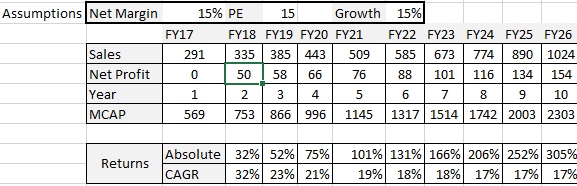

I am new to investing, so still learning the ropes. Would this be a fair extrapolation? I know that I have not considered several variables that can go for or against Repro and this is a rather simple/crude way to forecast? But is it too far fetched?

As per latest Annual Report Disclosure, there are lots of Related party Transaction. Should it cause any worry?

Also there is one subsidiary in which Repro owns around 75% stake. How may I Know who are the owner of balance shares. There are material related party transaction with this entity.

You are right about this. I was also slightly worried about it when I read that yesterday. I am surprised at so many related party transactions. Here are the worrying ones:

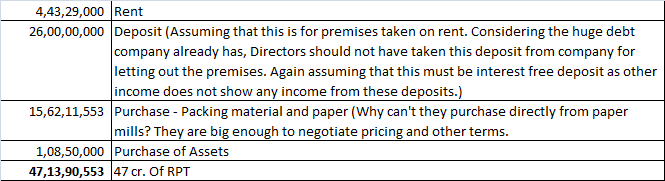

Rent:

The promoters are drawing rental income amongst them of worth Rs. 1,53,70,000. Especially worrying for me is the amounts drawn by Zoyaksa Consultants Private Ltd. which is of Rs. 96,53,000 and Trisna Trust of Rs. 89,63,500.

Zoyaksa Consultants Private Pvt. Ltd.

How is this company related is something I dont know yet? But not only are they getting rent of Rs. 96,53,000 but they are also being paid a high sum of 156,211,553 for materials purchased by Repro.

Anyone having idea till what time they are going to announce Q1FY18 results. I understand that as per regulation listed companies need to submit results to stock exchanges within 45 days from the end of quarter.

Zoyaksa Consultants Private Limited’s Corporate Identification Number is (CIN) U74100MH1994PTC076636 and its registration number is 76636.Its Email address is dimple.c@reproindialtd.com and its registered address is R-F 13, Sun Paradise Business Plaza, Senapati Bapat Marg, Delisle Road, Lower Parel Mumbai Mumbai City MH 400013 IN. It is inolved in Legal, accounting, book-keeping and auditing activities; tax consultancy; market research and public opinion polling; business and management consultancy.

So, same address, email address points to repro, same promoter group. They must have provided rationale for related party transactions… haven’t they?

Ps: just glanced thru related party transactions for 2017 in the latest annual report. Takes 5 pages…n company mentions all those as business transactions…i find this very odd. Definitely something which must be looked into in depth.

Company has issued 500000 options today for a price of Rs. 561 per option and the vesting period is also less. Out of these 100000 options have been granted to the directors. But vesting period is very low at 1 year. They should have atleast gone for three years to have meaningful retention. We can check at AGM.

Repro results. look like strike has taken a toll on revenue growth though still maintained profit but tahts totally due to other incomes, they got some of receivables. lso, provisioning in other income. Notes are very important to read

Within Other income there is 9.39 crores shown as recoveries from customers - which is very good. This gets nullified by an additional 9.00 cr provision that management has put in the other expenses. So, the bottom line being in green is not due to other income only.

Discolsure : Added after the company declared their FY17 results…

Below article covers interesting case study on how an unethical management can destroy minority shareholder wealth inspite of having excellent business and near monopoly. Something to ponder upon in case of Repro considering various related party transactions and non satisfactory answers provided in AGM.

Zoyaksa Consultants Private Pvt. Ltd. is Mr. Sanjeev Vohra’s co.

Summary of Related Party transactions in 2017 AR.

Besides above, there is remuneration to KMP’s to the tune of Rs.1.53 cr which may be justified considering the absolute amount given to each person. However, out of this amount Rs.31.75 lacs is paid to family members of KMP’s and I am not too sure about their involvement in the business.