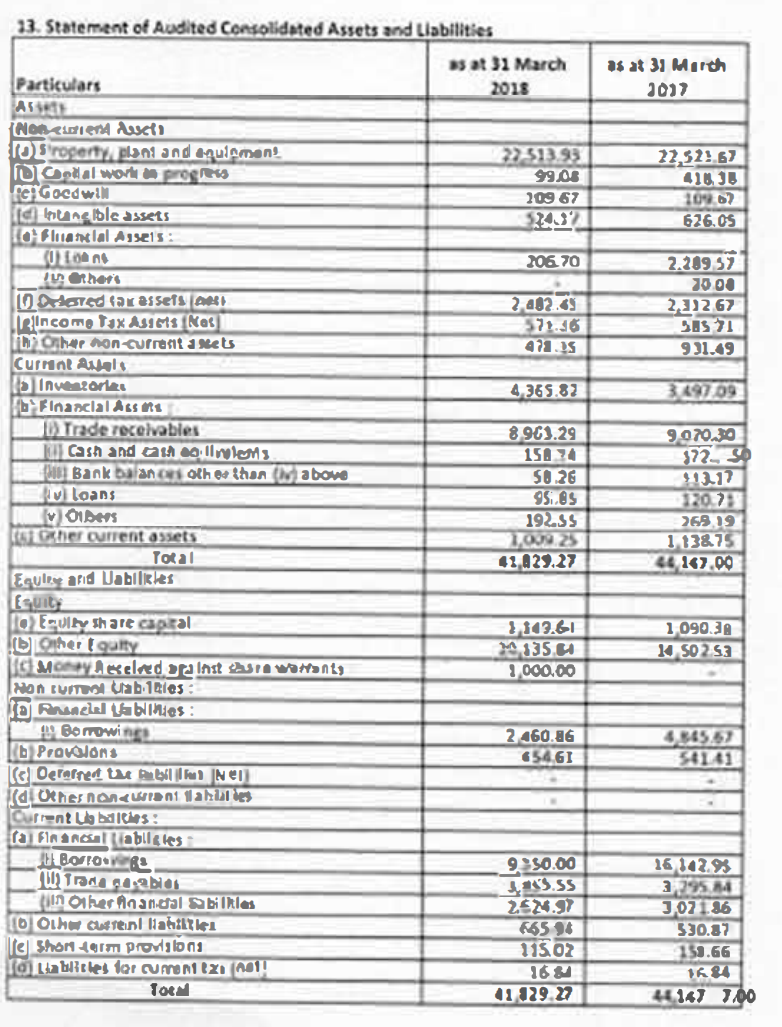

Has anyone been able to decipher the numbers in this balance sheet? It is smudged so badly as if they dont want anyone to read them.

It looks like WC hasn’t improved much though the BoD contribution is growing. If am reading it right Receivables have remained almost same (Is this still due to Africa?). The inventory could be due to domestic business.

I have my reservations with the proportion of the long-tail’s contribution to sales. Although 80-20 is the common representation of Power Law and is probably where the 80% of book sales coming from front titles comes from, I think it could be more like 95-5 where 95% of total book sales by value comes from a handful of Academic books and Bestsellers (which might be less than 1% of titles). This is my gut feel and is not backed by research and I doubt if there exists any, for the Indian market. So I am a bit skeptical about market size and BoD revenue projections for FY20 and onward that I see in the earlier part of this thread.

Also, has anyone done any calculations on RoCE for BoD business? Considering the current D/E and valuations, investing here without knowing this crucial figure could turn out to be very risky. Assuming negative working capital, we need to know what the value of assets for BoD (current capacity of 6000 books per day?) and have to find the split for BoD revenues and profits. Without figuring this, we will have no way of knowing how self-sustainable and scalable this business is, irrespective of the opportunity size.

Disc: Researching