Very basic question related to NPA’s.

NPA are bad for any banking company. But in case of HFC companies they keep the actual property as loan guarantee so why is NPA or defaulting bad because in case loan repayment is not done company sell the asset and recover money. Can someone please help me understand how NPA work? Why it is bad despite having mortgage?

No big impact of Chennai floods on asset quality: Repco MD

The company has a total of 146 branches, 11 of which are located in flood impacted areas of Chennai and around 2-3 percent of customer are impacted due to floods.

1 Like

The comments from management should address the concerns of investors to large extent I think. Infact the Management sounds bullish with the expectation of “naturally” and easily achievable 30% loan growth as in 1st half going forward!

1 Like

@sunilsurana : Though HFC can get the property, it takes time to get possession legally. Also it’s not easy to sell the property. Their primary business is not selling properties but making loans. In tough real estate market, a property can take years to sell even at low price. To absorb losses for long period of time is impossible for any financial.

In US subprime crisis, many home loan borrowers deserted houses and defaulted on loans. Banks literally had legal possession of thousands of empty houses that won’t sell. Mortgaged property acts as a comfort for HFC but too much of it is bad.

6 Likes

I think we need to take these assertions with a pinch of salt as top management have been getting stock options pretty heavily. They have vested interests in keeping feel good factor maintained when the stock is taking pounding. Anyway NPAs would be a problem until FY17 when recognition becomes due. However, it will not lead to permanent loss/write offs as they have demonstrated in the past.

Disc: One of the large holding in my portfolio

2 Likes

Repco results have been announced and I believe the Home Finance sector juggernaut continues selectively.

Prima facie, the numbers do not show much signs of Chennai floods impact, the loan sanctioned and disbursed are very good too.

Let the numbers speak:

YoY Q3 FY15 vs. Q3 FY16 comparison:

Revenue growth: 28%.

Profit growth: 26%.

YTD FY15 vs. YTD FY16 comparison:

Revenue growth: 28%.

Profit growth: 22%.

- 37% growth in loans sanctioned for corresponding periods of FY15 vs. FY16.

- 36.5% growth in loans disbursed for corresponding periods of FY15 vs. FY16.

- Gross NPAs are 2.29% vs. 1.99% - YoY.

- Net NPAs are 1.36% vs. 1.16%. - YoY.

Loan disbursement trend is heartening and in fact above expectations despite the slowdown concerns written everywhere.

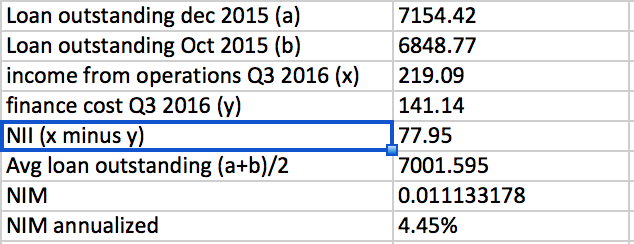

NIMs are stable around 4.45% (as calculated below).

9 Likes

What do you think about the NPA levels? Provisions have gone up almost ~80% 9m YoY.

The management said in the last concall that they would take 2-3 years to reach Net NPA of around 0%. Also as per the last CNBC interview, management said that the effect of Chennai floods would not be immediate as they will be a offering a revised payment schedule (delay of 1-2 months in EMIs) to the affected accounts. Thus, if business conditions do not normalize, we can expect even higher NPAs over the next 1-2 quarters.

Do you think they could have provisioned more to reduce Net NPAs at the cost of profit growth?

One need to find out if the increase in NPA is coming from Kerala or Telangana. Market will be ok if it is coming from Chennai region.

Provision Coverage should be about 47% of GNPA.

8-9% of Book Value is under cloud.

But if one looks at last 12 quarters, many quarters have been where GNPA are above 2%.

Some business qualities remain intrinsic to the business model and don’t change regardless of management quality.

For Repco, the investor has to understand that the company on an average will have about 2 % GNPA, 10% book under cloud. These characteristic won’t change even if the best of management tackles the business.

The most inportant number to watch is ROA which is more than 2% and if NPAs start affecting ROA then investor has to realize that fundamentals are changing for the bad.

For now things look good.

Disc: Invested and maybe biased in views.

4 Likes

Latest Motilal Oswal report on Q3FY16 results http://www.motilaloswal.com/site/rreports/635906111721150833.pdf

2 Likes

Repco Q3FY16 Earnings Presentation

http://www.repcohome.com/images/RHFL%20Q3FY16%20Earnings%20Presentation.pdf

Repco Home Finance Q3-FY16 Earnings - Concall Invite - 11th Feb at 3 PM IST

Hey guys ! Just had a quick question - Does any one know what the status is on Masala Bonds? Have companies started issuing them already (I know HDFC was thinking of issuing them in Jan 2016) not sure what happened.

What I am trying to Find out -

- Are Indian companies permitted to float these “masala” bonds currently? If not, is there any time line from the RBI for the same?

- If companies have issued these bonds, does anyone know what the yield of these bonds are lets say for AAA rated Indian companies? How significantly below 8 ish % ?

- Is this on Repco’s radar?

Reason why I ask -

If HFC s such as Repco, alter their borrowing profile incrementally to masala bonds, this could result in a significant impact on their incremental NII & NIM (assuming that these masala bonds are atleast 100 to 150 bps cheaper than the current cost of their funds (from domestic sources). Any information regarding masala bond yields will be helpful as this could significantly help HFC s like Repco expand margins.

Thanks

Rohit

Hello to all,

I have written a short story:

REPCO HOME FINANCE

CMP 580.90 MARKET CAP 3633.03 cr

BACKGROUND:

CORE BUSINESS:

Repco Home finance ltd. is presented in two segments – individual home loan and loan against property. The company provides a variety of loan to individual borrowers in both the salaried and non-salaried segments.

Repco’s primary sources of customer are:

- Loan camps (contributes 70%)

- Customer walk-ins

- Referrals

Process: - Primary assessment of customer documents is done and in-principle sanction is given

- Then customer is send to branch for further processing

- The branch personnel act as a single point i.e. from sourcing of loan till prelimnary checks on the creditworthiness of customers.

The company has now started DIRECT SALES AGENTS (small explanation) model which is still at an early days and has been employed in some branches of Maharashtra.

Repco’s primary sources of FUNDS:

The company has diversified source of funding viz. refinance from NHB, long term bank loan, working capital loans from Repco bank, NCD and CPs.

With the interest rate going down the share of NCD and CP borrowing would go up

The average cost of borrowing is 9.59%.

Credit risk process:

The preliminary appraisal is performed by branch manager, branch level valuers and lawyers.

Revalidate at corporate office level before sanction

Each borrower is rated based on a dynamic credit rating modal consisting of 18 parameters.

The interest rate is chargeable on the credit profile of the borrower.

BULLISH VIEWPOINTS

a. Company:

Lower competition from banks and other HFCs.

o Self-employed constitute 51% of work force in India however large HFCs focus on salaried segment due to ease of appraisal and clear property titles lead banks to focus on these areas

Non-salaried class is highly penetrated.

o Loan to salaried and non-salaried consist of 43% and 57%.

o Tier 2/3 and peripheral area of tier 1 are largely non-salaried and are under served by large bank and RHL has nearly 15 years of experience.

o Total loans written off since inception: 0.06%of total cumulative disbursement.

Low operating cost structure

o Lean branch model with 3 – 4 employees per branch with local knowledge

o Low rental

o Direct business

b. Industry:

Huge housing shortage

Govt focus in this sector

Interest rate cycle is low

RHL’s current leverage levels is at 6X vs 16X net owned fund by the NHB

BEARISH VIEWPOINTS:

A. Company:

i. The company’s loan portfolio is highly concentrated in Tamil-nadu

ii. The results are seasoned due to concentrated loan book.

B. Industry

a. Government intervention

i. Higher provision for the asset would lead to lower profitability

ii. Any laws which would affect the industry.

b. Slowdown in real estate

Valuation:

- Loan book growth : 25% for last 5 years

- NIM: 4.1 (comes with HDFC bank and Gruh)

- Cost to income ratio:18%

- Provisions are 62% and would be 100% according to annual report

- P/E 25.46

- Book value 147.10

- Dividend yield 0.26%

Views invited

4 Likes

A recent article on HFCs in Economic times covering Union budget 2016 and future growth of HFC:

With the risk of being repetition,

-

The tailwinds for the housing sector are very strong and are only getting stronger. I’m not aware of any sector that has such strong tailwinds in the recent past. I have listed below some of them.

-

Given the tail winds, if we can invest in select high quality housing finance stocks, there is high probability of out performing Index by a considerable margin.

-

The demand side was never a problem as most individuals prefer owning a home. They can only procrastinate but cannot avoid indefinitely. So, if Government can ease the supply side concerns then this would be a highly secular sector for the foreseeable future.

-

Passing of real estate regulatory bill on 10th March, 2016, finally, will address the supply issues. More investments would be made if the sector is regulated as there is safeguard for investors. This is positive for both real estate builders and housing finance companies.

-

There are tax incentives proposed with some riders for low cost housing developers which if used properly would lead to reduction in supply of low cost houses. Google for complete details.

-

There are tax deductions available for the end customer and there was some marginal increase as well in this budget but it’s only incremental. People will use calculators to avail such benefits to the last rupee, which is good thing to do.

-

The interest rate cycle is on the downswing in India and over the next few years there would be good reduction in the interest rates which would be passed onto customers thus fuelling demand and also improving margins for the housing finance companies. It is better to be ahead of the curve here to benefit with the upswing.

-

How much this ‘housing for all’ by 2022 would benefit the housing finance companies need to be dissected but this would not be negative at least. I’m sure PM Modi would want this initiative to be a huge success else he would be targeted threadbare by opposition. Either way, PM Modi has the will to do this.

-

Over time the housing finance companies would get an incremental fillip to their growth by 5-10% over and above their current growth and the one who is determinant on maintaining clean loan book with strong credit risk management process in place will do well.

You need to be aware of the risks before going gung ho on these companies as leverage is a double edged sword. It depends on who is using it and how

2 Likes

any idea how much will this going to make an impact ?

Here is a recent brilliant interview by Mr. Basant Maheshwari Sir reiterating the same view about HFC’s.

Housing fin cos, pharma midcaps and hi-tech IT are favourites: Basant Maheshwari, Wealth Advisers

I did not understand the IOT companies though. Any ideas about the players in the IOT/SMAC space? Kellton or Lycos? @richdreamz @catchsudipto

P.S.: If this name-based sharing is not allowed, mods please edit the post.

1 Like

Just looked at this thread. Sorry to be joining late to the discussion. But would just add my two bit:

What you are buying in an HFC is two things: its loan book (and the ability to grow that loan book) and its earnings (and the ability to protect the earnings with low cost, low NPAs, low cost of funds)

The loan book can be financed in two ways: own funds and borrowed funds. If own funds are high the book value will be high and if own funds are low the book value will be low. (Book value = Assets i.e. loan book - Liabilities i.e borrowings & liabilities). So book value is a function of the mode of funding the loan book.

When you buy a HFC stock, what you are essentially buying is that portion of loan book which is funded by Net Worth (i.e Book Value x No. of Shares). You have to presume that the rest of the loan book belongs to the lenders.

As such one has to look at the price multiple which is being paid to acquire the Net Worth Funded Loan Book. As a shareholder, your return would depend on the price you pay and that is why PBV (i.e Market Cap to Net Worth) would be an important tool. A higher PBV would thus reflect: the quality of the loan book, expectation of future growth and management’s ability to extract a premium over cost of funds. If any of these deteriorate or are suspect, the PBV would come down. So pay a high PBV only if you are confident of these 3 parameters.

At current price of Repco, the market cap is Rs 3700 crs and TTM PAT is Rs 142 crs. So you are essentially earning a return of 3.86% on your investment, which is quite low for the present. But if you are confident that the management can over the long term:

- Acquire new customers rapidly at a low cost;

- Borrow at a low rate;

- Manage the NPAs; and

- Earn a decent premium over cost of capital,

then your return on price paid would go up, justifying the current high PBV.

If you had bought the shares in Jun 13 at a price of Rs 250/- the market cap was Rs 1550 crs, the TTM PAT was Rs 82 crs, putting your return on price paid at 5.3%. But if you held on to the shares, at current TTM PAT of Rs 142 crs, your return on price paid would be 9.16%. And this growth in earnings over the years due to one or more combination of factors stated above would inevitably lead to a rise in future market cap.

8 Likes

Articles like these confirm my belief that interest rates have finally peaked for many years to come.

No better way to play it through HFCs.

Disc: One of the highest holding in portfolio

2 Likes

Very insightful and I learnt something. Thank you