Usually whenever Marcellus makes a change to the portfolio (buy or sell a stock) it is updated in the newsletter section on their website, although there is a delay of a month or so as they don’t want to disclose what they buying or selling while they are doing it.

You were right. Marcellus has removed Relaxo to make space for TCS. From their blog:

Changes made to Marcellus’ CCP portfolio: Tata Consultancy Services (TCS) has been part of some of Marcellus’ portfolio for the last two years. Work done by our analysts more recently on this company has led to an upgrade to our expectations of the rate of growth in the fundamentals of TCS, as highlighted below. Due to this upgrade in our expectations, we have included TCS in Marcellus’ CCP Portfolio as well. However, given our approach of maintaining an optimum level of concentration in the portfolio, we have replaced Relaxo Footwears with TCS, rather than increasing the list of stocks in the portfolio due to the addition of TCS. There has been no change in our conviction levels on Relaxo Footwears over the past few months. Relaxo continues to be part of several other Marcellus portfolios.

They are holding this in rising giants portfolio along with other stocks like Aavas

GMM Dr Lal Path Labs Page industries and ltts disclosed in the latest rising giants youtube video

I have read all your posts on Relaxo Footwear. And I am really impressed with your hard work as well as detailed analysis. What you found out in Relaxo in 2011, after 10 years, the stock has been more than 10 baggers. You were really ahead of your time. Thats why I amd specifically asking you this question. But since from quite a few times, you have not posted here, I feel that now you are not frequent here, so even other experinced VP investors can also answer. Going forward, in next 10 years, what is the trajectory for Relaxo Footwear. Even now, when market is down by almost 15%, still it is at PE of 106…too costly. Also it has already at high levels, i think 18 crore Footwear they are already making…so considering the unorganised players and even organised players, having quite a strong foothold in this market, what are the long term prospects of Relaxo? also at current valuations, how much is the possibility of its repeating past performance…that means being a 10 bagger in next decade? Kindly Guide…

Disclaimer : I am having a tracking position in this. But if its not a long term compunder, then I would prefer to come out of it…I am not looking for good performance for 2-3 years…I am expecting 20 CAGR for next 10 years…

This is my opinion but here is what I think, with more and more disposable income coming into Middle class household, I believe the masses will move onto more Mid - Premium range/type of footwear such as Crocs, Mochi or other premium brands with an established brand name already in the market.

As Relaxo mainly caters to low cost footwears - between (Rs.300 - Rs.1000) Range, I believe the brand may lose its sales volumes to brands that cater to premium footwear categories such as - Metro footwear and although it has given a massive run in the past it may not be the same for the future, I still expect growth in the stock. However it might be very difficult for them to duplicate their past performance in the future, hence in my humble opinion it may not be a 10 bagger in the next decade.

But I would like to take your attention towards this vast India with 130+ crores people with100 Crore still living under 1 lakh annual income.

Your observation are true, but currently way ahead of it’s time. India still is growing. There are a lot of families for whom Relaxo still is a premium brand. And few who still dream of buying one, one day.

The rally of relaxo is not over yet and has enough fuel to go ahead without any second though.

Yes, I agree with your point and ;oved your inputs in bringing more light on larger masses relying on Relaxo as their go to footwear brand, also as I mentioned earlier there will be a definite growth in the stock, especially because of their supply & distribution my once anti thesis pointer is it might lose some sales volume in the future that may affect the stock price.

All said and done I hope it becomes 10 bagger or even more in the coming decade.

Cheers!! lets enjoy the ride and come back here to evaluate ourselves in few years.

Though the article talks about things like inflation & rural spending.

I am still of the opinion, that the comparison is not right. I mean, a comparison between Metro & Bata seems more logical, then with Relaxo.

Besides, I still think, that the growth potential for tier 3 & 4 cities remains humungous. This is where Relaxo has all the advantage.

Price hike they took recently reduced the volume for articles in lower price band like chappels and the margin continued to bleed because of inflation in raw material prices.

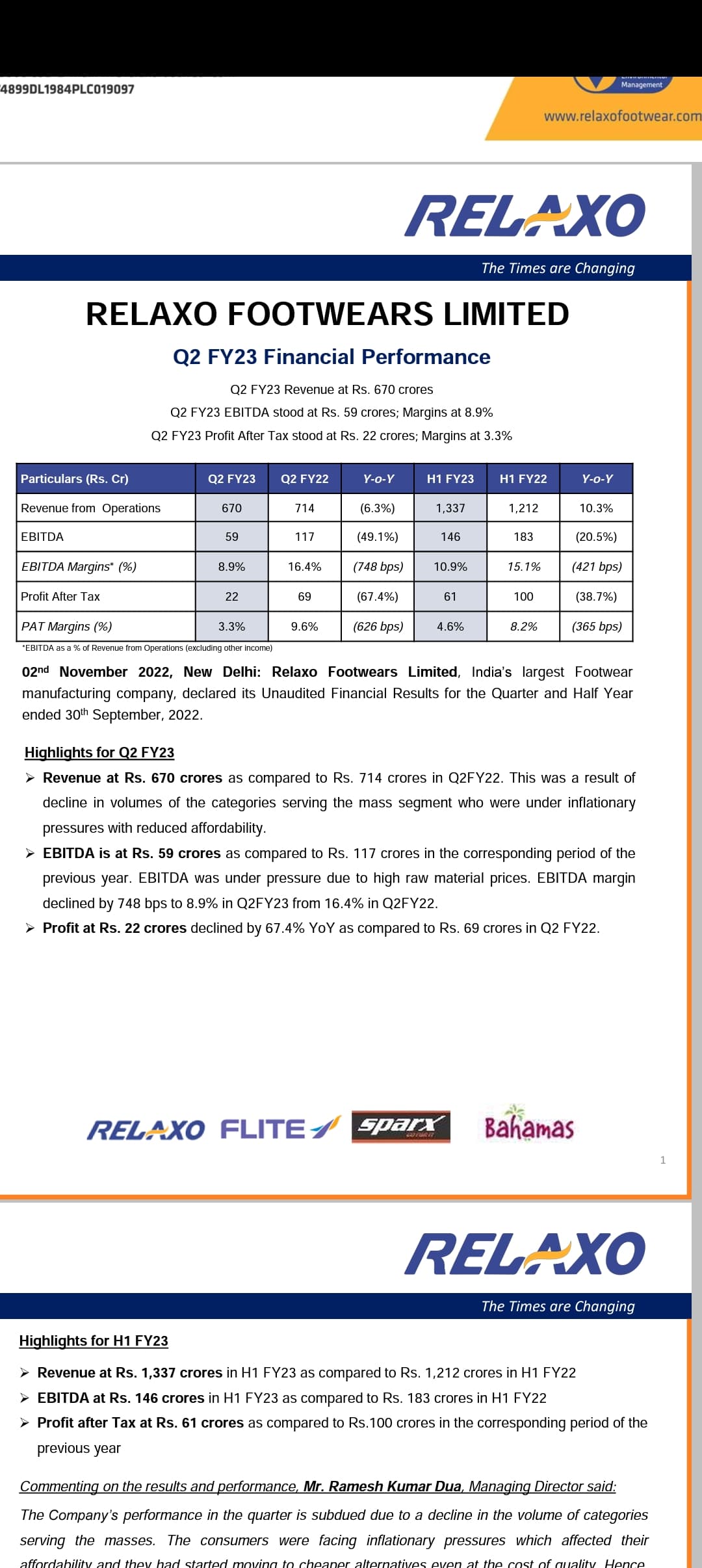

Please see the media release document.

VLS Finance owns 10% of Relaxo Footwear (one-third of Relaxo’s floating stock) and overall it has an investment portfolio value exceeding Rs. 3,000 crore (including Relaxo). These being portfolio investments, not strategic investments - basically, VLS is not a promoter entity for Relaxo so there’s more flexibility to liquidate. Over the years, there has been gradual reduction of VLS’s holding in Relaxo to the current 10% levels.

Honestly speaking this footwear space is still a commodity business. The target segment for this are mostly having no moat unless they will be able to create a brand in some lower middle class, middle class and upper middle class segment.

To be honest, its a fancied stock from a fancied investor. After falling so much, stock is still being valued at 108 PE . This, for a company, which is growing single digit in sales and profits for last 3 years with competition increasing drastically by the day and I have never seen anyone asking for “relaxo” brand while buying footwear… I think more pain in the offing for stock price